Downloaded 10 times

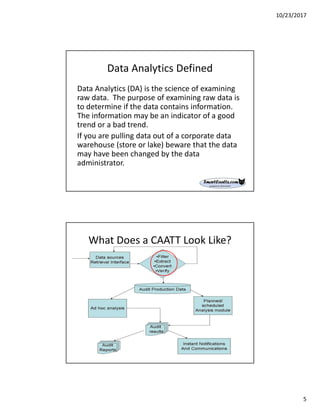

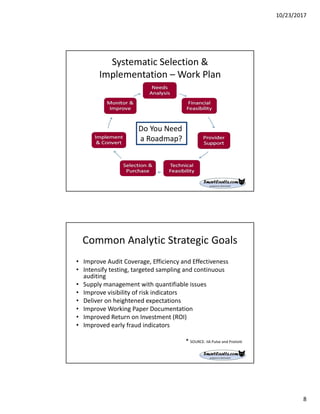

The document outlines the services of AuditNet, a global resource for auditors, providing access to templates, webinars, and professional resources for the audit community. It discusses the significance of selecting effective Computer Assisted Audit Tools (CAATs) to enhance audit processes, emphasizing systematic selection and implementation strategies. Additionally, it highlights the importance of training, monitoring, and continuous improvement in data analytics within internal audit functions.

![7.__Developing_a_Research_Proposal[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7-260131073037-df92dd7d-thumbnail.jpg?width=640&height=640&fit=bounds)

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)