All tasks assessment-501

•

0 likes•1,673 views

The document outlines a contingency plan for a company that includes identifying risks, assigning risk scores, proposed contingency strategies, responsibilities, timelines, and budgets. Three key risks identified are profit being more than 10% less than budgeted, lack of enforcement of credit terms impacting cash flow, and many bikes needing repairs or being thrown out due to rust. Contingency strategies proposed include developing sales strategies, creating credit policies and procedures, and minimizing rust on bikes. Responsibilities, timelines, and budgets are assigned for each contingency strategy.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to All tasks assessment-501

Similar to All tasks assessment-501 (20)

More from Jatins Anand

Recently uploaded

Recently uploaded (20)

All tasks assessment-501

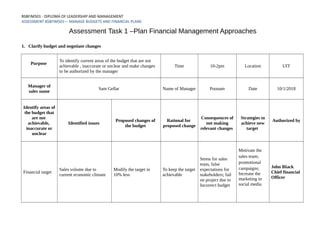

- 1. BSBFIM501 - DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501— MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 1 –Plan Financial Management Approaches 1. Clarify budget and negotiate changes Purpose To identify current areas of the budget that are not achievable , inaccurate or unclear and make changes to be authorized by the manager Time 10-2pm Location UIT Manager of sales name Sam Gellar Name of Manager Poonam Date 10/1/2018 Identify areas of the budget that are not achievable, inaccurate or unclear Identified issues Proposed changes of the budget Rational for proposed change Consequences of not making relevant changes Strategies to achieve new target Authorized by Financial target Sales volume due to current economic climate Modify the target in 10% less To keep the target achievable Stress for sales team, false expectations for stakeholders; fail on project due to Incorrect budget Motivate the sales team; promotional campaigns; Increase the marketing in social media John BIack Chief financial Officer

- 2. BSBFIM501 - DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 1 –Plan Financial Management Approaches Waste Removal The cost of waste removal is 20% more than budgeted To find other solutions for wasting and to reduce the waste of materials To reduce the cost of waste removal and keep it within budgeted Waste money with something that could be managed by other solution To find out the reason of waste keep track of production process,find better solutions for it, to create policies and procedures for wasting Charles Pierce – Production Manger Advertising Economic downturn To reduce the budget for expensive media and to explore cheaper media To keep the budget within the proposed and save money for other areas Using the budget for non-effective result and make it out of planned Alternative advertisement Stuart LaRoux – Operations General manger

- 3. BSBFIM501 - DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 1 –Plan Financial Management Approaches 2. Three accounting Principles Principles of accounting can also refer to the basic or fundamental accounting principles: cost principle , materiality principles and time period assumption going concern principles, economic entity principles, and so on. In this context, principles of accounting refers to the broad underlying concepts which guide accountants when preparing financial statements. Principles of accounting can also meangenerally accepted accounting principles(GAAP). Generally accepted accounting principles (GAAP) are a common set ofaccounting principles, standards and procedures that companies must follow when they compile their financial statements. GAAP is a combination of authoritative standards (set by policy boards) and the commonly accepted ways of recording and reporting accounting information. GAAP improves the clarity of the communication of financial information.GAAP attempts to standardize and regulate the definitions, assumptions and methods used in accounting. This helps companies prepare consistent financial statements from year to year. cost principles :The cost principle is one of the basic underlying guidelines in accounting. It is also known as the historical cost principle. The cost principle also means that valuable brand names and logos that were developed through effective advertising will not be reported as assets on the balance sheet. This could result in a company's most valuable assets not being included in the company's asset amounts. (On the other hand, a brand name that is acquired through a transaction with another company will be reported on the balance sheet at its cost.) materiality principles:In accounting, the concept of materiality allows you to violate another accounting principle if the amount is so small that the reader of the financial statements will not be misled. A classic example of the materiality concept or the materiality principle is the immediate expensing of a $10 wastebasket that has a useful life of 10 years. The matching principle directs you to record the wastebasket as an asset and then depreciate its cost over its useful life of 10 years. The materiality principle allows you to expense the entire $10 in the year it is acquired instead of recording depreciation expense of $1 per year for 10 years. The reason is that no investor,creditor, or other interested party would be misled by not depreciating the wastebasket over a 10-year period. Determining what is a material or significant amount can require professional judgment. For example, $5,000 might be immaterial for a large, profitable corporation, but it will be material or significant for a small company that has very little profit. time period assumption:It is also known as the periodicity assumption. The accounting guideline that allows the accountant to divide up the complex, ongoing activities of a business into periods of a year, quarter, month, week, etc. The precise time period covered is included in the heading of the income statement, statement of cash flows, and the statement of stockholders' equity.

- 4. BSBFIM501 - DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 1 –Plan Financial Management Approaches 3. Three Legislation and ATO requirement GST ACT 1999 : This Act may be cited as the A New Tax System (Goods and Services Tax) Act 1999.The goods and services tax[1](GST) in Australia is a value added tax of 10% on most goods and services sales. GST is levied on most transactions in the production process, but is refunded to all parties in the chain of production other than the final consumer. The tax was introduced by the Howard Government and commenced on 1 July 2000, replacing the previous federal wholesale sales tax system and designed to phase out a number of various State and Territory Government taxes, duties and levies such as banking taxes andstamp duty. An increase of the GST to 15% has been put forward, but is generally lacking in bi-partisan support. Corporation Act 2001 : The Corporations Act 2001 (Cth) (the Corporations Act, or informally as the 'Corps' Act) is an act of the Commonwealth of Australia that sets out the laws dealing with business entities in Australia at federal and interstate level. It focuses primarily on companies, although it also covers some laws relating to other entities such as partnerships and managed investment schemes. The Corporations Act is the principal legislation regulating companies in Australia. It regulates matters such as the formation and operation of companies (in conjunction with a constitution that may be adopted by a company), duties of officers, takeovers and fundraising. The Act is published in five volumes covering a total of ten chapters. The chapters have multiple parts, and within each part there may be multiple divisions. Each chapter contains a collection of sections. Australian Securities and Investments Commission Act 2001 : (1) The objects of this Act are: (a) to provide for the Australian Securities and Investments Commission ( ASIC ) which will administer such laws of the Commonwealth, a State or a Territory as confer functions and powers under those laws on ASIC; and (b) to provide for ASIC's functions, powers and business; and (c) to establish a Corporations and Markets Advisory Committee to provide informed and expert advice to the Minister about the content, operation and administration of the corporations legislation (other than the excluded provisions), about corporations and about financial products and financial markets; and

