Download to read offline

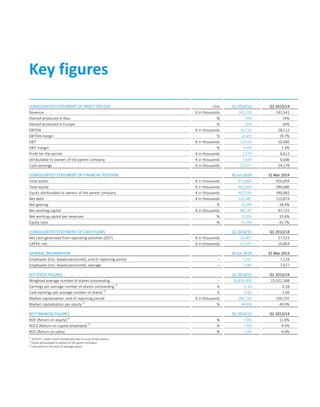

This document provides financial information for AT&S Group for the first quarter of 2014/15 compared to the same period the previous year. Key points: - Revenue was €141.3 million, similar to the previous year. - EBITDA increased 3.6% to €29.1 million. - Consolidated net income rose 14.6% to €7.6 million. - The Mobile Devices segment saw a 9% decline in revenue due to different project timelines versus the previous year, but current revenue levels are viewed positively. - The Industrial & Automotive segment grew revenue by 9% due to increased electronics in cars and steady growth in industrial applications.

![Metka - Resume of Coverage [Euroxx]](https://cdn.slidesharecdn.com/ss_thumbnails/euroxxmetkaresumeofcoverage01jul13tolis-130702013555-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)