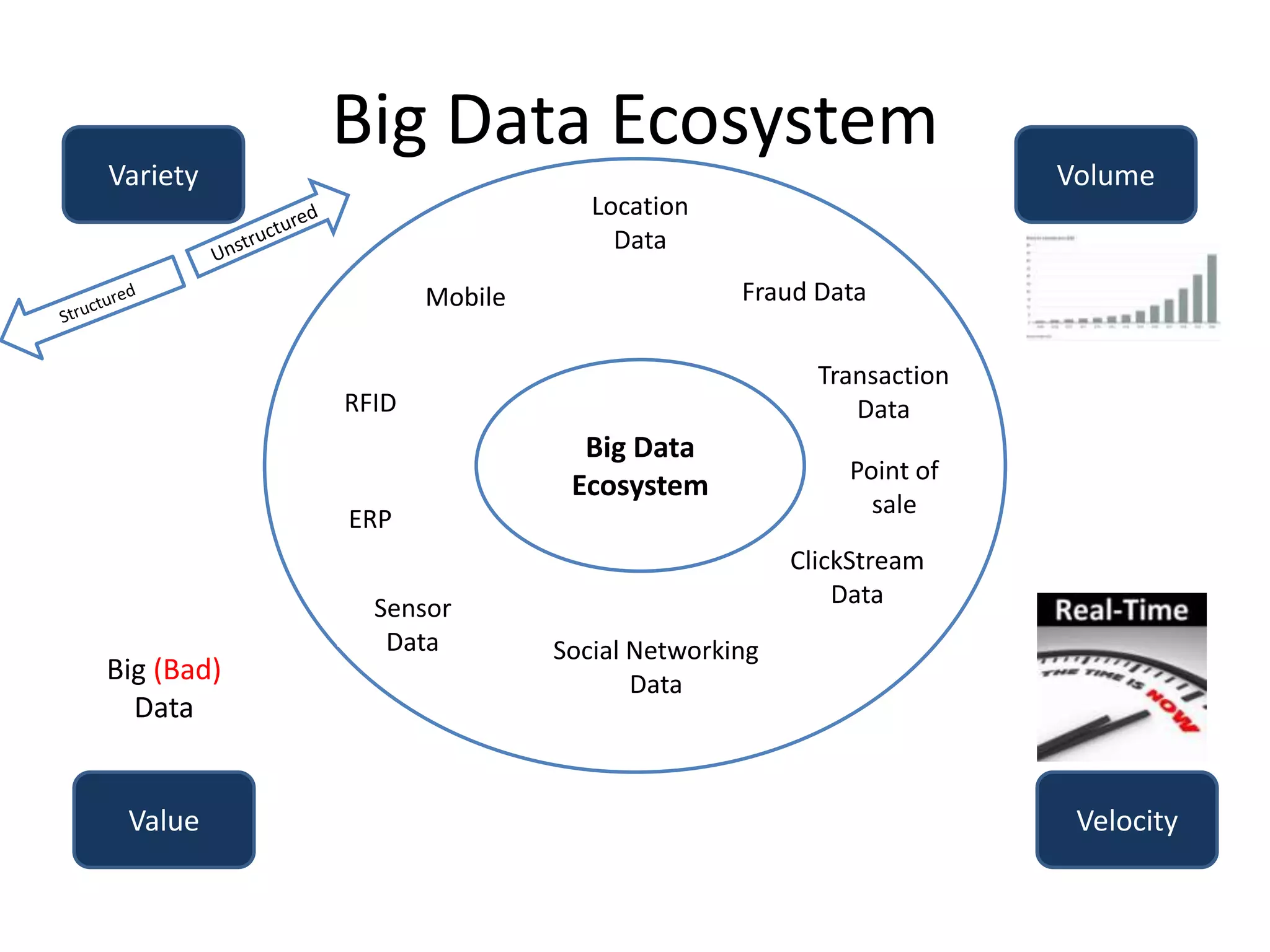

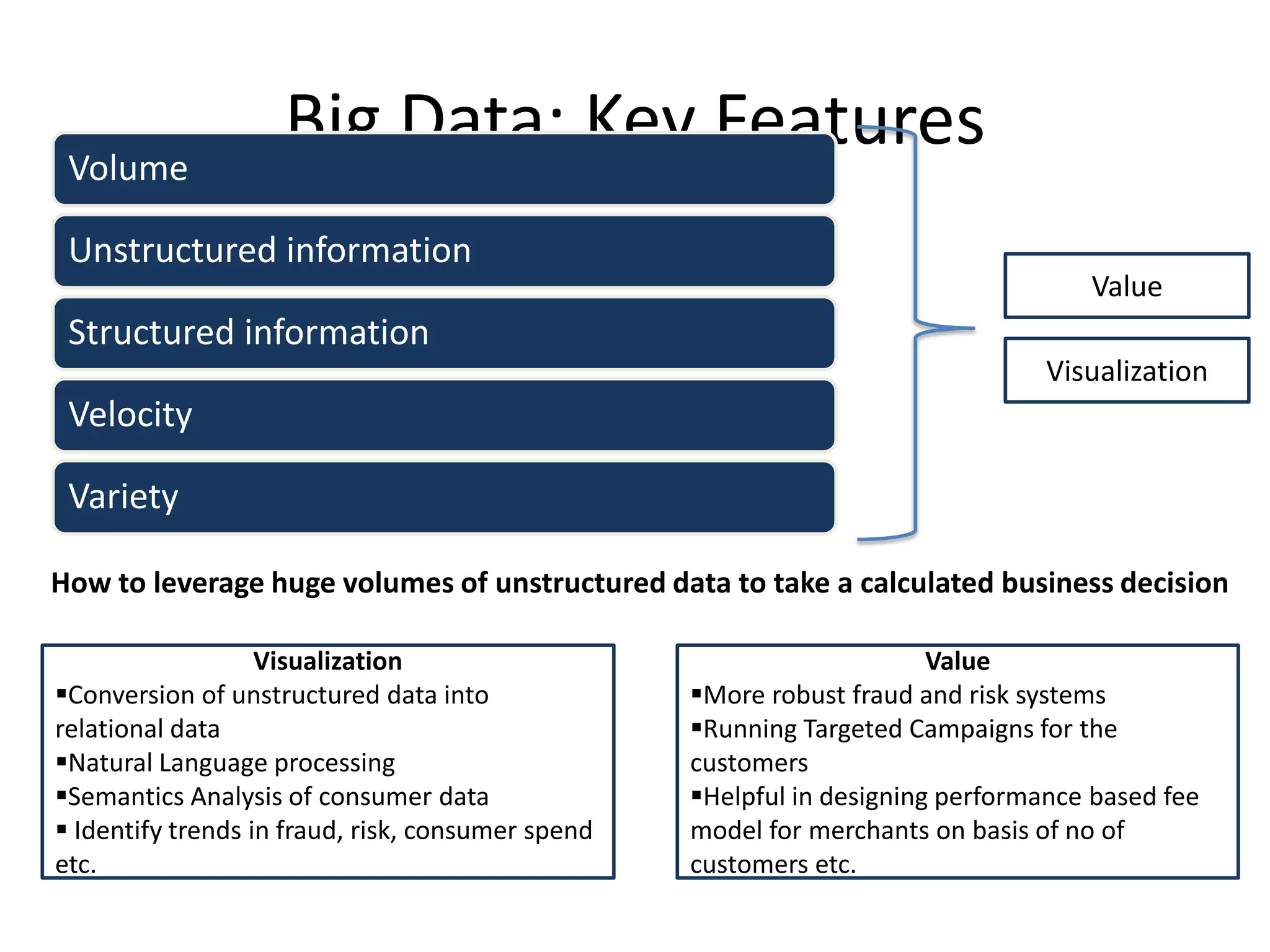

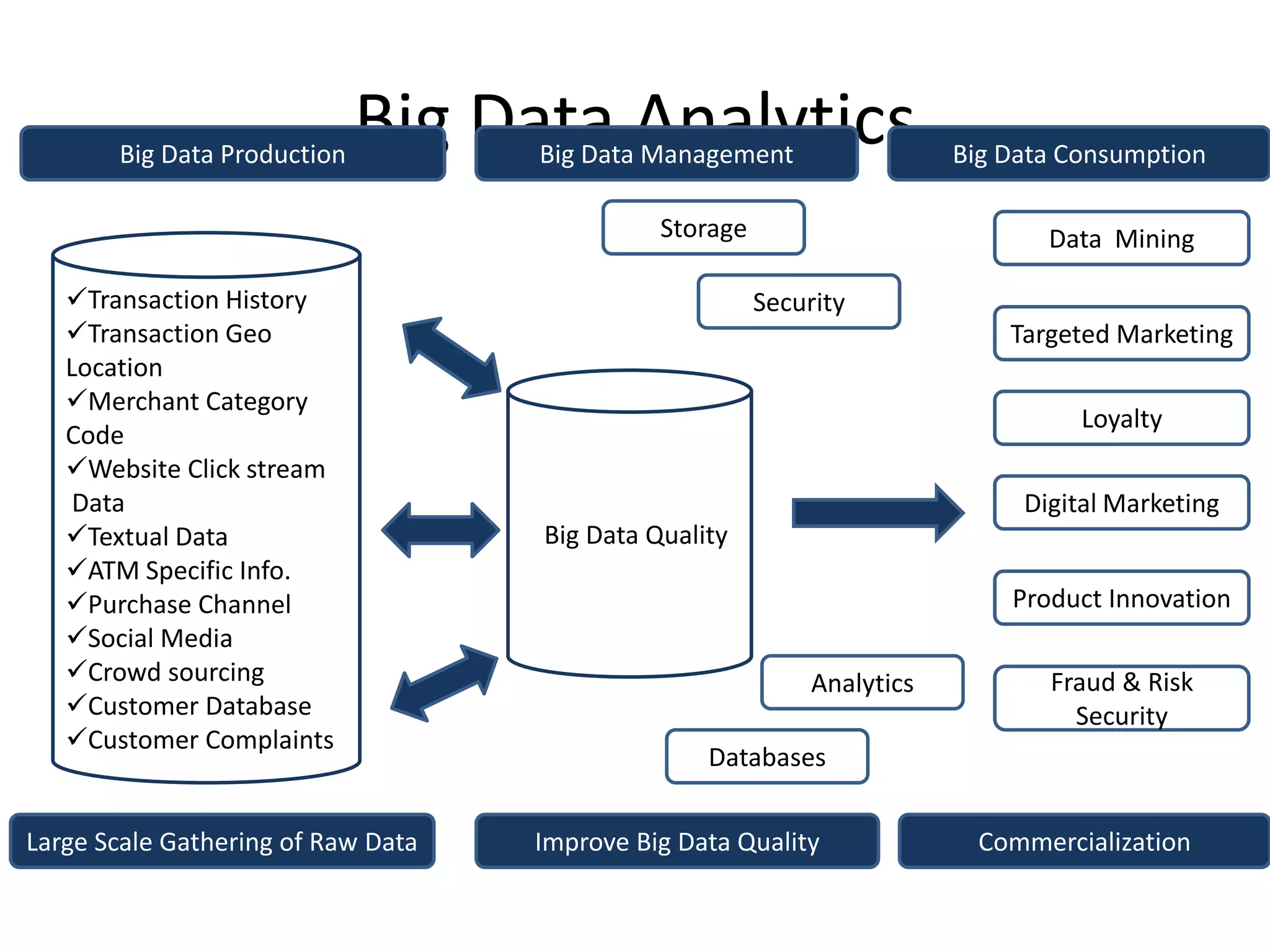