- 5. BSBFIM501 - DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 1 –Plan Financial Management Approaches (d) to establish a Takeovers Panel, a Companies Auditors Disciplinary Board, a Financial Reporting Council, an Australian Accounting Standards Board, an Auditing and Assurance Standards Board and a Parliamentary Joint Committee on Corporations and Financial Service. (2) In performing its functions and exercising its powers, ASIC must strive to: (a) maintain, facilitate and improve the performance of the financial system and the entities within that system in the interests of commercial certainty, reducing business costs, and the efficiency and development of the economy (b) promote the confident and informed participation of investors and consumers in the financial system. (d) administer the laws that confer functions and powers on it effectively and with a minimum of procedural requirements; and (e) receive, process and store, efficiently and quickly, the information given to ASIC under the laws that confer functions and powers on it; and (f) ensure that information is available as soon as practicable for access by the public; and (g) take whatever action it can take, and is necessary, in order to enforce and give effect to the laws of the Commonwealth that confer functions and powers on it. (3) This Act has effect, and is to be interpreted, accordingly. Australian Securities and Investments Commission(ASIC) is a body corporate (1) ASIC: (a) is a body corporate, with perpetual succession; and (b) has a common seal; and (c) may, subject to subsection (5), acquire, hold and dispose of real and personal property; and (ca) may enter into contracts; and (d) may sue and be sued in its corporate name. Note:ASIC was established by section 7 of the Australian Securities and Investments Commission Act 1989 and is continued in existence by section 261 of this Act.

- 6. BSBFIM501 - DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 1 –Plan Financial Management Approaches ATO Requirement Record keeping : Generally, for tax purposes, you must keep your records in an accessible form (either printed or electronic) for five years. Some of the basic records you may need to keep are: governing documents (for example, constitution, rules, trust deed) financial reports (for example, financial statements, annual budgets, reconciliations, audit reports, accounts payable and accounts receivable) cash book records of daily receipts and payments tax invoices and income tax records, such as debtors and creditors lists, stocktake records and motor vehicle expenses records relating to employees (for example, TFN declarations, pay as you go (PAYG) with holding, super annuation and fringe benefits provided) records of payments withheld from suppliers who do not quote an Australian business number (ABN) banking records (for example, bank statements, deposit books, cheque books, bank reconciliation) grant documentation (for example, when funding will be received, when acquittals need to be made, application deadlines) registration, certificates and accompanying documents to regulators (for example, ATO, Australian Charities and Not-for-profits Commission, and state regulators) contracts and agreements (for example, cleaning, maintenance and insurance contracts, finance or lease agreements) copies of reviews of entitlement to tax concessions records to help prepare tax statements and returns.

- 7. BSBFIM501 - DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 1 –Plan Financial Management Approaches 4. Principles and Techniques of managing budget items Capital budgeting has five principles that play a crucial role in the allocation of money and the process of capital budgeting. The five principles are; (1) decisions are based on cash flows, not accounting income, (2) cash flows are based on opportunity cost, (3) The timing of cash flows are important, (4) cash flows are analyzed on an after tax basis, (5) financing costs are reflected on project’s required rate of return. (1) Relevant cash flows are based on incremental cash flows. This represents the changes in cash flow if the project is undertaken. Aspects of cash flow that affect capital budgeting are sunk costs and externalities. These are both costs that cannot be avoided. Sunk costs are costs that are unavoidable, even if the project is undertaken. Externalities are side effects of a project that affect other firm cash flows. (2) Cash flows are based on opportunity cost. In other words, it is the cash flow that will be lost due to the financing of a project. These are cash flows that are accumulated by assets the firm already owns and would be sunk if the project under consideration is undertaken. (3) The timing of cash flow is crucial because it is dependent on the time value of money. Cash flow that is received now will be worth more in the future if it were to be received later. (4) Cash flows are measured on an after tax basis. It is useless to measure cash flow before taxes because it is not its present value. Firm’s value is based on cash flow that a firm gets to keep, not the money that is sent to the government. (5) Financing costs are reflected on project’s required rate of return. Rate of return is an aspect of financing that has potential risks. Project’s that are expected to have a higher rate of return than their cost of capital will increase the value of the firm. BudgetingTechniques A budget is basically a plan of action for the forthcoming business period and budget planning should involve the whole organisation. The ability to budget effectively is crucial both in terms of performance and profitability as without having an awareness of costs it is all too easy to spiral down into losses over a period of time.

- 8. BSBFIM501 - DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 1 –Plan Financial Management Approaches There are thee main budgeting techniques: Incremental budgeting Zero-based budgeting Flexed budgeting Incremental Budgeting The incremental approach to budgeting combines the costs identified from the previous accounting period with percentage additions. These percentage additions are utilised to cover two key areas which include cost increases as a result of inflation or higher purchases costs and predictions associated with increases in costs and income as a result of business volume predictions. A key limitation of the incremental budgeting system is the manner in which percentages are added in a blanket fashion resulting in the likelihood of higher overall costs in the long-term. This may then also result in a business having to increase its sale prices to a level that is no longer competitive. Zero-Based Budgeting The clue is is in the title here as the zero-based budgeting system requires budgeting to commence with the assumption that every cost has a zero base. Next, each item relating to expenditure is worked through and decisions are made as to whether the purchase is completely essential. Then different purchasing options associated with the specific item are explored as a means of ensuring the item is obtained as cost-effectively as possible. One of the main limitations of the zero-budgeting system is that it can take an awful lot of time to work through each individual cost in this manner. However, it is fair to add that utilising this approach will then provide an extremely useful database containing valuable, time-saving information for the years to come. Flexed Budgeting As with zero-based budgeting, the flexed budgeting system gives its name away in the title as it involves ‘flexing’ the normal budget. The benefits of flexed budgeting are that it is likely to be considerably more accurate as the budget is adapted to suit various external changes. Within this approach managers are able to provide key information resulting in an achievable budget, pessimistic budget and optimistic budget. Through undertaking the process of flexed budgeting, managers are better able to make important decision relating to risk and expenditure, having gained a wider perspective on best and worst outcomes. As highlighted above, there are three main categories associated with budgeting which include incremental, zero-based and flexed budgeting. Each of these approaches has various strengths and limitations with the latter approach being able to provide more accurate information.

