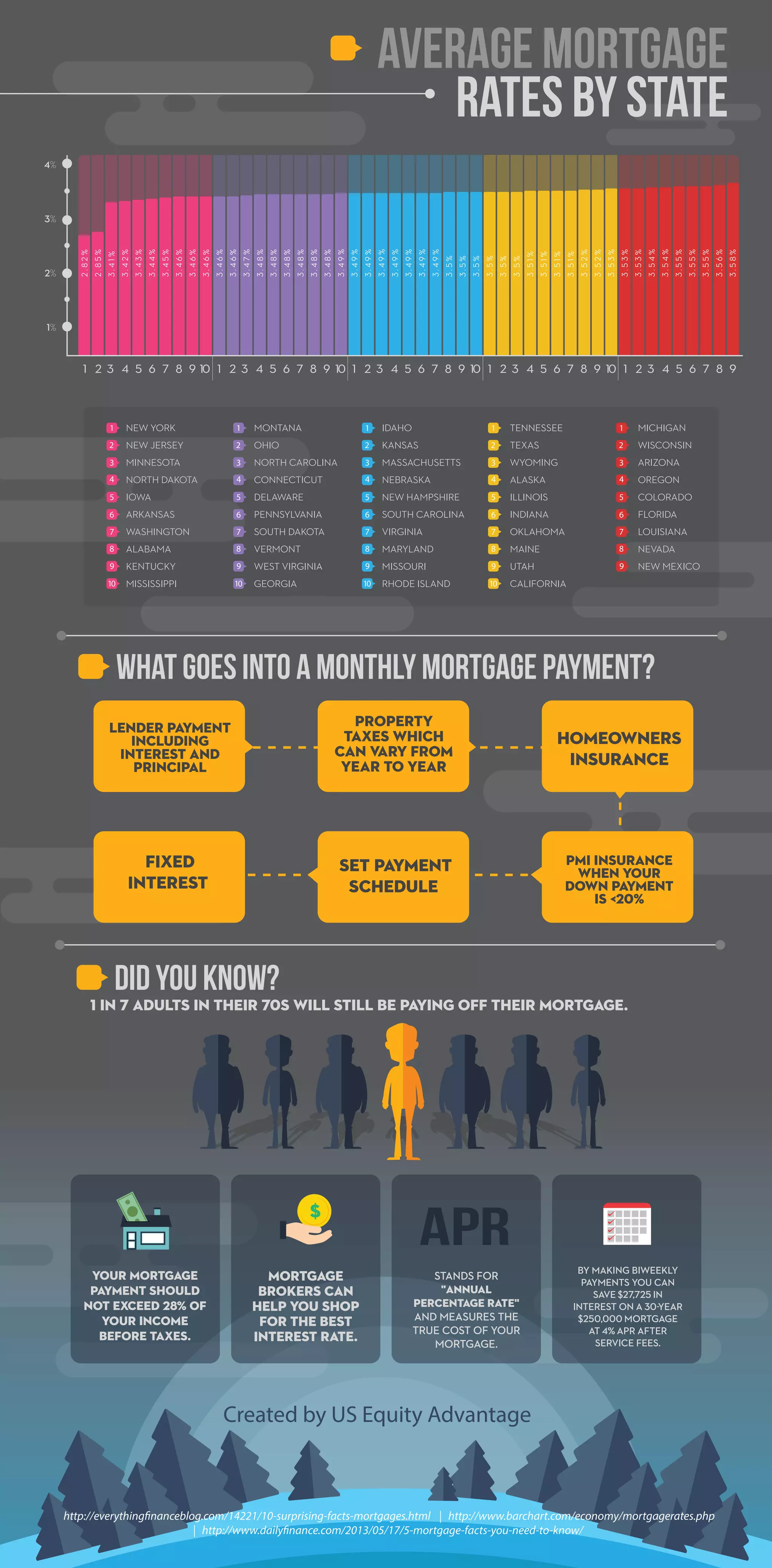

The document outlines key information about mortgages, including the components of monthly payments, average mortgage rates by state, and surprising facts such as 1 in 7 adults in their 70s still paying off a mortgage. It emphasizes that mortgage payments should not exceed 28% of pre-tax income, and discusses the potential savings from biweekly payments. Additionally, it highlights the importance of mortgage brokers in finding the best interest rates.

![2015 Infographic 0115[3]](https://cdn.slidesharecdn.com/ss_thumbnails/ec15fab1-5391-4836-91b4-aef0660382e3-150211093921-conversion-gate02-thumbnail.jpg?width=640&height=640&fit=bounds)