Downloaded 14 times

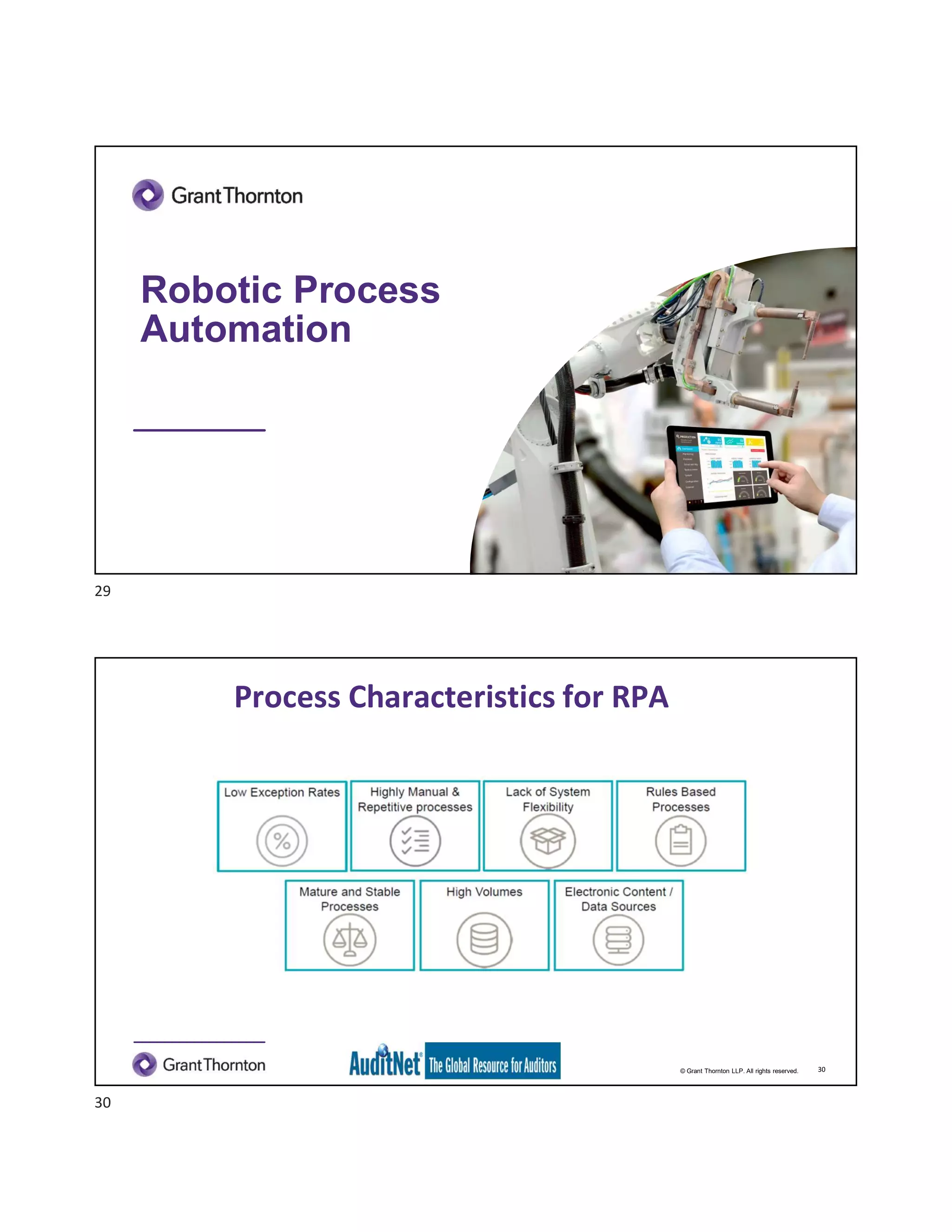

The document discusses the role of robotic process automation (RPA) in auditing, emphasizing its potential to enhance efficiency and accuracy in audit processes. It highlights the features of AuditNet, a global resource for auditors, and outlines training and certification opportunities related to RPA. Additionally, it provides insights into the practical applications of RPA in various auditing functions, alongside the benefits and challenges of integrating technology into auditing tasks.

![[DSC Europe 25] Jim Sterne - Adopting Generative AI Capabilities Into the Ent...](https://cdn.slidesharecdn.com/ss_thumbnails/sxhpofuorcagxsaulkmt-3-251204082258-7e66bc48-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Goran Obradovic - The Rise of Sovereign AI: Building the Regi...](https://cdn.slidesharecdn.com/ss_thumbnails/7nw2xxixrxqdxvrb5wca-6-251205085714-ab09a2ac-thumbnail.jpg?width=640&height=640&fit=bounds)