- 9. BSBFIM501 - DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 1 –Plan Financial Management Approaches 5. Contingency Plan CONTINGENCY PLAN Company name Developer of the plan Poonam Position Manager of Sales Centre Risk identified Risk Likeline ss Risk Impact Risk Score Contingency Responsibility Time Line in days Budget Profit for FY more than 10% less than budgeted 5 5 25 Develo strate ies to increase sales and training of staff m sales techniques Sam Gellar - Sales General Manager 30 days $8,000 Currently no enforcement of credit terms (customers take too long to pay back impacting on cash flow) 4 5 20 Creates policies and procedures and John Black - CFO 24 days $1,500 Many bikes need to be thrown out in parts rust 4 5 20 Minimize the rust using sprays anti- rust,in case of bikes damaged, fix and sell it cheaper Charles Pierce - Production Manager 20 days $10,000

- 10. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 2- Implement financial management approaches Assessment Task 2- Impement financial management approches Role: You are the manager of Sales Team A. You manage a small tteam of sales team members. Your duties include accessing budget information for your team, explaining relevant aspects of budget documents to your team, and supporting team members to achieve performance goals. 1. Role-play to support team member prep work Purpose To train Bill on policies and procedures as well as usage of formulas and functions on Microsoft Excel Determine organisational needs Keep control of expenses Identify coaching/training needs of team member 30 hours of training Mentoring program 2. Plan Training session Topic to be taught Training Method How do we test participants Resource Required Outcome/Competency Policies and procedures Booklet, online information Internal audition Booklet, documents online, auditor, computer At the end of the training, participants will be able to use and apply policies and procedures Advanced Excel skills (formulas and functions) Course with trainer Online demonstration Excel workbook, computer, excel, trainer, room, tables, chairs, board participants will have advanced excel skills being able to use formulas and functions

- 11. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 2- Implement financial management approaches How to access budget information Workshop, guide information Internal audition Computer, room, video, mentor At the end of the coaching participants will be able to access budget information Advanced accounting Skllls Coaching program Make the employee to Work on a real case being monitored by senior staff member Senior staff member, computer At the end of the coaching program work on a real participants will have advanced accounting skills, being able to deal with different problems and prolects, finding solutions

- 12. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances Assessment Task 3- Monitor and finances Budget variance Report FY Actual Q1 Actual Q2 Actual Q3 Actual Q4 Actual REVENUE Commissions 60,000 52,000 17,500 15,000 25,000 22,000 17,000 15,000 17,500 15,000 Direct wages fixed 200,000 200,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 Sales 3,000,000 2,900,000 700,000 600,000 1000,000 900,000 700,000 800,000 700,000 600,000 Cost of Goods Sold 400,000 380,000 100,000 95,000 100,000 95,000 100,000 95,000 100,000 95,000 Gross Profit 2,340,000 2,247,000 535,000 444,000 825,000 735,000 532,000 640,000 535,000 444,000 EXPENSES General & Administrative Expenses Travel 20,000 22,000 5,000 4,000 5,000 6,000 5,000 6,000 5,000 6,000 Legal Fees 5,000 4,500 1,250 1,050 1,250 1,150 1,250 1,150 1,250 1,150 Bank Charges 600 700 150 200 150 200 150 150 150 150 Office Supplies 5,000 4,000 1,250 1,000 1,250 1,000 1,250 1,000 1,250 1,000 Postage 500 125 100 125 100 125 100 125

- 13. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances Printing 400 100 Dues & subscriptions 500 600 125 150 125 150 125 150 125 150 Telephone 10,000 11,200 2,500 2,800 2,500 2,800 2,500 2,800 2,500 2,800 Repairs & maintenance 50,000 45,000 25,000 20,000 25,000 20,000 25,000 20,000 25,000 20,000 Payroll tax 25,000 25,000 6,250 6,250 6,250 6,250 6,250 6,250 6,250 6,250 Marketing Expenses Advertising 200,000 208,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 Employment Expenses Superannuation 45,000 45,000 11,250 11,250 11,250 11,250 11,250 11,250 11,250 11,250 Wages & salaries 500,000 500,000 125,000 125,000 125,000 125,000 125,000 125,000 125,000 125,000 Staff amenities 20,000 23,000 5,000 6,000 5,000 6,000 5,000 6,000 5,000 6,000 Occupancy Costs Electricity 40,000 38,000 10,000 8,000 10,000 10,000 10,000 10,000 10,000 10,000 Insurance 100,000 100,000 25,000 25,000 25,000 25,000 25,000 25,000 25,000 25,000 Rates 100,000 100,000 25,000 25,000 25,000 25,000 25,000 25,000 25,000 25,000 Rent 200,000 200,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 Water 30,000 35,000 7,500 10,000 7,500 10,000 7,500 7,500 7,500 7,500 Waste removal 50,000 60,000 12,500 15,000 12,500 15,000 12,500 15,000 12,500 15,000

- 14. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances TOTAL EXPENSES 1,401,500 1,422,500 362,875 362,825 362,875 374,925 337,875 342,375 337,875 342,375 NET PROFIT (BEFORE INTEREST & TAX) 1,021,000 825,000 169,625 77,175 462,125 357,575 194,625 297,625 194,625 97,625 Income Tax Expense (25%Net) 255,250 206,250 42,406 19,294 115,531 89,394 48,656 74,406 48,656 24,406 NET PROFIT AFTER TAX 765,750 618,750 127,219 57,881 346,594 268,181 145,969 223,219 145,969 73,219 1. Graphs for Gross Profit, total Expenses and net profit after Tax for each quater.

