Downloaded 11 times

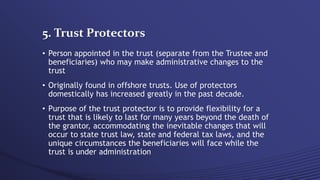

The document discusses irrevocable trusts, explaining their characteristics and the limitations on altering them once established. It outlines various methods for modifying such trusts, including beneficiaries' agreements, court orders, decanting, trust termination, and the role of trust protectors, and emphasizes the importance of adapting trust terms to changing circumstances. Additionally, it highlights the implications of outdated trust documents and legislative changes affecting trust administration and tax obligations.

![[2015 07-28] lecture 22: ... Nothing, Something](https://cdn.slidesharecdn.com/ss_thumbnails/2015-07-28lecture22-150728212658-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)