Be A Tax Return Filer

•Download as PPTX, PDF•

0 likes•88 views

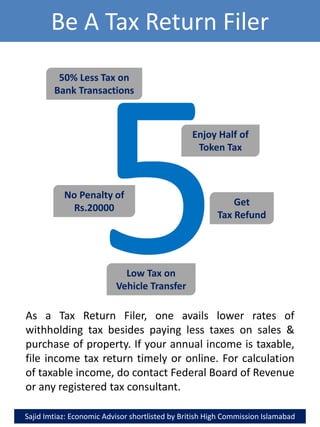

There are 1 Million active taxpayers out of 207 Million Pakistanis. It is good to be a tax return filer to enjoy financial benefits. (Sajid Imtiaz)

Report

Share

Report

Share

Recommended

The morality of tax avoidance

There are two videos in PPT, where are black slides:

Video1: https://www.youtube.com/watch?v=wxW8GP59Sq8

Video 2: https://www.youtube.com/watch?v=VcZF_DxQ5cU

Tax evasion & Tax avoidance

This document defines and compares tax evasion and tax avoidance. Tax evasion is illegal and involves intentionally avoiding taxes by not reporting all income or hiding funds. Tax avoidance uses legal tax deductions and loopholes to reduce tax liability. Causes of tax evasion include weak enforcement, corruption, complex laws, and high tax rates. Common evasion practices are under-reporting income, bribery, and lobbying governments. Tax avoidance uses legal deductions and planning to postpone or lower taxes owed. India loses $314 billion annually to tax evasion, which deprives the country of funds for infrastructure and reduces economic growth.

tax avoidence

Tax avoidance means neglecting to pay taxes that are owed. It is commonly practiced by multinational companies using tax havens to hide profits. While some tax avoidance has existed since the 1920s, it has grown significantly in recent decades, costing governments $50-200 billion in lost revenue annually. Poor countries have struggled to raise sufficient tax revenue due to tax competition between governments and trade liberalization policies that shift more of the tax burden onto poor individuals through consumption taxes. Tax havens undermine market competition and capital investment by allowing wealthy individuals and companies to escape taxation, and enable political corruption through secret bank accounts.

Gst, black money & tx evasion

This document discusses GST, black money, and tax evasion in India. It provides details on key aspects of GST including how it will replace existing indirect taxes, make the country a single market, and simplify compliance. It also describes common sources of black money such as illegal activities and defines tax evasion as illegal non-payment or underpayment of taxes through misrepresentation or false reporting. Common tax evasion techniques like smuggling, fake receipts, and personal expenses claimed as business costs are outlined.

Tax evasion

India loses over $314 billion annually to tax evasion, including $314 billion from uncollected income taxes and $800 billion from corporate tax incentives. Tax evasion occurs through weak enforcement systems, corruption, complex laws, and methods like overstating expenses and underreporting income. While some large companies and trusts have been caught evading taxes, overall tax evasion remains a major problem as only about 36 million of India's 1.3 billion people pay income taxes. Efforts to curb evasion through new laws and whistleblower rewards have had limited success.

Tackling Tax Avoidance

Tax is a crucial revenue stream for administrations across the world.

While many agencies have already established processes for compliance and enforcement, a combination of avoidance and error is still costing governments billions.

Detection and Prevention measures provide the key to tackling these challenges

Tax Fraud

Tax fraud occurs when an individual or entity underreports income or overstates deductions on a tax return to reduce the amount of taxes owed. In India, major areas of tax fraud include falsification of invoices, unreported income, and bribery of tax officials. The Indian government estimates an annual loss of 14 trillion rupees from tax evasion. Recent government efforts to curb fraud include new laws targeting undisclosed foreign assets, a proposed nationwide goods and services tax, and increased use of technology in tax administration. However, tax fraud remains a significant problem in India due to complex tax laws, weak enforcement, and corruption. Simplification of the tax system and improved monitoring are needed to further reduce the prevalence of tax evasion.

Convertibility of Black money to white

Black money refers to funds earned on the books but unreported to avoid taxes. It exists due to factors like high taxes, corruption, and perceptions of government. Black money has grown significantly in India, estimated at 25-50% of GDP in developing countries. While some argue black money improves well-being and entrepreneurship, it undermines the tax system, economic forecasts, and public confidence. Past tax amnesty programs in India have had varying success in generating tax revenue from unreported funds. Moving forward, policies aim to curb black money through increased audits, incentives for legal transactions, and simplified tax compliance.

Recommended

The morality of tax avoidance

There are two videos in PPT, where are black slides:

Video1: https://www.youtube.com/watch?v=wxW8GP59Sq8

Video 2: https://www.youtube.com/watch?v=VcZF_DxQ5cU

Tax evasion & Tax avoidance

This document defines and compares tax evasion and tax avoidance. Tax evasion is illegal and involves intentionally avoiding taxes by not reporting all income or hiding funds. Tax avoidance uses legal tax deductions and loopholes to reduce tax liability. Causes of tax evasion include weak enforcement, corruption, complex laws, and high tax rates. Common evasion practices are under-reporting income, bribery, and lobbying governments. Tax avoidance uses legal deductions and planning to postpone or lower taxes owed. India loses $314 billion annually to tax evasion, which deprives the country of funds for infrastructure and reduces economic growth.

tax avoidence

Tax avoidance means neglecting to pay taxes that are owed. It is commonly practiced by multinational companies using tax havens to hide profits. While some tax avoidance has existed since the 1920s, it has grown significantly in recent decades, costing governments $50-200 billion in lost revenue annually. Poor countries have struggled to raise sufficient tax revenue due to tax competition between governments and trade liberalization policies that shift more of the tax burden onto poor individuals through consumption taxes. Tax havens undermine market competition and capital investment by allowing wealthy individuals and companies to escape taxation, and enable political corruption through secret bank accounts.

