Downloaded 16 times

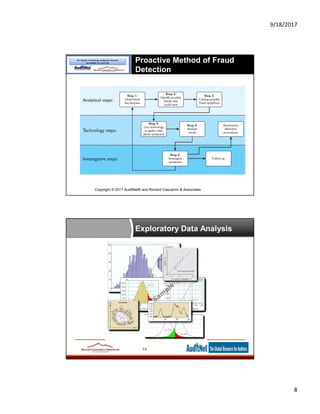

The document provides information about data analytics for auditors, featuring insights from experts Jim Kaplan and Richard Cascarino, along with details about auditnet®, a comprehensive resource for audit professionals. It covers topics such as probability theory, fraud detection techniques, data mining, and statistical analysis relevant to internal audit practices. Furthermore, it outlines the necessary conditions and procedures for obtaining CPE credits during webinars conducted by auditnet®.

![7.__Developing_a_Research_Proposal[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7-260131073037-df92dd7d-thumbnail.jpg?width=640&height=640&fit=bounds)

![Hacking-Uncovered-How-People-Get-Hacked-and-How-to-Stay-Safe[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/hacking-uncovered-how-people-get-hacked-and-how-to-stay-safe1-260130170011-4883a9c7-thumbnail.jpg?width=640&height=640&fit=bounds)

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)