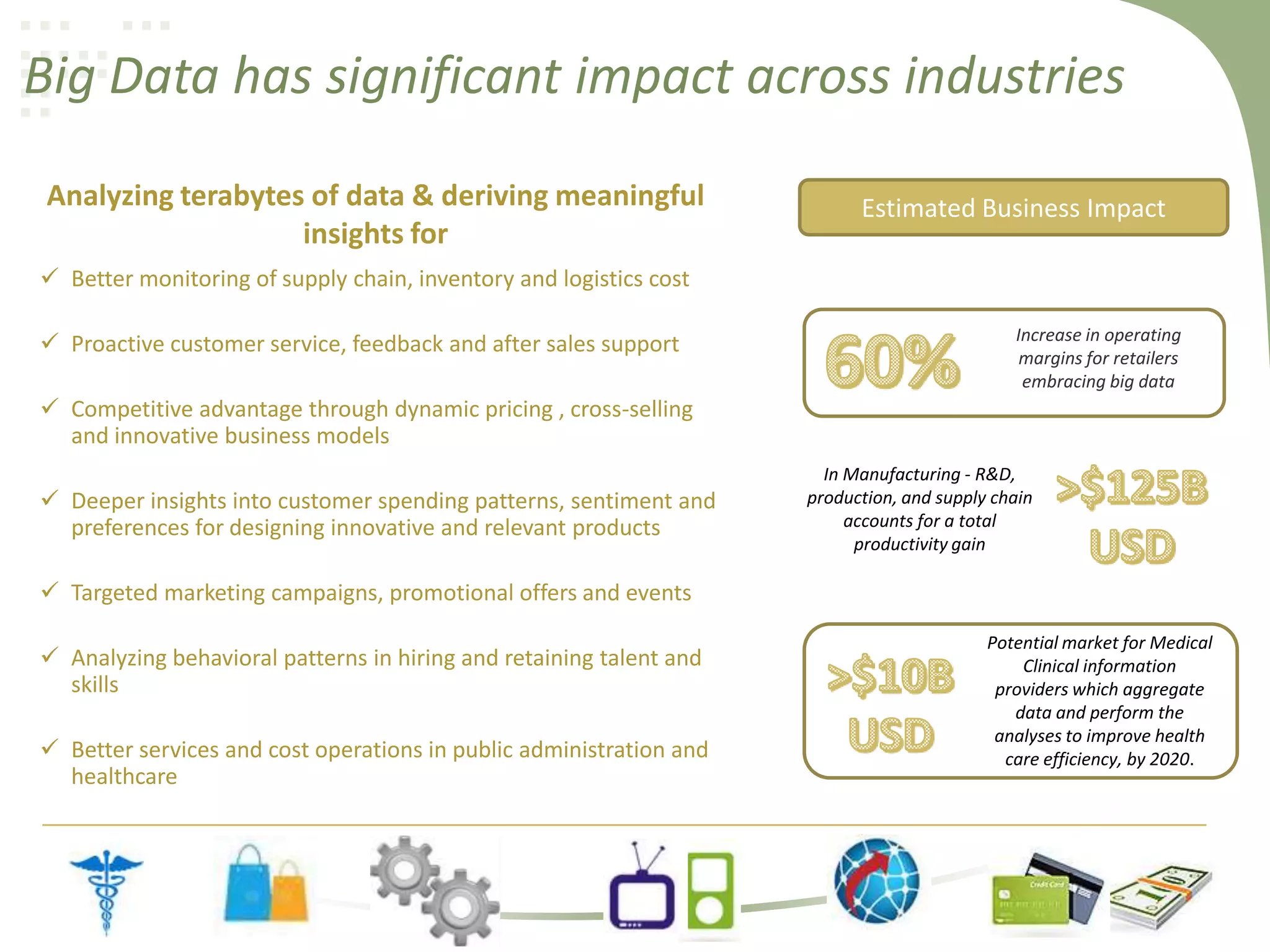

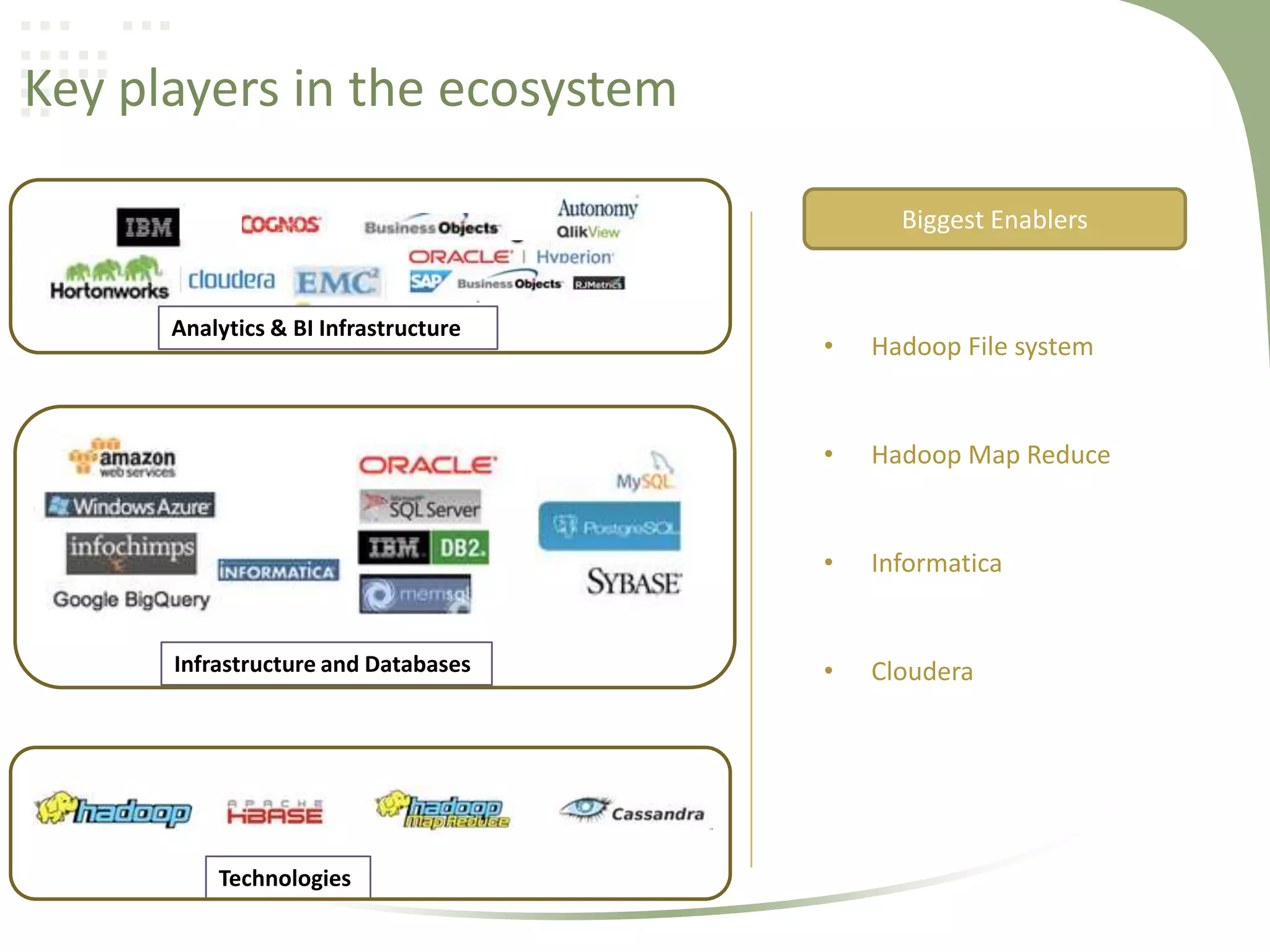

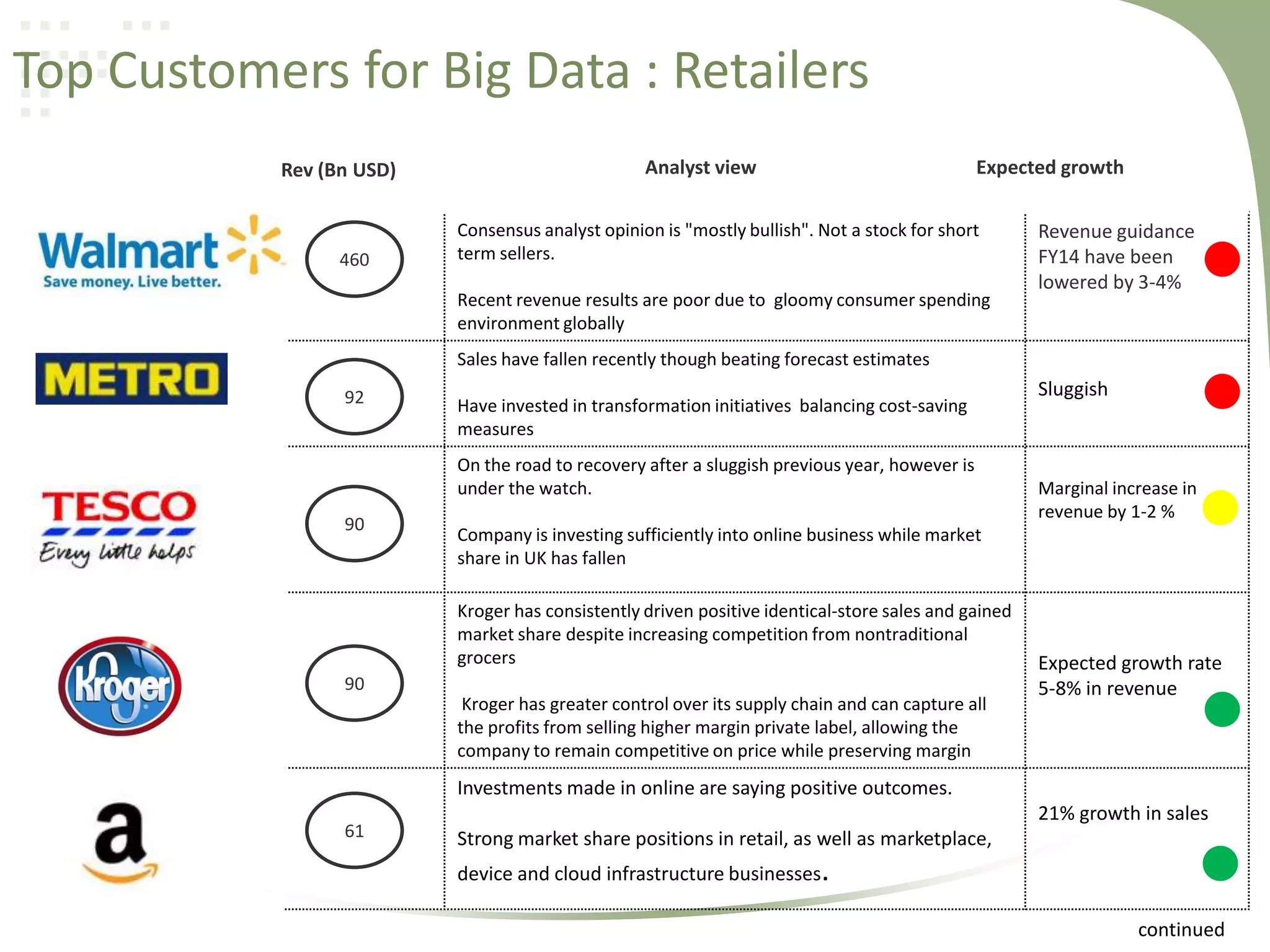

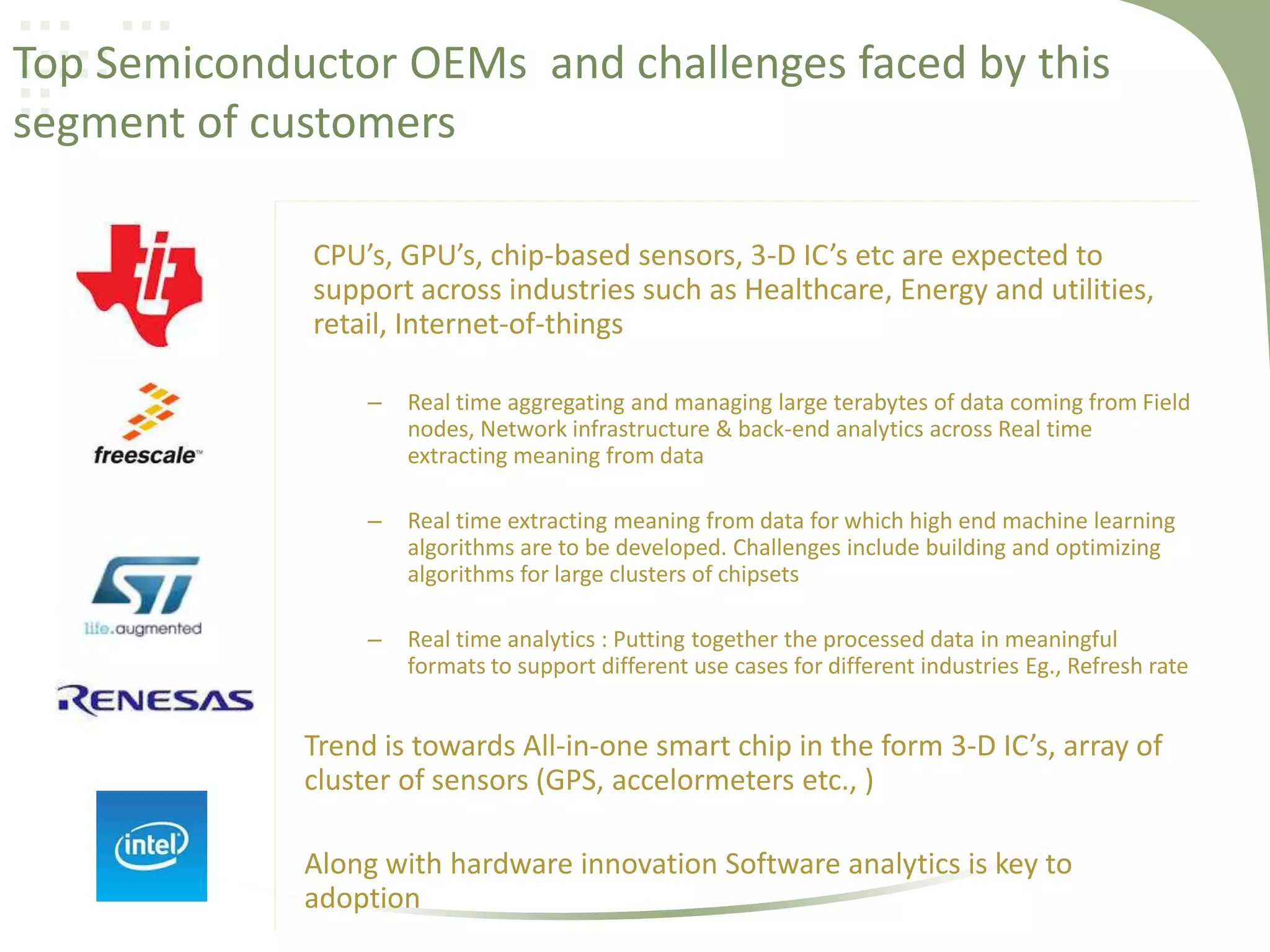

The assessment report discusses trends and challenges in big data, cloud computing, and medical devices, outlining their key players, customer challenges, and market opportunities. It highlights the significant impact of big data across industries, the cost-saving advantages of cloud computing, and the growth prospects in the medical device market amid regulatory and economic pressures. The report also emphasizes the need for technological advancements and integration strategies to optimize these sectors.