Gst, black money & tx evasion

This document discusses GST, black money, and tax evasion in India. It provides details on key aspects of GST including how it will replace existing indirect taxes, make the country a single market, and simplify compliance. It also describes common sources of black money such as illegal activities and defines tax evasion as illegal non-payment or underpayment of taxes through misrepresentation or false reporting. Common tax evasion techniques like smuggling, fake receipts, and personal expenses claimed as business costs are outlined.

Tax evasion

India loses over $314 billion annually to tax evasion, including $314 billion from uncollected income taxes and $800 billion from corporate tax incentives. Tax evasion occurs through weak enforcement systems, corruption, complex laws, and methods like overstating expenses and underreporting income. While some large companies and trusts have been caught evading taxes, overall tax evasion remains a major problem as only about 36 million of India's 1.3 billion people pay income taxes. Efforts to curb evasion through new laws and whistleblower rewards have had limited success.

Tackling Tax Avoidance

Tax is a crucial revenue stream for administrations across the world.

While many agencies have already established processes for compliance and enforcement, a combination of avoidance and error is still costing governments billions.

Detection and Prevention measures provide the key to tackling these challenges

Tax Fraud

Tax fraud occurs when an individual or entity underreports income or overstates deductions on a tax return to reduce the amount of taxes owed. In India, major areas of tax fraud include falsification of invoices, unreported income, and bribery of tax officials. The Indian government estimates an annual loss of 14 trillion rupees from tax evasion. Recent government efforts to curb fraud include new laws targeting undisclosed foreign assets, a proposed nationwide goods and services tax, and increased use of technology in tax administration. However, tax fraud remains a significant problem in India due to complex tax laws, weak enforcement, and corruption. Simplification of the tax system and improved monitoring are needed to further reduce the prevalence of tax evasion.

Convertibility of Black money to white

Black money refers to funds earned on the books but unreported to avoid taxes. It exists due to factors like high taxes, corruption, and perceptions of government. Black money has grown significantly in India, estimated at 25-50% of GDP in developing countries. While some argue black money improves well-being and entrepreneurship, it undermines the tax system, economic forecasts, and public confidence. Past tax amnesty programs in India have had varying success in generating tax revenue from unreported funds. Moving forward, policies aim to curb black money through increased audits, incentives for legal transactions, and simplified tax compliance.

Tax evasion and avoidance

This document discusses tax evasion and avoidance. It defines tax as a financial charge imposed by governments to fund public expenditures. Direct taxes are levied on personal income, while indirect taxes are levied on goods and services. Tax evasion is illegally not paying taxes when they are due, while tax avoidance uses legal loopholes to reduce taxes owed. Common methods of evasion include failing to pay taxes, smuggling, and falsifying financial statements. Tax evasion harms economies by reducing government revenues. To reduce evasion, governments can simplify tax laws, increase awareness, and strengthen penalties for noncompliance.

Amarakoon-Zimbabwe Economic Review

This document discusses reforms to ease the cost of doing business in Zimbabwe in order to increase liquidity and build reserves through foreign and domestic investment. It analyzes Zimbabwe's rankings in the World Bank's Ease of Doing Business report, noting areas that need improvement such as starting a business, construction permits, and contract enforcement. The document recommends policy reforms like strengthening property rights and the rule of law to boost safety of capital. It also suggests improving access to credit, labor costs, and regulatory efficiency to increase investment returns. Overall, the document advocates restoring confidence through transparent policies and credible financial, labor, and public sector reforms to attract more foreign and domestic investment.

Ethical issues in tax evasion ppt

ethical issues in tax evasion. In business, theres always a situation where one has to choose one of the 2 things:

1) ethics 2) profits

one has to decide whether profits are more important than ethics

TAX AVOIDANCE AND TAX EVASION -DIFFERENCE AND EFFECT ON INDIAN ECONOMY

Tax avoidance is the legal minimization of tax liability by taking advantage of loopholes and ambiguities in tax laws, while tax evasion is the illegal non-payment or underpayment of taxes by hiding income or making false claims. While tax avoidance is legal, tax evasion is a criminal offense. Tax evasion reduces government revenue and increases inflation, impacting India's economic growth and development. It also increases corruption and wealth inequality between rich and poor.

Pay As You Go (Payg) Final

Pay As You Go (PAYG) is Australia's system for regularly collecting income tax from earnings during the income year. There are two parts to PAYG - withholdings from payments to others like salaries, and installments paid by individuals and businesses on their own income. PAYG collects tax prepayments that are credited towards taxpayers' annual tax liability. Eligible taxpayers must pay quarterly installments that are calculated based on their business and investment income. Penalties may apply for non-compliance with PAYG obligations.