- 15. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances Q1 Q2 Q3 Q4 -200000 0 200000 400000 600000 800000 1000000 -92500 -92500 107500 -92500 440000 732500 640000 440000 532500 825000 532500 532500 GROSS PROFIT Variance Actual Planned

- 16. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances Q1 Q2 Q3 Q4 -50000 0 50000 100000 150000 200000 250000 300000 350000 400000 -50 12050 4500 4500 362825 362875 342375 342375 362875 374925 337875 337875 TOTAL EXPENSES Variance Actual Planned

- 17. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances Q1 Q2 Q3 Q4 -100000 -50000 0 50000 100000 150000 200000 250000 300000 350000 400000 -69337.5 -78412 77250 -72750 127218.75 346593.75 145968.75 145968.75 NET PROFITAFTER TAX Variance Actual Planned

- 18. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances 2. Spreadsheet to capture budgeted and actual figures to produce a variance report. Big Red Bicycle Budget Variation Report FY 2011/2012 Q1 Actual Variance Q2 Actual Variance Q3 Actual Variance Q4 Actual Variance $ % $ % $ % $ % REVENUE Commissions 17,500 15,000 (2,500 ) 14% 25,000 22,000 (2,50 0 10% 17,000 15,000 (2,500) 14% 17,500 15,000 (2,500 ) 14% Direct wages fixed 50,000 50,000 0.00 0% 50,000 50,000 0.00 0% 50,000 50,000 0.00 0% 50,000 50,000 0.00 0% Sales 700,000 600,00 0 100,0 00 14% 1000,0 00 900,00 0 100,0 00 10% 700,00 0 800,00 0 100,00 0 14% 700,00 0 600,00 0 100,0 00 14% Cost of Goods Sold 100,000 95,000 (5,000 ) (5% ) 100,00 0 95,000 (5,00 0) (5% ) 100,00 0 95,000 (5,000) (5%) 100,00 0 95,000 (5,000 ) 5% Gross Profit 535,000 444,00 0 (92,50 0 17% 825,00 0 735,00 0 (92,5 00 11% 532,00 0 640,00 0 107,50 0 20% 535,00 0 444,00 0 (92,50 0 17% EXPENSES General & Administrative Expenses

- 19. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances Travel 5,000 4,000 1,000 20% 5,000 6,000 1,000 20% 5,000 6,000 1,000 20% 5,000 6,000 1,000 20% Legal Fees 1,250 1,050 (200) 16% 1,250 1,150 (100) (8% ) 1,250 1,150 (100) (8%) 1,250 1,150 (100) (8% Bank Charges 150 200 50,00 33% 150 200 50,00 33% 150 150 0.00 0% 150 150 0.00 0% Office Supplies 1,250 1,000 (250) 20% 1,250 1,000 (250) 20% 1,250 1,000 (250) 20% 1,250 1,000 (250) 20% Postage & Printing 100 125 25,00 25% 100 125 25,00 25% 100 125 25,00 25% 100 125 25,00 25% Dues & subscriptions 125 150 25,00 20% 125 150 25,00 20% 125 150 25,00 20% 125 150 25,00 20% Telephone 2,500 2,800 300,0 0 12% 2,500 2,800 300,0 0 12% 2,500 2,800 300,00 12% 2,500 2,800 300,0 0 12% Repairs & maintenance 25,000 20,000 5,000 20% 25,000 20,000 0.00 0% 25,000 20,000 0.00 0% 25,000 20,000 0.00 0% Payroll tax 6,250 6,250 0.00 0% 6,250 6,250 0.00 0% 6,250 6,250 0.00 0% 6,250 6,250 0.00 0% Marketing Expenses Advertising 50,000 50,000 2,000 4% 50,000 56,000 6,000 12% 50,000 50,000 0.00 0% 50,000 50,000 0.00 0% Employment Expenses Superannuation 11,250 11,250 0.00 0% 11,250 11,250 0.00 0% 11,250 11,250 0.00 0% 11,250 11,250 0.00 0% Wages & salaries 125,000 125,00 0 0.00 0% 125,00 125,00 0.00 0% 125,00 125,00 0.00 0% 125,00 125,00 0.00 0%

- 20. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances 0 0 0 0 0 0 Staff amenities 5,000 6,000 1,000 20% 5,000 6,000 0.00 0% 5,000 6,000 1,000 20% 5,000 6,000 1,000 20% Occupancy Costs Electricity 10,000 8,000 2,000 20% 10,000 10,000 0.00 0% 10,000 10,000 0.00 0% 10,000 10,000 0.00 0% Insurance 25,000 25,000 0.00 0% 25,000 25,000 0.00 0% 25,000 25,000 0.00 0% 25,000 25,000 0.00 0% Rates 25,000 25,000 0.00 0% 25,000 25,000 0.00 0% 25,000 25,000 0.00 0% 25,000 25,000 0.00 0% Rent 50,000 50,000 0.00 0% 50,000 50,000 0.00 0% 50,000 50,000 0.00 0% 50,000 50,000 0.00 0% Water 7,500 10,000 2,500 33% 7,500 10,000 2,500 33% 7,500 7,500 0.00 0% 7,500 7,500 0.00 0% Waste removal 12,500 15,000 2,500 20% 12,500 15,000 2,500 20% 12,500 15,000 2,500 20% 12,500 15,000 2,500 20% TOTAL EXPENSES 362,875 362,82 5 (50) 0% 362,87 5 374,92 5 12,05 0 3% 337,87 5 342,37 5 4,500 1% 337,87 5 342,37 5 4,500 1% NET PROFIT (BEFORE INTEREST & TAX) 169,625 77,175 92,45 0 55% 462,12 5 357,57 5 104,5 50 23% 194,62 5 297,62 5 103,00 0 53% 194,62 5 97,625 97,00 0 50% Income Tax Expense (25%Net) 42,406 19,294 23,11 3 55% 115,53 1 89,394 26,13 8 23% 48,656 74,406 25,750 53% 48,656 24,406 24,25 0 50%

- 21. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances NET PROFIT AFTER TAX 127,219 57,881 69,33 8 55% 346,59 4 268,18 1 78,41 3 23% 145,96 9 223,21 9 77,250 53% 145,96 9 73,219 72,75 0 50% Big Red Bicycle -Budget Variation Report FY 2011/2012 FY Actual Variance $ % REVENUE Commissions 60,000 52,000 (5,000) (6%) Direct wages fixed 200,000 200,000 0.00 0% Sales 3,000,000 2,900,000 (200,000) (6%) Cost of Goods Sold 400,000 380,000 (20,000) (5%) Gross Profit 2,340,000 2,247,000 (175,000) (7%) EXPENSES General & Administrative Expenses

