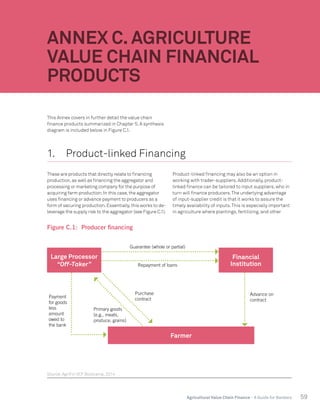

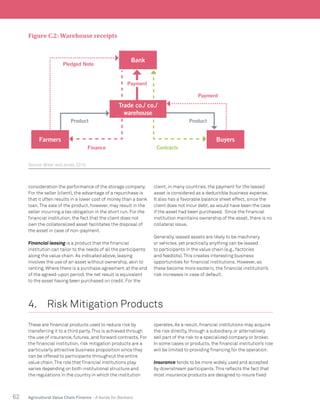

This document provides an introduction and overview of agricultural value chain finance (AVCF). It explains that understanding value chains can help banks identify opportunities to expand lending and services to new market segments in a profitable way. The document outlines the main participants in agricultural value chains and their typical financial needs. It also differentiates between "tight" and "loose" value chain relationships, and discusses internal versus external value chain finance approaches. The intended audience is financial institutions and practitioners interested in improving outreach and profitability through a value chain approach.

![70 Agricultural Value Chain Finance - A Guide for Bankers

References

ADB (African Development Bank). 2013. Agricultural Value Chain Financing (AVCF) and Development for Enhanced

Export Competitiveness. [Online] Available:

http://www.afdb.org/en/documents/document/agricultural-value-chain-financing-avcf-and-development-for-

enhanced-export-competitiveness-47028/

Agar,Jason. ACDI/VOCA. 2011. Rural and Agricultural Finance. USAID.

---. 2011. Rural and Agricultural Finance:Taking Stock of Five Years of Innovation. USAID.

AgriFin. 2012. Lessons from the Learning Visit to Banco Oportunidade Mozambique. Results Story, Maputo and

Chimoio:AgirFin.

Bankaool, AgriFin. 2016. Selecting a Target Value Chain – A Summary of Bankaool’s Market Study on the Vegetable

Value Chains in Mexico

Barrett, Christopher et al. 2012.“Smallholder participation in contract farming:comparative evidence from five

countries.” World Dev. 40(4):715–30.

Beaudoin, Christopher, and Esther Thorson. 2004.“Social capital in rural and urban communities:Testing

differences in media effects and models.” Journalism & Mass Communication Quarterly, 81(2), 378-399.

Bellemare, Marc F. 2012.“As You Sow, So Shall You Reap:The Welfare Impacts of Contract Farming.” World

Development, 40(7), 1418–1434.

Bernhardt,Jennifer, Stephanie Grell Azar, and Janette Klaehn. 2009. Integrated Financing for Value Chains.Technical

Guide, World Coucil of Credit Unions.

Christen, Robert, P. and Jamie Anderson, 2013.“Segmentation of Smallholder Households:Meeting the Range

of Financial Needs in Agricultural Families.” Washington, D.C.:CGAP. http://www.cgap.org/sites/default/files/

Focus-Note-Segmentation-of-Smallholder-Households-April-2013_0.pdf.

GIZ. 2013. Value chain development by the private sector in Africa:Lessons learned and guidance notes. [Online]

Available:http:// ccps-africa.org.winhost.wa.co.za/dnn7/Portals/0/VCP%20web%20en%2018-07-13m.pdf

Bogaard, Hans. 2014.“Value Chain Finance and the Importance of Understanding the Value Chain.” Presentation at

Revolutionising Finance for agri-value chains.

Colbert, Ross. 2013.“Winning Through the Supply Chain:Strategic Issues in Managing Food and Agri Suply and

Supply Chains.” AgriFin Presentation. Colombo:AgriFin.

Collier, Paul and Stefan Dercon. 2013.“African Agriculture in 50 Years :Smallholders in a Rapidly Changing World?”

World Development, xx.

Dalberg Global Development Advisors. 2012.“Catalyzing Smallholder Agricultural Finance.”

Deininger, Klaus, and Derek Byerlee. (2012).The rise of large farms in land abundant countries:Do they have a

future?. World Development, 40(4), 701-714.

Demirhan, Ömer. 2013.“Execution of ALES :Yapı Kredi Case.” Presentation at Agrifin Boot Camp.

---.2014a“Industry and Customer Analysis:Analyzing Specific Value Chains inTurkey.”Presentation at Agrifin Boot Camp.

Doran, Alan, Ntongi McFayden, and Robert C.Vogel. 2009.The Missing Middle in Agricultural Finance:Relieving the

capital constraint on smallholder groups and other agricultural SMEs. Oxfam Policy and Practice:Agriculture,

Food and Land, 9(7), 65-118.](https://image.slidesharecdn.com/c02cdfb3-760d-4c71-b00b-2817434ff8c8-160606200049/85/Bankers-Guide-to-AVCF-76-320.jpg)