Business Activity Statement Presentation

The document discusses the Business Activity Statement (BAS) and various Australian taxation obligations reported on the BAS, including:

- Goods and Services Tax (GST)

- Pay As You Go Withholding (PAYGW)

- Pay As You Go Installments (PAYGI)

- Fringe Benefits Tax (FBT)

- Wine Equalization Tax (WET)

- Luxury Car Tax (LCT)

It provides details on what information is included in the BAS, who needs to complete one, payment periods, and lodging deadlines. It also gives overviews of each of the different tax types listed above.

Tax avoidance 5.4

Tax planning involves legally arranging one's financial affairs to minimize tax liability, while complying with all applicable tax laws. Tax avoidance uses artificial or dubious methods to reduce taxes in a manner that defeats the intent of tax statutes. Tax evasion illegally avoids taxes through actions like knowingly making untrue statements or omitting required information. The line between tax planning and avoidance is thin, with avoidance including an element of mala fide intent or use of "colorable devices" to circumvent the spirit of tax laws.

Tax evasion

This document discusses tax evasion in the Philippines. It defines tax evasion as the criminal act of deliberately failing to pay tax liability. People who commit tax evasion face criminal charges and penalties such as jail time and fines. The document then discusses various tax revenues in the Philippines including income tax, excise tax, franchise taxes, and import duties. It provides examples of high-profile tax evasion cases in the country. Finally, it discusses what counts as tax evasion and common types of tax evasion such as tax fraud, abusive tax schemes, and employment tax fraud.

David Stewart Tax Evasion

David Stewart Tax Evasion: What is tax evasion? What are tax evasion penalties? What are some celebrities who have been charged with tax evasion? Take a look!

BENEFIT OF LOWER TAX RATE OF INCOME TAX ON DIGITAL TURNOVER FOR SMALL BUSINES...

Measures for promoting Digital payments & Creation of Less Cash Economy:

BENEFIT OF LOWER TAX RATE OF INCOME TAX ON DIGITAL TURNOVER FOR SMALL BUSINESSES.

Tax planning

This document discusses different methods taxpayers can use to reduce their tax liability: tax evasion, tax avoidance, and tax planning. Tax evasion involves illegally hiding income or falsifying records. Tax avoidance aims to reduce taxes through legal but questionable loopholes. In contrast, tax planning makes legitimate use of exemptions, deductions, and other provisions in the tax code to lower tax burden. Proper tax planning is an encouraged way for taxpayers to minimize their liability within the law.

Tax evasion a_forensicexpertsviewpoint_gfsu

This document discusses tax evasion from the perspective of a forensic expert. It begins by defining tax evasion and tax avoidance, noting that the latter involves legally minimizing taxes while the former involves illegal means. Next, it compares tax evasion and avoidance and examines reasons for the tax gap in the UK. It then looks at global tax evasion by profession and discusses long-term remedies like tax planning and management. The document outlines ways that tax evasion occurs and who is responsible in India. It also examines some attempts at tax evasion during India's demonetization and concludes by emphasizing the importance of tax planning to curb evasion.

Tax Planning, Tax Evasion, Tax Avoidance,

This document discusses different methods for taxpayers to minimize tax liability: tax planning, tax avoidance, and tax evasion. Tax planning involves legally taking advantage of exemptions, deductions, and rebates to reduce taxes. Tax avoidance also reduces taxes legally by exploiting loopholes. Tax evasion illegally underreports income or falsifies information to pay less tax than owed. The document provides examples of actions considered tax planning, such as certain investments, and tax evasion, like falsely claiming donations. Overall it aims to explain legal and illegal options and their objectives in paying the minimum required tax.

Sales Tax Compliance and Automation with Vertex SMB

This webinar discusses sales and use tax solutions. It is roughly 1 hour long with Mary Orefice presenting. Attendees are asked to type any questions in the question box. The webinar discusses common myths about sales tax, a case of a company failing to collect sales tax, and provides an overview of sales tax rates across states. It also summarizes Vertex SMB software which can help with sales tax calculation, management of tax rates and certificates, and generating returns.

Tax Evasion and Methods of Avoiding Tax

This document discusses tax evasion and avoidance. It provides data on various individuals' PTP scores and ways that people evade taxes such as smuggling, submitting false returns, and claiming personal expenses as business expenses. It also lists penalties for tax evasion ranging from 100-300% of unpaid taxes to Rs. 5000 for not filing returns. The document identifies limitations of the Indian tax structure that contribute to evasion, such as high taxation rates, corruption, and frequent changes in government. It defines tax avoidance as the legal exploitation of tax regulations to minimize taxes owed.

Property Tax Article 3

The document discusses issues with New Zealand's proposed Resident Land Withholding Tax. It summarizes that the proposed tax rates of 33% of profit or 10% of sale price are excessively high and could double or quadruple taxpayers' current tax liabilities. It provides examples showing the proposed tax is much higher than the actual tax owed. It argues the tax places undue burden on conveyancing agents and may leave creditors out of pocket if it takes priority over other loans. It calls for the officials to refine the policy to ensure a more reasonable tax system is implemented.