- 22. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances Travel 20,000 22,000 2,000 10% Legal Fees 5,000 4,500 (500) (10%) Bank Charges 600 700 100,00 17% Office Supplies 5,000 4,000 (1,000) 20% Postage & Printing 400 500 100 25% Dues & subscriptions 500 600 100 20% Telephone 10,000 11,200 1,200 12% Repairs & maintenance 50,000 45,000 (5,000) (10%) Payroll tax 25,000 25,000 0.00 0% Marketing Expenses Advertising 200,000 208,000 0,000 4% Employment Expenses Superannuation 45,000 45,000 0.00 0% Wages & salaries 500,000 500,000 0.00 0% Staff amenities 20,000 23,000 3,000 15% Occupancy Costs Electricity 40,000 38,000 (2,000) (5%) Insurance 100,000 100,000 0.00 0%

- 23. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances Rates 100,000 100,000 0.00 0% Rent 200,000 200,000 0.00 0% Water 30,000 35,000 5,000.00 17% Waste removal 50,000 60,000 10,000.00 20% TOTAL EXPENSES 1,401,500 1,422,500 21,000.00 1% NET PROFIT (BEFORE INTEREST & TAX) 1,021,000 825,000 196,000 (19%) Income Tax Expense (25%Net) 255,250 206,250 49,000 (19%) NET PROFIT AFTER TAX 765,750 618,750 147,000 -19%

- 24. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances 3. Modified contigency plan and modified implementation plan For every variance identified: Variance type & % Rational Strategy to correct Person responsible Time Monitor Sales — 6% less Impact negatively on the profit Create promotional campaigns, discounts for cash payments, training sales team in sales techniques Sam Gellar Sales General Manager 3 weeks Monthly Bank Charges 17% To avoid paying unnecessary bank charges Negotiate with the back better charges, if not possible, find a bank with better rates Pat Roberts Senior Accountant 1 week FY Dues & Subscriptions 20% To reduce the percentage on dues and subscriptions in 20% to keep within the budget For subscriptions, to find free subscriptions or even cut them off, when i is not possible to negotiate a cheaper price Stuart LaRoux Operations General Manager 1 week Monthly Travel 10% To reduce the percentage and keep within the budget Create a policy and procedure to evaluate when is extremely necessary to travel, otherwise, video chats Charles Pierce Production Manager 2 weeks Monthly Postage & Printing 25% To reduce the percentage, finding out what is waste and keep it within the budget Create a policy and procedure for printing. For postage, to find out the reason and share the expense with the recipient. Charles Pierce Production Manager 2 weeks Monthly

- 25. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances Telephone 12% To be more objective when using telephone reducing the time spent on it To create a limit of minutes for calls, when is possible, to use other communication ways (email, message, etc) Stuart LaRoux Operations General Manager 1 week Fortnight Staff Amenities 15% To reduce the money spent on staff amenities keeping within the budget To find out what is necessary for staff and reduce what is not so necessary Holly Burke HR Manager 2 weeks Monthly Advertising 4% To keep the budget within the proposed and save money for other areas To find cheaper alternative advertisement (social media, for example) Stuart LaRoux Operations General Manager 2 weeks Monthly Water 17% To use the right amount of water avoiding waste and to keep it within budgeted Create policies and procedures for water usage Stuart LaRoux Operations General Manager 3 weeks Monthly Waste Removal 20% To reduce the cost of waste removal and keep it within budgeted To find out the reason of waste, keep track of production process, find better solutions for it, to create policies and procedures for wasting Stuart LaRoux Operations General Manager 3 weeks Monthly 4. Create a 3 step procedure based on 1 Variance identified, to eliminate or reduce the likeliness of a variance occurring in the future. Manage budget and financial plans procedure Purpose : the purpose of this procedure is to reduce or even eliminate the likeliness of variance in budgets of Big Red Bicycle. This is a part of a continuous improvement on budget and financial plans.

- 26. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances Area: Sales 1. Planning • Analyse the market and economic forecast; • To analyse competitors companies; • To maintain clients and explore others possible clients; • Establish the target to be achieved considering SMART criteria; • To train sales staff in sales techniques; 2. Monitor • Monthly sales report; • Identify what are the gaps that results in low level of sales; • If is related to staff performance, to provide training to help them achieving targets; • If is due to economic situation, to create promotional campaigns, discounts, etc. 3. Review and evaluate • Evaluate sales performance; • Review and establish new procedures for those systems that may be failing; • Agree on a new plan.

- 27. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment Task 3- Monitor and finances

- 28. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes ASSESSMENT TASK 4 - Review and evaluate financial management processes TASK A As you are aware, one risk to the strategic plans of Big Red Bicycle (BRB) is bad debt and poor cash flow due to large trade debtor balances. Consider the following: The following information from the Statement of Financial Position and current ledger accounts in the electronic accounting system (MYOB AccountRight). Account $ Trade debtors 362,500 Trade creditors 80,000 Opening stock 100,000 Closing stock 300,000 Purchases 1,000,000 1. Review the Statement of Financial Performance in Appendix 2 to calculate: a. The average debtor days: 46 days Average debtor days = (tradedebtors sales ) x365 = (362,500 2,900,000 )x365 = 45.63 b. The average creditor days: 77 days Average creditor days = ( trade creditors cost of sales ) x365 = ( 80,000 380,000 ) x365 = 76,84 c. The average stock turnover: $60,000

- 29. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes Average stock turnover = (openingstock+closingstock 2 ) = (100,000+20,000 2 ) = 60,000 2. Two written recommendations for improvement to existing financial management processes to improve cash flow. Firstly, we should improve the average debtor days by trying to collect from our debtor within 30 days. From our record, it is shown that there is 15% of our debtors pay their debts later than 60 days. Secondly, we should try to negotiate with our creditors to let us have 45-60 days period of credit days. Therefore, we have more time to manage our cash flow. To support recommendations refer to data sources, organisational needs, and analytical techniques, for example: a. Statement of Financial Performance b. ledger accounts c. scenario information d. ageing debtors budget e. ratios. To improve the existing financial management process in a matter of improving cash flow is necessary to reduce the payment period and also create a discount for payment in cash. To slow down payables is another good technique regarding to cash flow. As was calculated before, the average debtors days is 46 days, which is a higher and critical number for a company. On basic recommendation would be to make it easy for people to pay, giving them many systems to pay. It is very important to have a reliable monthly statement of financial performance, ate least until the percentage of debtors to reduce, and them keep track of it for each quarter. The statements clarify the operations and the financial position of the company. As BRB does not currently train sales staff on credit terms, it could be a recommendation to train staff on this particular case. It is very important not just to sell but to negotiate in good terms for the company. 3. List three sources of information of use to complete this activity