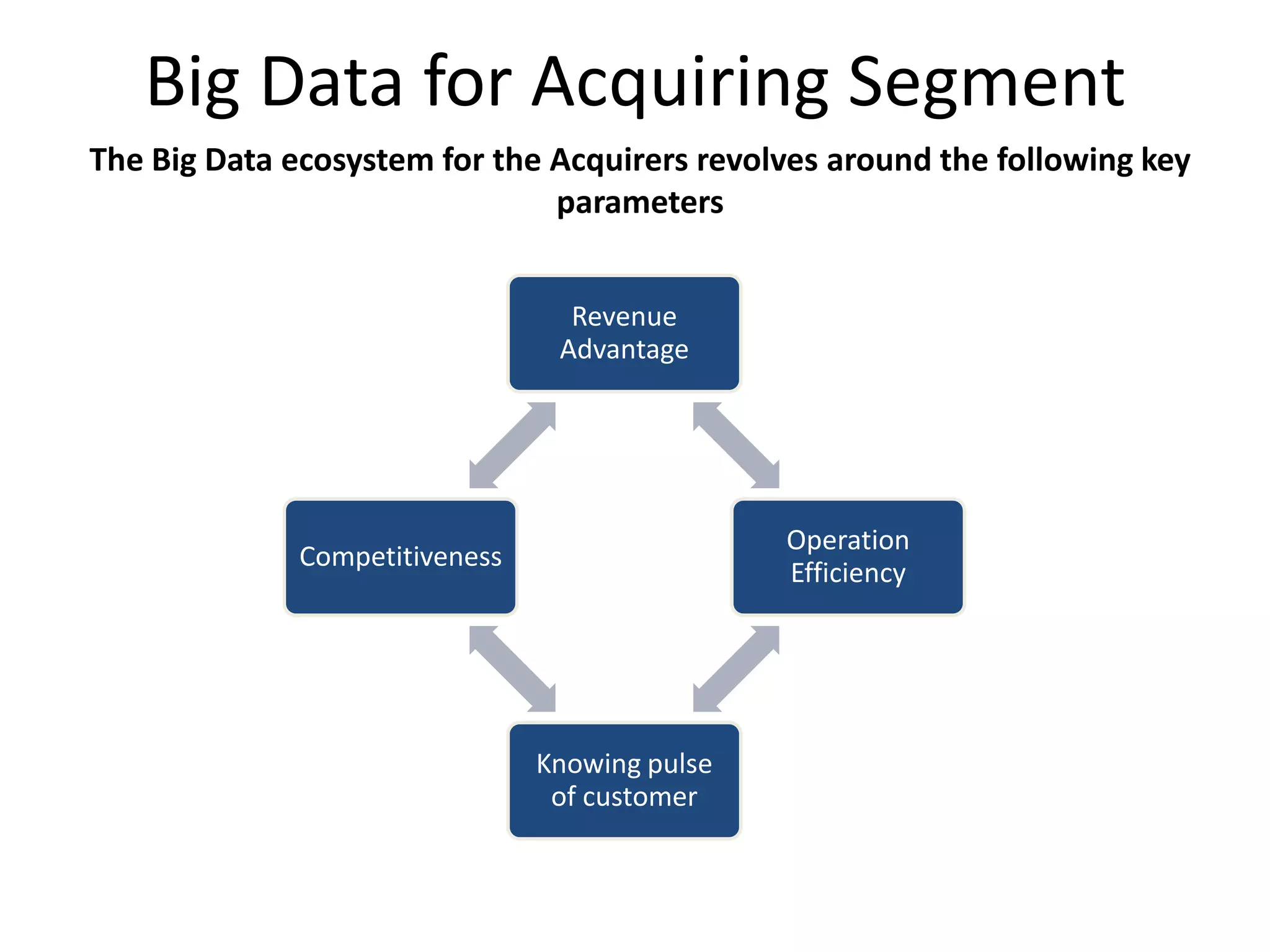

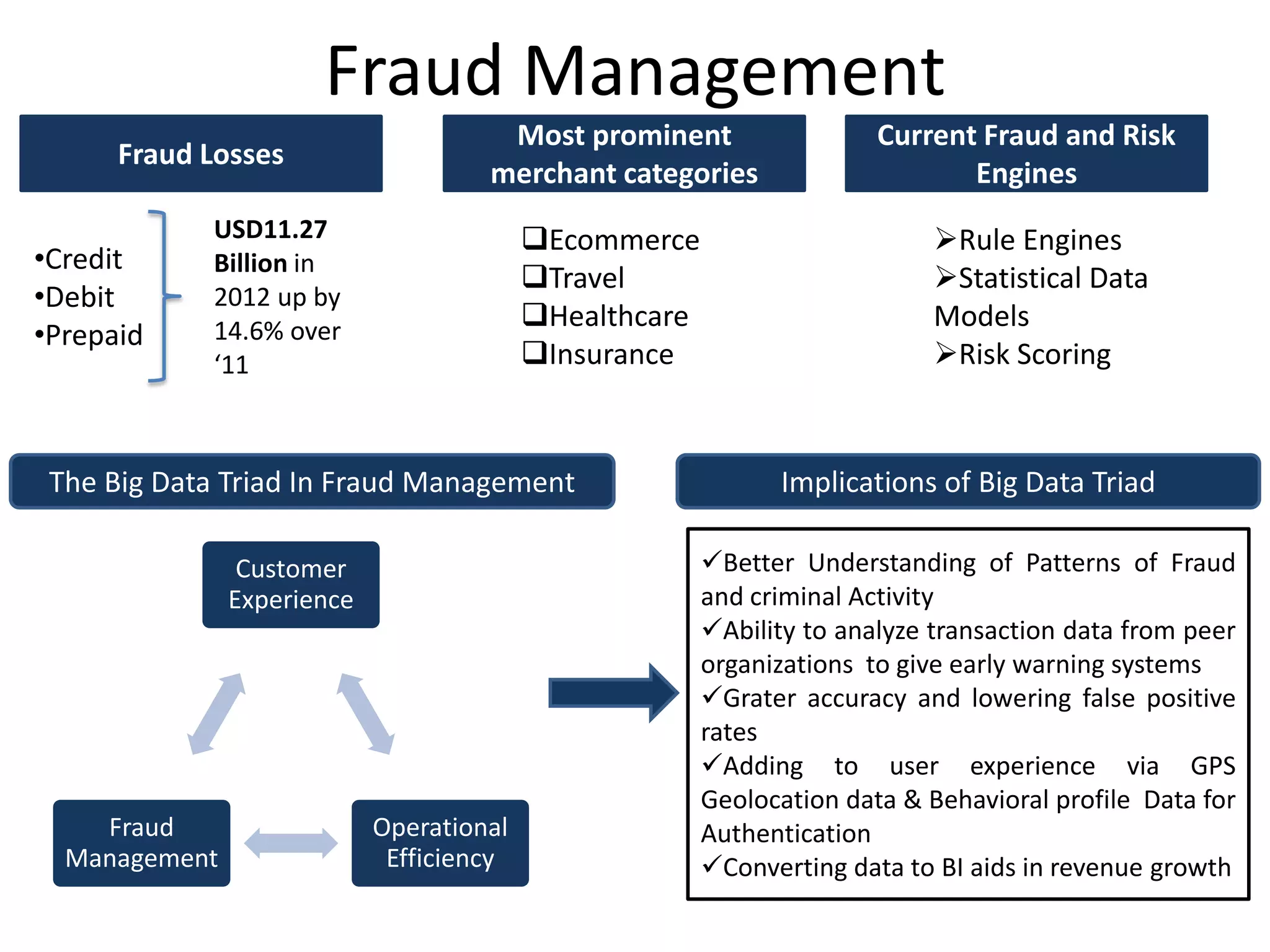