Public revenue

The document discusses the major and minor sources of revenue for the government. Major sources include taxes and prices, while minor sources are fees, special assessments, rates, fines, tributes, and indemnities. It then defines different types of taxes - direct and indirect taxes, proportional, progressive, regressive, and degressive taxes. It also defines prices, fees, special assessments, rates, fines, tributes, indemnities and other principles of taxation including equality, sacrifice, certainty, convenience, economy, fiscal adequacy, elasticity, flexibility, diversity, and neutrality.

GoCoin Presentation to SM Rotary Club (LAVA)

GoCoin (Bitcoin, Litecoin, Dogecoin payment processor) presentation to the Rotary Club of Santa Monica at the Riviera CC Friday, Aug 8, 2014. Presented by Steve Beauregard

A guide to vat on uber eats and reverse charges

Uber is able to escape VAT by making use of a gap in how tax is gathered for cross-EU company sales. This stems from the fact that it classifies its 40,000 UK drivers as independent entities, each too small to register for VAT. Read on to learn about VAT on UberEats, reverse charges and more.

Board of Directors of OGDCL 2023

Oil & Gas Development Company Limited (OGDCL), a profitable leading company of Pakistan is also listed on London Stock Exchange. (Sajid Imtiaz)

Top 10 Problems in Lahore

Capital of Punjab, Lahore has been facing myriad of problems like Air Pollution, Contaminated Food, Urbanization, Street Beggars, etc. (Sajid Imtiaz)

Biz Milestone of Pakistan

Owing to efficient Securities and Exchange Commission of Pakistan, total registered companies in Pakistan are over two hundred thousand by August 2023. (Sajid Imtiaz)

More Related Content

What's hot

Tax evasion and avoidance

This document discusses tax evasion and avoidance. It defines tax as a financial charge imposed by governments to fund public expenditures. Direct taxes are levied on personal income, while indirect taxes are levied on goods and services. Tax evasion is illegally not paying taxes when they are due, while tax avoidance uses legal loopholes to reduce taxes owed. Common methods of evasion include failing to pay taxes, smuggling, and falsifying financial statements. Tax evasion harms economies by reducing government revenues. To reduce evasion, governments can simplify tax laws, increase awareness, and strengthen penalties for noncompliance.

Amarakoon-Zimbabwe Economic Review

This document discusses reforms to ease the cost of doing business in Zimbabwe in order to increase liquidity and build reserves through foreign and domestic investment. It analyzes Zimbabwe's rankings in the World Bank's Ease of Doing Business report, noting areas that need improvement such as starting a business, construction permits, and contract enforcement. The document recommends policy reforms like strengthening property rights and the rule of law to boost safety of capital. It also suggests improving access to credit, labor costs, and regulatory efficiency to increase investment returns. Overall, the document advocates restoring confidence through transparent policies and credible financial, labor, and public sector reforms to attract more foreign and domestic investment.

Ethical issues in tax evasion ppt

ethical issues in tax evasion. In business, theres always a situation where one has to choose one of the 2 things:

1) ethics 2) profits

one has to decide whether profits are more important than ethics

TAX AVOIDANCE AND TAX EVASION -DIFFERENCE AND EFFECT ON INDIAN ECONOMY

Tax avoidance is the legal minimization of tax liability by taking advantage of loopholes and ambiguities in tax laws, while tax evasion is the illegal non-payment or underpayment of taxes by hiding income or making false claims. While tax avoidance is legal, tax evasion is a criminal offense. Tax evasion reduces government revenue and increases inflation, impacting India's economic growth and development. It also increases corruption and wealth inequality between rich and poor.

Pay As You Go (Payg) Final

Pay As You Go (PAYG) is Australia's system for regularly collecting income tax from earnings during the income year. There are two parts to PAYG - withholdings from payments to others like salaries, and installments paid by individuals and businesses on their own income. PAYG collects tax prepayments that are credited towards taxpayers' annual tax liability. Eligible taxpayers must pay quarterly installments that are calculated based on their business and investment income. Penalties may apply for non-compliance with PAYG obligations.

Business Activity Statement Presentation

The document discusses the Business Activity Statement (BAS) and various Australian taxation obligations reported on the BAS, including:

- Goods and Services Tax (GST)

- Pay As You Go Withholding (PAYGW)

- Pay As You Go Installments (PAYGI)

- Fringe Benefits Tax (FBT)

- Wine Equalization Tax (WET)

- Luxury Car Tax (LCT)

It provides details on what information is included in the BAS, who needs to complete one, payment periods, and lodging deadlines. It also gives overviews of each of the different tax types listed above.

Tax avoidance 5.4

Tax planning involves legally arranging one's financial affairs to minimize tax liability, while complying with all applicable tax laws. Tax avoidance uses artificial or dubious methods to reduce taxes in a manner that defeats the intent of tax statutes. Tax evasion illegally avoids taxes through actions like knowingly making untrue statements or omitting required information. The line between tax planning and avoidance is thin, with avoidance including an element of mala fide intent or use of "colorable devices" to circumvent the spirit of tax laws.

