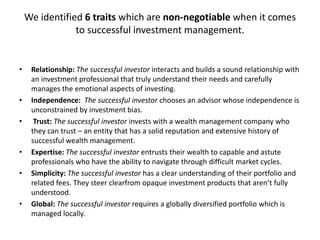

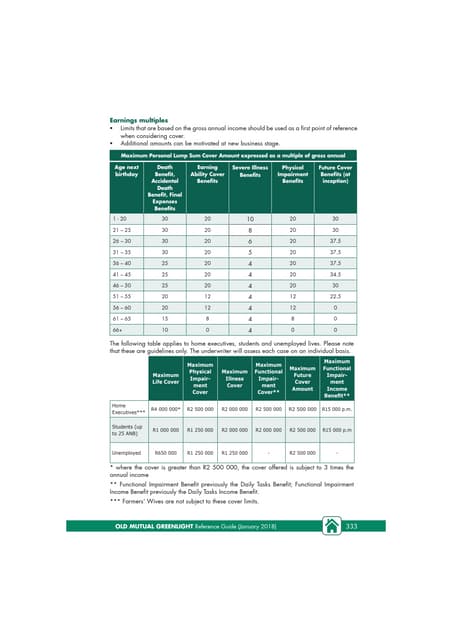

The document summarizes a presentation given by Sasfin Wealth, a South African wealth management firm. It discusses Sasfin Wealth's history, investment process, competitive advantages, and awards. It also provides an overview of Sasfin Securities and outlines six traits of successful investing. The presentation concludes by discussing Sasfin's investment offerings and foundation portfolios.