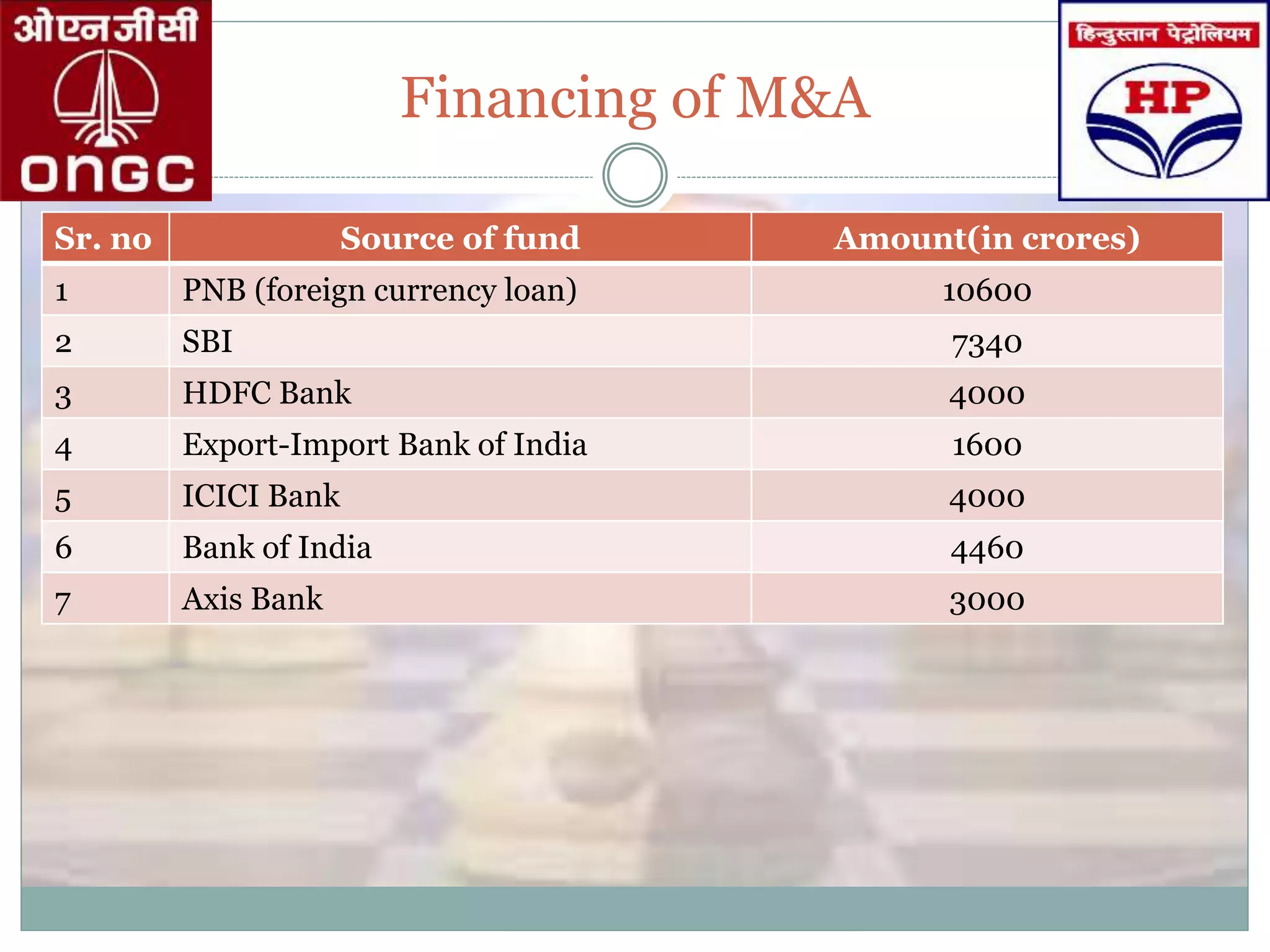

The document details the acquisition of HPCL by ONGC, discussing its historical context, rationale behind the merger, and its projected impact on the oil and gas industry. It highlights ONGC's evolution into an integrated oil company and contrasts the financial implications of acquiring HPCL versus BPCL. The merger is positioned as beneficial for both companies, although it also raises concerns about competition and inefficiencies in the sector.