Downloaded 732 times

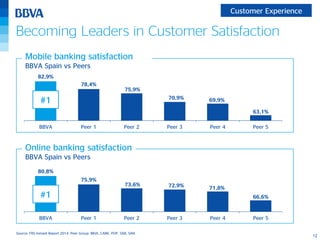

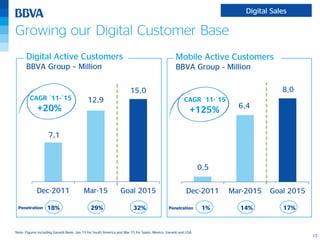

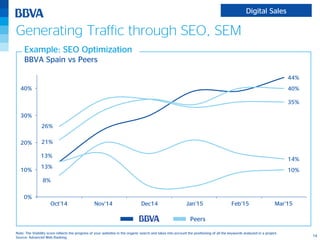

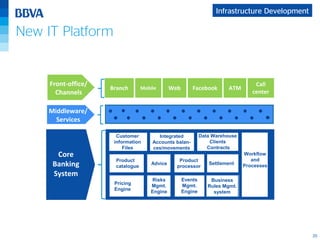

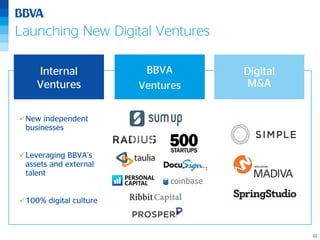

Ricardo Forcano of BBVA presented at the BoAML Digital Banking Revolution Conference in London on May 13, 2015. BBVA's digital strategy focuses on transforming its current business and launching new digital ventures. To transform its business, BBVA aims to become a leader in customer satisfaction for mobile and online banking, grow its digital customer base significantly, and generate additional sales through digital channels. BBVA is also optimizing its distribution model and developing a new IT platform. For new ventures, BBVA is launching independent digital businesses through ventures, acquisitions, and its BBVA Ventures program.