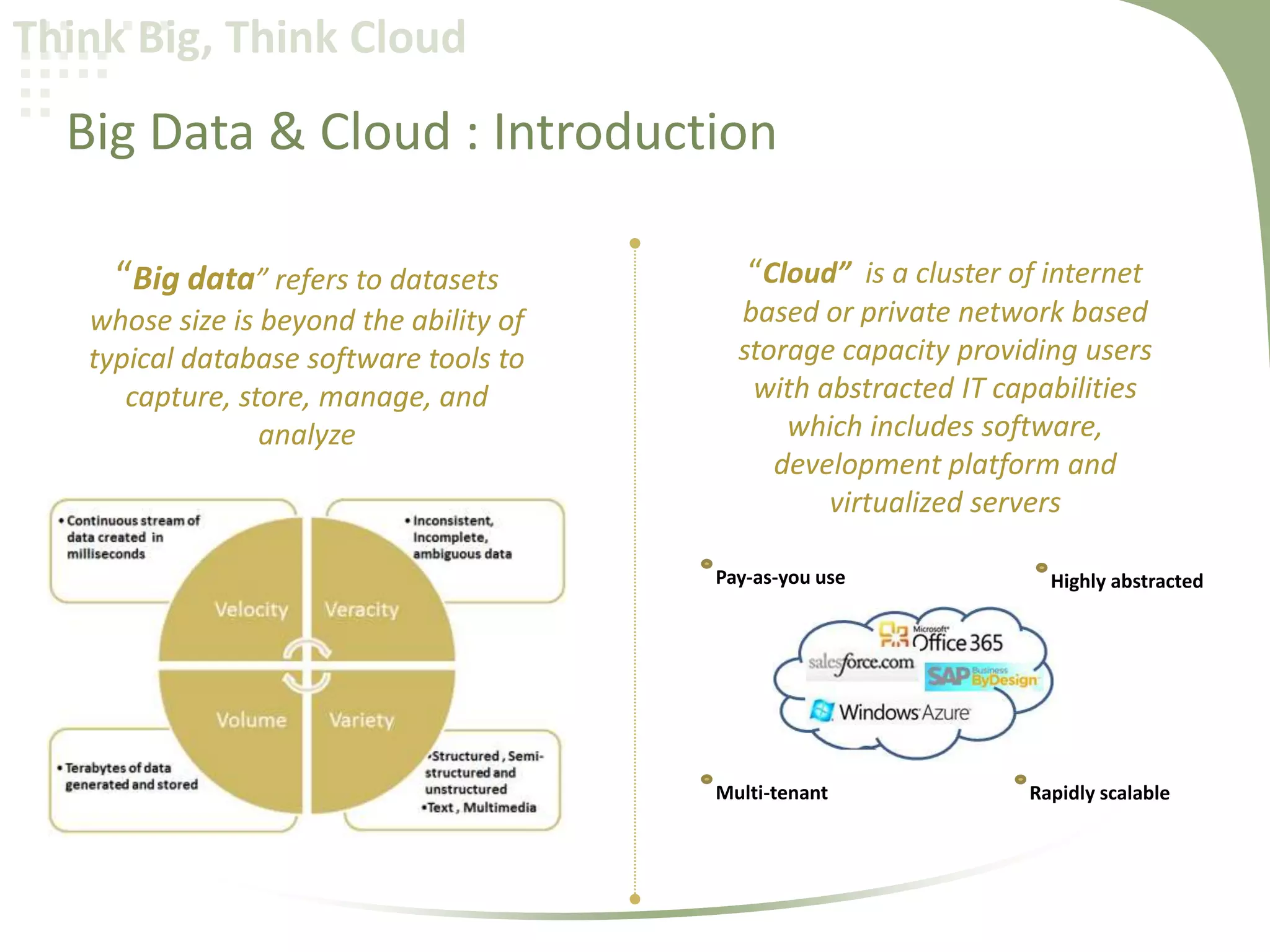

![Trends & Challenges: Big Data

Storage

Massive spurt in digital data after 2000

(from 25% in 2000 to 94% in 2007)

Content

– Expansion in multimedia content

– Increasing popularity in social media

– Proliferation in use of sensors in

Internet of Things

Investments

Big Data investment are geared towards

generating and maintaining revenue

[Sales, Marketing, Customer service, R&D]

Data usage Policy

• Data Privacy , Intellectual property rights

• Data security

Shortage of skills

• To derive insights from big data

• Demand for deep analytical talent in the US could be 50-60%

greater than its projected supply by 2018

Technology and Analyses techniques

• Deploy new technology (storage computing & analytical

software, analytic techniques)

• Upgrade legacy systems & incompatible standards for

integration

Internet based business

Industries generating revenues over

Internet spend the most (>75%) on Big

Data

Big data & Meaningful content

• Large tracts of data is unstructured and in inaccessible form

• Organizational structures & workflows not aligned to optimize

use of big data](https://image.slidesharecdn.com/bigdata-131228015548-phpapp01/75/Big-data-6-2048.jpg)

![IIR_conferentie_1.2[1]](https://cdn.slidesharecdn.com/ss_thumbnails/5e711ff2-6399-41cc-a31b-ca80aa315ffd-160121133537-thumbnail.jpg?width=640&height=640&fit=bounds)

![[BLT] 고벤처포럼 - 스타트업과 특허전략](https://cdn.slidesharecdn.com/ss_thumbnails/bltstartupip26-160628085136-thumbnail.jpg?width=640&height=640&fit=bounds)