Download as PDF, PPTX

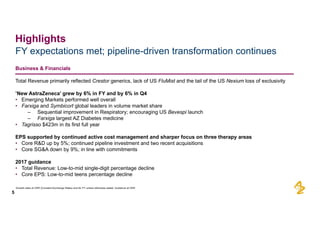

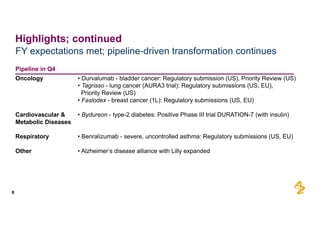

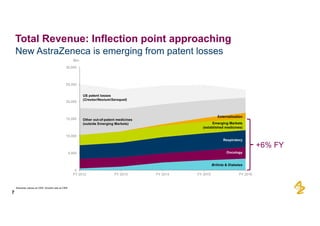

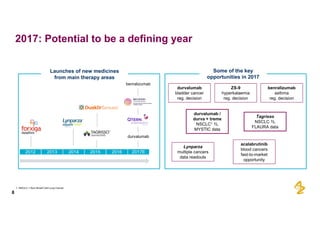

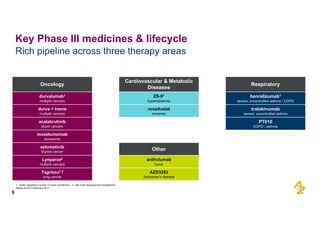

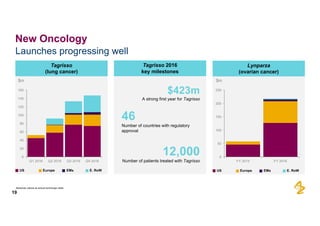

The document provides an overview of AstraZeneca's full-year and Q4 2016 results presentation. It notes that total revenue was primarily impacted by generic competition for Crestor and the tail-end of Nexium's loss of exclusivity in the US. The "New AstraZeneca" grew by 6% in FY 2016 and Q4, led by growth in Emerging Markets, Symbicort, and Farxiga. EPS was supported by cost management. 2017 guidance forecasts low-to-mid single digit revenue decline and low-to-mid teens decline in core EPS. The presentation highlights pipeline progress including regulatory filings for Tagrisso, Durvalumab and Faslodex.