Tax evasion

This document discusses tax evasion in the Philippines. It defines tax evasion as the criminal act of deliberately failing to pay tax liability. People who commit tax evasion face criminal charges and penalties such as jail time and fines. The document then discusses various tax revenues in the Philippines including income tax, excise tax, franchise taxes, and import duties. It provides examples of high-profile tax evasion cases in the country. Finally, it discusses what counts as tax evasion and common types of tax evasion such as tax fraud, abusive tax schemes, and employment tax fraud.

David Stewart Tax Evasion

David Stewart Tax Evasion: What is tax evasion? What are tax evasion penalties? What are some celebrities who have been charged with tax evasion? Take a look!

BENEFIT OF LOWER TAX RATE OF INCOME TAX ON DIGITAL TURNOVER FOR SMALL BUSINES...

Measures for promoting Digital payments & Creation of Less Cash Economy:

BENEFIT OF LOWER TAX RATE OF INCOME TAX ON DIGITAL TURNOVER FOR SMALL BUSINESSES.

Tax planning

This document discusses different methods taxpayers can use to reduce their tax liability: tax evasion, tax avoidance, and tax planning. Tax evasion involves illegally hiding income or falsifying records. Tax avoidance aims to reduce taxes through legal but questionable loopholes. In contrast, tax planning makes legitimate use of exemptions, deductions, and other provisions in the tax code to lower tax burden. Proper tax planning is an encouraged way for taxpayers to minimize their liability within the law.

Tax evasion a_forensicexpertsviewpoint_gfsu

This document discusses tax evasion from the perspective of a forensic expert. It begins by defining tax evasion and tax avoidance, noting that the latter involves legally minimizing taxes while the former involves illegal means. Next, it compares tax evasion and avoidance and examines reasons for the tax gap in the UK. It then looks at global tax evasion by profession and discusses long-term remedies like tax planning and management. The document outlines ways that tax evasion occurs and who is responsible in India. It also examines some attempts at tax evasion during India's demonetization and concludes by emphasizing the importance of tax planning to curb evasion.

Tax Planning, Tax Evasion, Tax Avoidance,

This document discusses different methods for taxpayers to minimize tax liability: tax planning, tax avoidance, and tax evasion. Tax planning involves legally taking advantage of exemptions, deductions, and rebates to reduce taxes. Tax avoidance also reduces taxes legally by exploiting loopholes. Tax evasion illegally underreports income or falsifies information to pay less tax than owed. The document provides examples of actions considered tax planning, such as certain investments, and tax evasion, like falsely claiming donations. Overall it aims to explain legal and illegal options and their objectives in paying the minimum required tax.

Sales Tax Compliance and Automation with Vertex SMB

This webinar discusses sales and use tax solutions. It is roughly 1 hour long with Mary Orefice presenting. Attendees are asked to type any questions in the question box. The webinar discusses common myths about sales tax, a case of a company failing to collect sales tax, and provides an overview of sales tax rates across states. It also summarizes Vertex SMB software which can help with sales tax calculation, management of tax rates and certificates, and generating returns.

Tax Evasion and Methods of Avoiding Tax

This document discusses tax evasion and avoidance. It provides data on various individuals' PTP scores and ways that people evade taxes such as smuggling, submitting false returns, and claiming personal expenses as business expenses. It also lists penalties for tax evasion ranging from 100-300% of unpaid taxes to Rs. 5000 for not filing returns. The document identifies limitations of the Indian tax structure that contribute to evasion, such as high taxation rates, corruption, and frequent changes in government. It defines tax avoidance as the legal exploitation of tax regulations to minimize taxes owed.

Property Tax Article 3

The document discusses issues with New Zealand's proposed Resident Land Withholding Tax. It summarizes that the proposed tax rates of 33% of profit or 10% of sale price are excessively high and could double or quadruple taxpayers' current tax liabilities. It provides examples showing the proposed tax is much higher than the actual tax owed. It argues the tax places undue burden on conveyancing agents and may leave creditors out of pocket if it takes priority over other loans. It calls for the officials to refine the policy to ensure a more reasonable tax system is implemented.

Public revenue

The document discusses the major and minor sources of revenue for the government. Major sources include taxes and prices, while minor sources are fees, special assessments, rates, fines, tributes, and indemnities. It then defines different types of taxes - direct and indirect taxes, proportional, progressive, regressive, and degressive taxes. It also defines prices, fees, special assessments, rates, fines, tributes, indemnities and other principles of taxation including equality, sacrifice, certainty, convenience, economy, fiscal adequacy, elasticity, flexibility, diversity, and neutrality.

GoCoin Presentation to SM Rotary Club (LAVA)

GoCoin (Bitcoin, Litecoin, Dogecoin payment processor) presentation to the Rotary Club of Santa Monica at the Riviera CC Friday, Aug 8, 2014. Presented by Steve Beauregard

A guide to vat on uber eats and reverse charges

Uber is able to escape VAT by making use of a gap in how tax is gathered for cross-EU company sales. This stems from the fact that it classifies its 40,000 UK drivers as independent entities, each too small to register for VAT. Read on to learn about VAT on UberEats, reverse charges and more.