- 30. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes 1.Financial statements Financial statements present the results of operations and the financial position of the company. Financial statements for businesses usually include income statements, balance sheets, statements of retained earnings and cash flows. It is standard practice for businesses to present financial statements that adhere to generally accepted accounting principles (GAAP) to maintain continuity of information and presentation across international borders. Financial statements are often audited by government agencies, accountants, firms, etc. to ensure accuracy and for tax, financing or investing purposes.In short, it is a view of the company’s financial positions as of the date it is prepared. Balance Sheet (Statement of Financial Position) The balance sheet tells you whether the company can pay its bills on time, its financial flexibility to acquire capital and its ability to distribute cash in the form of dividends to the company's owners. In short, it is a view of the company’s financial positions as of the date it is prepared. The balance sheet shows the company's assets, liabilities and shareholders' equity. Each is defined in Statement of Financial Accounting Concepts No. 6, but to summarize: Assets are items that provide probable future economic benefits Liabilities are obligations of the firm that will be settled by using assets. Equity (variously called stockholders equity, shareowners equity or owners equity) is the residual interest that remains after you subtract liabilities from assets and represents what is left for the shareholders. The key balance sheet accounting equation is Assets = Liabilities + Owners Equity, or A=L+OE In the most common format, assets on a balance sheet are listed on the left; they ordinarily have debit balances unless the balance is negative or a contra-asset, an offset to a basic asset account is shown separately. Liabilities and owner’s equity is shown on the righthand side, and these accounts typically have credit balances. These three main categories are separated and further divided to show important relationships and subtotals. Assets are broken down into current and noncurrent (or long-term). Assets are listed from top to bottom in order of decreasing liquidity, i.e., how quickly they can be converted to cash. (For more on this see, Reading The Balance Sheet.) Current assets are cash and other assets that are expected to be used during the normal operating cycle of the business, usually one year. They typically include cash and cash equivalents, short-term investments, accounts receivables, inventory and prepaid expense. Noncurrent assets will not be

- 31. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes realized in full within one year. They typically include long-term investments: property, plant and equipment; intangible assets and other assets. Liabilities are listed in order of expected payment. Obligations expected to be satisfied within one year are current liabilities. They include accounts payable, trade notes payable, advances and deposits, current portion of long-term debt and accrued expenses. Noncurrent liabilities include bonds payable and the portion of long-term debt such as loans maturing in period longer than a year. The structure of the owners' equity section depends on whether the entity is an individual, a partnership or a corporation. Assuming it's a corporation, the section will include capital stock, additional paid-in capital, retained earnings, accumulated other comprehensive income and treasury stock. Balance sheet data can be used to compute key indicators that reveal the company's financial structure and its ability to meet its obligations. These include working capital, current ratio, quick ratio, debt-equity ratio and debt-to-capital ratio. (To learn more read, Testing Balance Sheet Strength.) Analysts, potential creditors and investors can learn a lot from reviewing a company’s balance sheet. For example: How risky is the firm’s capital structure? How does it compare to other companies in the same industry? Too much debt in the capital structure can pose a risk during rough periods in the economy, too little debt might be a sign that too little leverage is being used possibly limiting the company’s ability to grow as quickly as their competitors. How liquid is the company? This can be assessed by looking at the firm’s current assets relative to their current liabilities. The balance sheet in combination with other financial statements is a key tool in reviewing a company’s financial picture and its financial viability. Income Statement The income statement (also known as the profit and loss statement or P&L) tells you both the earnings and profitability of a business. The P&L is always for a specific period of time, such as a month, a quarter or a year. The periodic nature of the income statement is essential as this allows users to compare results for the company over similar periods of time, and to the results of other firms for the same period. Depending on the industry, year over year comparisons that eliminate seasonal variables can be especially useful. The format of the income statement has been determined by a series of accounting pronouncements; some of these are decades old, others released in the past few years. Like the balance sheet, the income statement is broken into several parts:

- 32. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes Income from continuing operations Results from discontinued operations (if any) Extraordinary items (if any) Cumulative effect of a change in accounting principle (if any) Net income Other comprehensive income Earnings per share information Income from continuing operations is the heart of the P&L. It includes sales (or revenue), cost of goods sold, operating expenses, gains and losses, other revenue and expense items that are unusual or infrequent but not both, and income tax expense. This section of the income statement is used to compute the key profitability ratios of gross margin, operating margin, and pretax margin that help readers assess the ability of the company to generate income from its activities. Results from continuing operations are of primary interest because they are ongoing and can be predictive of future earnings; investors put less weight on discontinued operations (which are about the past) and extraordinary items (unusual and infrequent, thus unlikely to recur). Companies thus have an incentive to push negative items that belong in continuing operations into other categories. Net income is the "bottom line"; it is expressed both on an actual and, after comprehensive income, on a per share basis. If a company has hybrid securities, like convertible bonds, there is the potential for additional shares to be created and earnings to be diluted. Earnings per share may therefore be presented on basic and diluted bases, in accordance with the complex rules of FAS 128. 2. Cash flow Cash flow is the life blood of all businesses and is the primary indicator of business health. It is generally acknowledged as the single most pressing concern of most small and medium-sized enterprises (SMEs), although even finance directors of the largest organisations emphasise the importance of cash, and cash flow modelling is a fundamental part of any private equity buy-out. In a credit crunch environment, where access to liquidity is restricted, cash management becomes critical to survival.Cash flow can also be described as a cycle. Your business uses cash to acquire resources. The resources are put to work and goods and services produced. These are then sold to customers. You collect their payments and make those funds available for investment in new resources, and so the cycle repeats. It is crucially important that you actively manage and control these cash inflows and outflows. So what do these look like?