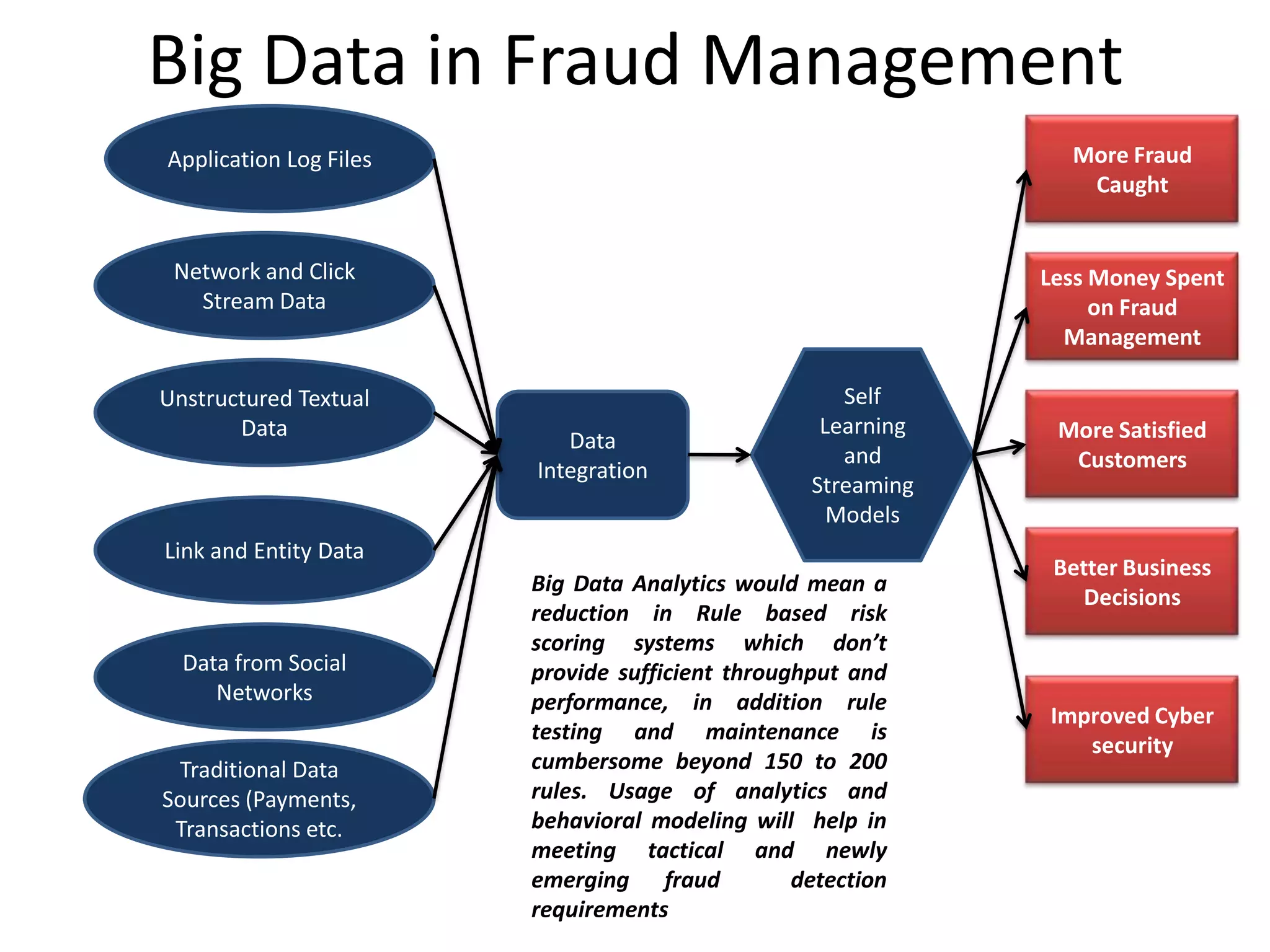

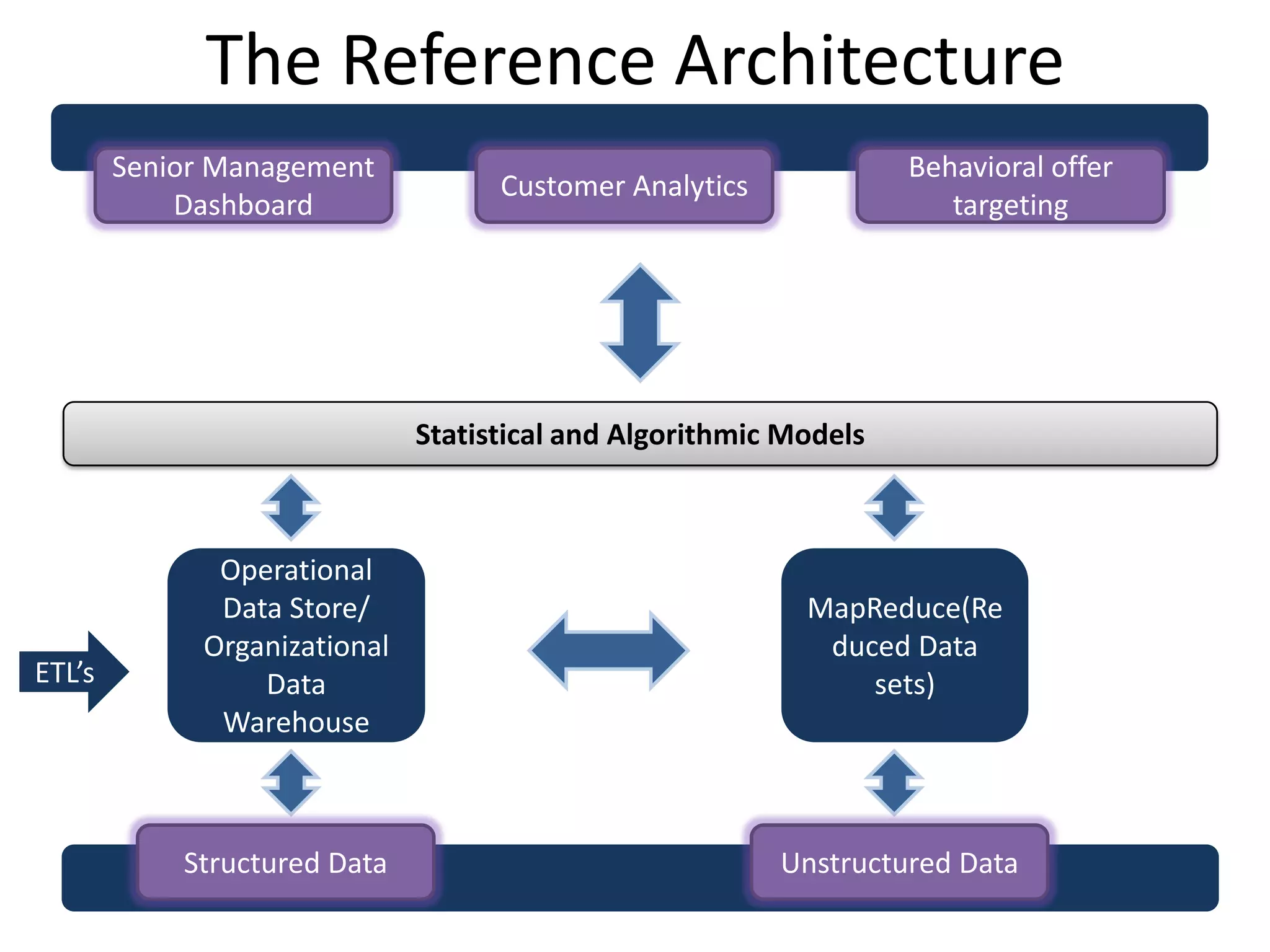

Big data analytics can provide acquirers with revenue advantages, improved knowledge of customer needs, and greater operational efficiencies. It allows for enhanced fraud management, loyalty programs, and merchant services through analysis of large, diverse transaction datasets. Realizing these benefits requires integrating multiple data sources and deploying analytical tools to glean insights from both structured and unstructured payment information.