What's hot (19)

TAX AVOIDANCE AND TAX EVASION -DIFFERENCE AND EFFECT ON INDIAN ECONOMY

TAX AVOIDANCE AND TAX EVASION -DIFFERENCE AND EFFECT ON INDIAN ECONOMY

BENEFIT OF LOWER TAX RATE OF INCOME TAX ON DIGITAL TURNOVER FOR SMALL BUSINES...

BENEFIT OF LOWER TAX RATE OF INCOME TAX ON DIGITAL TURNOVER FOR SMALL BUSINES...

Sales Tax Compliance and Automation with Vertex SMB

Sales Tax Compliance and Automation with Vertex SMB

More from Daily 10 Minutes

Board of Directors of OGDCL 2023

Oil & Gas Development Company Limited (OGDCL), a profitable leading company of Pakistan is also listed on London Stock Exchange. (Sajid Imtiaz)

Top 10 Problems in Lahore

Capital of Punjab, Lahore has been facing myriad of problems like Air Pollution, Contaminated Food, Urbanization, Street Beggars, etc. (Sajid Imtiaz)

Biz Milestone of Pakistan

Owing to efficient Securities and Exchange Commission of Pakistan, total registered companies in Pakistan are over two hundred thousand by August 2023. (Sajid Imtiaz)

Khurshid Barlas

Khurshid Barlas is founder and chairman of Pakistan Association of Exhibition Industry (PAEI), President of UK Pakistan Business Council (Pakistan Chapter), Chairman of standing committees of Rawalpindi Chamber of Commerce & Industry and honorary member of AJK Board of Investment. (Sajid Imtiaz)

Image Inventor

As creative director, Sajid Imtiaz has been serving leading advertising agencies in Pakistan. Currently he is working in Enhancerz at Islamabad.

Pakistani Van Stops

Responsible citizens should make queue at van stops countrywide particularly for senior citizens. (Sajid Imtiaz)

Pre-Launch Discount Offer in Housing Schemes

At Pre-Launch phase in Pakistan, housing societies e.g. 7 Wonders Cities Islamabad and GC Homes Chakri Interchange are offering incentives to investors as marketing technique. (Sajid Imtiaz)

Investor-Friendly Housing Societies

GC Homes is offering a pre-launch promotion for its new housing society where buyers can receive free plots when purchasing plots. Specifically, buyers will get 1 free plot when buying 1 plot or 2 free plots when buying another plot. These types of buy one get one free offers are common marketing techniques used by developers during the pre-launch phase of new housing projects.

Sajid Imtiaz

Psychology-driven creative director Sajid Imtiaz focuses on using psychological principles to inform creative direction. His approach leverages an understanding of human behavior and decision-making to develop compelling and effective creative campaigns. Sajid aims to craft messaging that resonates with audiences on a deeper level through strategic use of psychology in creative works.

Leading 4 Business Sectors in Pakistan

Around 2017 new companies were registered during October 2021. Construction, Trading, IT and eCommerce are leading four sectors of economy. (Sajid Imtiaz)

New Companies in 4 Cities in July 2021

In Islamabad, Lahore, Karachi and Peshawar, 1693 new companies were registered during July 2021. Governments of Sindh and Khyber Pakhtunkhwa have to facilitate entrepreneurs. (Sajid Imtiaz)

Adnan Ahmed Mirza

A thoroughbred advertising professional, Adnan Mirza is successfully leading Time and Space Media in Islamabad since 2001. (Sajid Imtiaz)

4 Business Hubs of Pakistan

In Islamabad, Lahore, Karachi and Peshawar, 4101 new companies were registered during May-June 2021. Governments of Sindh and Khyber Pakhtunkhwa have to facilitate entrepreneurs. (Sajid Imtiaz)

3 Business Cities of Pakistan

Around 2504 new companies were registered throughout Pakistan in June 2021. Construction & Real Estate, Trading, IT, Services, eCommerce, Food & Beverages are steadily growing sectors in Pakistan. (Sajid Imtiaz)

3 Business Cities

Around 1597 new companies were registered throughout Pakistan in May 2021. Construction, Trading, IT, Services, Food and Beverages are steadily growing sectors in Pakistan. (Sajid Imtiaz)

Influencing Premier of Pakistan

Government of Pakistan is implementing some ideas e.g. Madina and Tourism presented online by Sajid Imtiaz.

Rising Corporate Pakistan

850 new companies registered in March 2021 in Islamabad, 751 in Lahore, and 385 in Karachi. Construction, Trading, IT, Services, Food and Beverages are steadily growing sectors in Pakistan according to Sajid Imtiaz, Associate Creative Director at Adage.

Rising Corporate Pakistan

Around 2257 new companies were registered throughout Pakistan in February 2021. Trading, IT, construction, services and real estate development are steadily growing sectors in Pakistan. (Sajid Imtiaz)

Corporate Pakistan

Around 2201 new companies were registered throughout Pakistan in January 2021. Trading, IT, construction, services and e-commerce are steadily growing sectors in Pakistan. (Sajid Imtiaz)

Two Economic Managers in Pakistan

Member Oil and Member Gas of OGRA (Oil and Gas Regulatory Authority) are the two most influential economic managers of Pakistan. (Sajid Imtiaz)

More from Daily 10 Minutes (20)

Recently uploaded

KYC Compliance: A Cornerstone of Global Crypto Regulatory Frameworks

This presentation explores the pivotal role of KYC compliance in shaping and enforcing global regulations within the dynamic landscape of cryptocurrencies. Dive into the intricate connection between KYC practices and the evolving legal frameworks governing the crypto industry.