- 33. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes Inflows Cash inflow is money coming into your business: • money from the sale of your goods or services to customers • money on customer accounts outstanding • bank loans • interest received on investments • investment by shareholders in the company. Outflows Cash outflow is, naturally, what you pay out: • purchasing finished goods for re-sale • purchasing raw materials to manufacture a final product • paying wages • paying operating expenses (such as rent, advertising and R&D) • purchasing fixed assets • paying the interest and principal on loans • taxes. Cash flow management Cash flow management is all about balancing the cash coming into the business with the cash going out. The danger is that demands for cash, from the landlord, employees or the tax man, arrive before cash you’re owed is collected. More often than not, cash inflows seem to lag behind your cash outflows, leaving your business short. This money shortage is your cash flow gap. If a company is trading profitably, each time the cycle turns, a little more money is put back into the business than flows out. But not necessarily. If you don’t carefully monitor your cash flow and take corrective action when necessary, your business may find itself in trouble. If cash flow is carefully monitored, you should be able to forecast how much cash will be available on hand at any given time, and plan your business activities to ensure there is always cash to meet upcoming payments 3. Chart of accounts Chart of accounts is constructed with its digitization numbering system. It is not necessary to include an entire dictionary of accounting terms in any general accounting manual, but it is useful to include those that are commonly used within the company’s transactions, as well as those that appear in its accounting software. Of particular importance are those terms that are unique to the industry within which the company operates. For example, the oil and gas, software, and movie industries have special terminology that cannot be learned through regular accounting classes. Developing chart of accounts and its procedure for the first time, the definitions provided, on the manual book, should be concise and meaningful. One or two sentences of definition are usually

- 34. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes sufficient. Because the definitions are references sources, they should be developed for quick and easy look-up. For example, the definition for “fixed asset” may be listed under “A,” using the header “Asset, fixed.” If a user goes to the “F” section of the definitions, there should be a referral statement, such as “Fixed asset, see Asset, fixed. This standard indexing method should make it as easy as possible to find a specific definition. A different approach to the inclusion of accounting term definitions in the manual is to define every account listed in the chart of accounts. By doing so, any accounting personnel who are responsible for entering transactions into either the general ledger or its supporting journals will have a better idea of which accounts should be used. This can save a great deal of time later on, when incorrectly applied transactions must be researched and corrected. The following sample definitions are used for the three-digit sample chart of accounts that was described in my previous post (Chart Of Accounts): 010 – Cash – Money deposited at the bank. If there are restrictions on deposited cash, then it is accounted for as a long-term asset. 020 – Petty cash – Money retained in the petty cash box. 030 – Accounts receivable – Money due from customers for services received or products shipped, but not yet received. If there are amounts due from officers or employees, these moneys are listed under “other accounts receivable.” 040 – Reserve for bad debts – A reserve fund that is held as a contingency against the Non- payment of outstanding accounts receivable. This account should always have a credit balance. 050 – Marketable securities – Cash that is invested in easily traded equity or debt securities. The cost of acquiring these securities is included in the account. 060 – Raw materials inventory – The amount of materials kept on hand for eventual inclusion in finished goods. All freight costs associated with the acquisition of raw materials are included in this account. 070 – Work-in-process inventory – The cost of partially completed units of production. Costs stored in this account include raw materials, and any raw materials or overhead used to date. 080 – Finished goods inventory – The cost of completed products that have not yet been shipped to customers. Costs stored in this account include all raw materials, direct labor, and overhead used during the production process. 090 – Reserve for obsolete inventory – A reserve fund that is held as a contingency against the eventual write-off of any types of inventory that no longer have a resale value. 100 – Fixed assets—Computer equipment – Purchased computer equipment exceeding the corporate capitalization limit that has an expected life of greater than one year. 110 – Fixed assets—Computer software – Purchased computer software exceeding the corporate capitalization limit that has an expected life of greater than one year. 120 – Fixed assets—Furniture and fixtures – Purchased furniture exceeding the corporate capitalization limit that has an expected life of greater than one year. 130 – Fixed assets—Leasehold improvements – Improvements made by the company to its leased properties, exceeding the corporate capitalization limit, that has an expected life of greater than one year. 140 – Fixed assets—Machinery – Purchased production equipment exceeding the corporate capitalization limit that has an expected life of greater than one year.

- 35. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes 150 – Accumulated depreciation—Computer equipment – The total of all depreciation charged against the computer equipment fixed asset account, net of disposed assets. This account has a credit balance. 160 – Accumulated depreciation—Computer software – The total of all depreciation charged against the computer software fixed asset account, net of disposed assets. This account has a credit balance. 170 – Accumulated depreciation—Furniture and fixtures – The total of all depreciation charged against the furniture and fixtures fixed asset account, net of disposed assets. This account has a credit balance. 180 – Accumulated depreciation—Leasehold improvements – The total of all depreciation charged against the leasehold improvement fixed asset account, net of disposed assets. This account has a credit balance. 190 – Accumulated depreciation—Machinery – The total of all depreciation charged against the machinery fixed asset account, net of disposed assets. This account has a credit balance. 200 – Other assets – An account in which minor asset items are stored that do not fit into any other asset account categories. 300 – Accounts payable – Both billed and accrued commitments to pay suppliers for services rendered or products shipped to the company. 310 – Accrued payroll liability – An obligation to pay wages to employees, but which has not yet been paid. 320 – Accrued vacation liability – An obligation to pay for earned vacation time to employees, but which has not yet been paid. 330 – Accrued expenses liability—Other – An account in which minor accrued expenses are stored, or those accrued expenses are stored, that do not occur on a recurring basis. 340 – Un-remitted sales taxes – Sales taxes to government entities that are a company obligation to make as a result of selling products or services into the geographic areas governed by those entities, but which have not yet been made. 350 – Un-remitted pension payments – Pensions payments that are an obligation of the company to make into the employee pension fund, but which have not yet been made. 360 – Short-term notes payable – Debt obligations that are due for payment in less than one year. 370 – Other short-term liabilities – An account in which minor liability items are stored that do not fit into any other liability account categories. 400 – Long-term notes payable – Debt obligations that are due for payment in more than one year. 500 – Capital stock – The amount of funds received from investors in exchange for the issuance of common or preferred stock. 510 – Retained earnings – Total corporate earnings since the creation of the company, less dividends and any prior period adjustments. 600 – Revenue – The sale of products or services, or receipts from investments, such as interest, royalties, or dividends. 700 – Cost of goods sold—Materials – The direct cost of materials associated with the sale of a tangible product. This includes all materials listed on a product’s bill of materials, plus all scrap incurred during production, less the resale value of any by-products. 710 – Cost of goods sold—Direct labor – The labor expense required to produce a product or service, which is limited to assembly labor. 720 – Cost of goods sold—Manufacturing supplies – The cost of supplies consumed when a product is manufactured. This includes all incidental machinery maintenance supplies and packaging materials.