13 Jun 24 ILC Retirement Income Summit - slides.pptx

ILC's Retirement Income Summit was hosted by M&G and supported by Canada Life. The event brought together key policymakers, influencers and experts to help identify policy priorities for the next Government and ensure more of us have access to a decent income in retirement.

Contributors included:

Jo Blanden, Professor in Economics, University of Surrey

Clive Bolton, CEO, Life Insurance M&G Plc

Jim Boyd, CEO, Equity Release Council

Molly Broome, Economist, Resolution Foundation

Nida Broughton, Co-Director of Economic Policy, Behavioural Insights Team

Jonathan Cribb, Associate Director and Head of Retirement, Savings, and Ageing, Institute for Fiscal Studies

Joanna Elson CBE, Chief Executive Officer, Independent Age

Tom Evans, Managing Director of Retirement, Canada Life

Steve Groves, Chair, Key Retirement Group

Tish Hanifan, Founder and Joint Chair of the Society of Later life Advisers

Sue Lewis, ILC Trustee

Siobhan Lough, Senior Consultant, Hymans Robertson

Mick McAteer, Co-Director, The Financial Inclusion Centre

Stuart McDonald MBE, Head of Longevity and Democratic Insights, LCP

Anusha Mittal, Managing Director, Individual Life and Pensions, M&G Life

Shelley Morris, Senior Project Manager, Living Pension, Living Wage Foundation

Sarah O'Grady, Journalist

Will Sherlock, Head of External Relations, M&G Plc

Daniela Silcock, Head of Policy Research, Pensions Policy Institute

David Sinclair, Chief Executive, ILC

Jordi Skilbeck, Senior Policy Advisor, Pensions and Lifetime Savings Association

Rt Hon Sir Stephen Timms, former Chair, Work & Pensions Committee

Nigel Waterson, ILC Trustee

Jackie Wells, Strategy and Policy Consultant, ILC Strategic Advisory Board

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck mari...

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck maria r mitchell.docx

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck maria r mitchell.docx

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck maria r mitchell.docx

International Sustainability Standards Board

Issb standards

New standard for reporting sustainability on lines of tcfd

快速制作美国迈阿密大学牛津分校毕业证文凭证书英文原版一模一样

原版一模一样【微信:741003700 】【美国迈阿密大学牛津分校毕业证文凭证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

South Dakota State University degree offer diploma Transcript

办理美国SDSU毕业证书制作南达科他州立大学假文凭定制Q微168899991做SDSU留信网教留服认证海牙认证改SDSU成绩单GPA做SDSU假学位证假文凭高仿毕业证GRE代考如何申请南达科他州立大学South Dakota State University degree offer diploma Transcript

The state of welfare Resolution Foundation Event

How has Britain’s safety net changed since 2010 and what comes next?

Economic Risk Factor Update: June 2024 [SlideShare]

May’s reports showed signs of continued economic growth, said Sam Millette, director, fixed income, in his latest Economic Risk Factor Update.

For more market updates, subscribe to The Independent Market Observer at https://blog.commonwealth.com/independent-market-observer.

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strategies

Fabular Frames and the Four Ratio Problem

Digital, interactive art showing the struggle of a society in providing for its present population while also saving planetary resources for future generations. Spread across several frames, the art is actually the rendering of real and speculative data. The stereographic projections change shape in response to prompts and provocations. Visitors interact with the model through speculative statements about how to increase savings across communities, regions, ecosystems and environments. Their fabulations combined with random noise, i.e. factors beyond control, have a dramatic effect on the societal transition. Things get better. Things get worse. The aim is to give visitors a new grasp and feel of the ongoing struggles in democracies around the world.

Stunning art in the small multiples format brings out the spatiotemporal nature of societal transitions, against backdrop issues such as energy, housing, waste, farmland and forest. In each frame we see hopeful and frightful interplays between spending and saving. Problems emerge when one of the two parts of the existential anaglyph rapidly shrinks like Arctic ice, as factors cross thresholds. Ecological wealth and intergenerational equity areFour at stake. Not enough spending could mean economic stress, social unrest and political conflict. Not enough saving and there will be climate breakdown and ‘bankruptcy’. So where does speculative design start and the gambling and betting end? Behind each fabular frame is a four ratio problem. Each ratio reflects the level of sacrifice and self-restraint a society is willing to accept, against promises of prosperity and freedom. Some values seem to stabilise a frame while others cause collapse. Get the ratios right and we can have it all. Get them wrong and things get more desperate.

Does teamwork really matter? Looking beyond the job posting to understand lab...

Does teamwork really matter? Looking beyond the job posting to understand lab...Labour Market Information Council | Conseil de l’information sur le marché du travail

Vicinity Jobs’ data includes more than three million 2023 OJPs and thousands of skills. Most skills appear in less than 0.02% of job postings, so most postings rely on a small subset of commonly used terms, like teamwork.

Laura Adkins-Hackett, Economist, LMIC, and Sukriti Trehan, Data Scientist, LMIC, presented their research exploring trends in the skills listed in OJPs to develop a deeper understanding of in-demand skills. This research project uses pointwise mutual information and other methods to extract more information about common skills from the relationships between skills, occupations and regions.Detailed power point presentation on compound interest and how it is calculated

Detailed information about compund interest

欧洲杯投注-欧洲杯投注买球-欧洲杯投注买球网|【网址🎉ac22.net🎉】

【网址🎉ac22.net🎉】欧洲杯投注 Sports 与其他博彩公司相比,其独特之处在于欧洲杯投注 Sports 基于低利润和高营业额的独一无二的体育博彩模式,该模式可以为玩家开出最高的赔率。欧洲杯投注的优势在于中文界面友好,接受人民币投注。他们的开户奖金和实时体育投注界面是大陆玩家的首选。

Using Online job postings and survey data to understand labour market trends

Using Online job postings and survey data to understand labour market trendsLabour Market Information Council | Conseil de l’information sur le marché du travail

[4:55 p.m.] Bryan Oates

OJPs are becoming a critical resource for policy-makers and researchers who study the labour market. LMIC continues to work with Vicinity Jobs’ data on OJPs, which can be explored in our Canadian Job Trends Dashboard. Valuable insights have been gained through our analysis of OJP data, including LMIC research lead

Suzanne Spiteri’s recent report on improving the quality and accessibility of job postings to reduce employment barriers for neurodivergent people.

Decoding job postings: Improving accessibility for neurodivergent job seekers

Improving the quality and accessibility of job postings is one way to reduce employment barriers for neurodivergent people.BIHC Briefing June 2024 from Bank+Insurance Hybrid Capital in association wit...

Our latest market and regulatory coverage and analysis

Ending stagnation: How to boost prosperity across Scotland

A toxic combination of 15 years of low growth, and four decades of high inequality, has left Britain poorer and falling behind its peers. Productivity growth is weak and public investment is low, while wages today are no higher than they were before the financial crisis. Britain needs a new economic strategy to lift itself out of stagnation.

Scotland is in many ways a microcosm of this challenge. It has become a hub for creative industries, is home to several world-class universities and a thriving community of businesses – strengths that need to be harness and leveraged. But it also has high levels of deprivation, with homelessness reaching a record high and nearly half a million people living in very deep poverty last year. Scotland won’t be truly thriving unless it finds ways to ensure that all its inhabitants benefit from growth and investment. This is the central challenge facing policy makers both in Holyrood and Westminster.

What should a new national economic strategy for Scotland include? What would the pursuit of stronger economic growth mean for local, national and UK-wide policy makers? How will economic change affect the jobs we do, the places we live and the businesses we work for? And what are the prospects for cities like Glasgow, and nations like Scotland, in rising to these challenges?

The Impact of Generative AI and 4th Industrial Revolution

This infographic explores the transformative power of Generative AI, a key driver of the 4th Industrial Revolution. Discover how Generative AI is revolutionizing industries, accelerating innovation, and shaping the future of work.

Recently uploaded (20)

KYC Compliance: A Cornerstone of Global Crypto Regulatory Frameworks

KYC Compliance: A Cornerstone of Global Crypto Regulatory Frameworks

13 Jun 24 ILC Retirement Income Summit - slides.pptx

13 Jun 24 ILC Retirement Income Summit - slides.pptx

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck mari...

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck mari...

South Dakota State University degree offer diploma Transcript

South Dakota State University degree offer diploma Transcript

Economic Risk Factor Update: June 2024 [SlideShare]

Economic Risk Factor Update: June 2024 [SlideShare]

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Does teamwork really matter? Looking beyond the job posting to understand lab...

Does teamwork really matter? Looking beyond the job posting to understand lab...

Detailed power point presentation on compound interest and how it is calculated

Detailed power point presentation on compound interest and how it is calculated

Using Online job postings and survey data to understand labour market trends

Using Online job postings and survey data to understand labour market trends

BIHC Briefing June 2024 from Bank+Insurance Hybrid Capital in association wit...

BIHC Briefing June 2024 from Bank+Insurance Hybrid Capital in association wit...

Ending stagnation: How to boost prosperity across Scotland

Ending stagnation: How to boost prosperity across Scotland

The Impact of Generative AI and 4th Industrial Revolution

The Impact of Generative AI and 4th Industrial Revolution

Be A Tax Return Filer

- 1. Be A Tax Return Filer Get Tax Refund No Penalty of Rs.20000 Low Tax on Vehicle Transfer 50% Less Tax on Bank Transactions Enjoy Half of Token Tax As a Tax Return Filer, one avails lower rates of withholding tax besides paying less taxes on sales & purchase of property. If your annual income is taxable, file income tax return timely or online. For calculation of taxable income, do contact Federal Board of Revenue or any registered tax consultant. Sajid Imtiaz: Economic Advisor shortlisted by British High Commission Islamabad