- 36. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes 730 – Cost of goods sold—Applied overhead – The cost of manufacturing, excluding materials, direct labor, and supplies. Includes depreciation on manufacturing equipment and facilities, as well as factory administration, indirect labor, maintenance, production Employee’s benefits, quality control and inspection, production facility rent, repair expenses, rework labor, and spoilage. 800 – Bank charges – The expense associated with credit card fees, bank service charges, and the cost of printing checks. 805 – Benefits – The expense associated with medical insurance, dental insurance, long-term and short-term disability insurance, and health club reimbursement fees. All employee payroll deductions to co-pay benefits should be credited against this account. 810 – Depreciation – The expense associated with the periodic reduction of the value of fixed assets, in accordance with a standard value-reduction methodology. 815 – Insurance – The expense associated with key-man life insurance, business insurance, and workers’ compensation insurance. 825 – Office supplies – The expense associated with miscellaneous tangible office purchases, such as paper products, printer cartridges, and diskettes. 830 – Salaries and wages – The expense associated with employee pay, which includes salaries, wages, severance payments, signing bonuses, and accrued wages. 835 – Telephones – The expense associated with “800” phone service, incoming phone lines, and cell phones. The cost of phone equipment is charged either to office supplies or to fixed assets, depending upon the dollar-value purchased. 840 – Training – The expense associated with outsourced training suppliers, tests, and purchased training materials. It does not include travel costs associated with employee travel to training classes, nor the salary cost of in-house training personnel. 845 – Travel and entertainment – The expense associated with the travel of either employees or reimbursed contractors. Includes air fare, lodging, parking, and meals. 850 – Utilities – The expense associated with water, heat, waste removal, and electricity fees charged by utilities. 855 – Other expenses – Includes all incidental expenses under $500 that do not readily fall into any other category. Consult with the assistant controller before making entries into this account. 860 – Interest expense – The expense associated with the interest cost of revolving debt, interest on late payments to suppliers, and outstanding company bonds. Also includes accrued interest on unpaid interest expenses. 900 – Extraordinary items – Any expense that is both unusual and infrequent, such as a gain on a troubled debt restructuring or the loss of foreign assets due to governmental expropriation. No entries to this account are allowed without the controller’s approval. Other Common Terms and Definitions Used for Chart of Accounts Other definitions for accounts that are commonly used by the accounting staff include: 1. Travel and Subsistence Meals and lodging: Includes meals and lodging costs (hotel, motel, etc.) in accordance with company policy for reimbursement. Per diem allowances for meals and lodging are included here. Travel in private vehicle: Includes travel in employee-owned vehicles at the currently approved mileage reimbursement rate. Travel in rented vehicle: Includes daily car rental fees from outside providers. Travel in public carrier: Includes air, bus, and train travel.

- 37. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes Travel in motor pool vehicles: Includes charges for the use of company-owned vehicles at the approved rates. Costs of air travel for the company-owned air plane are included here. Other travel costs: Includes such incidental expenses as tips, telephone calls, taxis, tolls, and parking while on a company-authorized trip. Tips on meals are included in meal costs. Conference and registration fees: Includes registration fees for seminars, work shops, conferences, and similar meetings. Tuition for schools and workshops is included here. If meals and lodging fees included in registration fees cannot be separated, then they are included here. 2. Communications Postage: Includes postage charges for mailing, as well as service and rental fees for postage machines, and periodic service fees charged by online postage providers. Express postage: Includes all freight costs for express delivery services, including pickup fees. Cell phones: Includes the basic monthly fees, as well as roaming charges, for all issued cell phones. Telephone local service: Includes the basic monthly charges for all phones. Telephone long distance: Includes the charges for all long distance services, including the WATS line, line rentals, and telegraph charges. Telephone installation and maintenance: Includes all charges for the installation of phones and subsequent maintenance of the phone system. 3. Marketing Advertising: Includes the cost of classified advertising for employee hiring, as well as required advertising for published purchasing bids. Publicity and public information: Includes the cost of radio, television, and live shows promoting the company, as well as related layout and copy costs. 4. Rents Rental of buildings and floor space: Includes payments to others for buildings, rooms for events, and floor space in buildings for special events. Rental of housing facilities and meeting rooms is included here. Rental of computer equipment: Includes the rental or lease cost of computer software and equipment, such as payments on operating leases. Other rentals: Includes any rental that cannot be recorded in other rental accounts. 5. Repairs and Maintenance Repairs, streets and parking: Includes repairs and other maintenance on roads, streets, drives, and parking lots. Repairs, building and grounds: Includes wages and material costs of repairing, cleaning, and maintaining buildings and grounds. Outside contractor costs for this purpose are recorded here. Repairs, office equipment: Includes the costs of repairing and maintaining office equipment such as furniture, copiers, and facsimile machines. It does not include maintenance on the phone system. Maintenance contracts, equipment: Includes the annual contract costs for maintenance contracts on office equipment. Repairing and servicing other equipment: Includes the costs of repairing and servicing machinery, engineering equipment, laboratory equipment, shop equipment, and other equipment not classified in the preceding repair accounts.

- 38. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes 6. Fees, Professional Engineering fees: Includes out-of-pocket fees for professional engineering services. Auditing fees: Includes the costs of auditing fees to outside independent auditors. Other incidental costs of the audit, such as supplies, telephone, postage and printing charges related to the audit, are included here. Medical fees: Includes direct payments to others for medical services, including pre-employment physicals and lab tests. Legal fees: Includes all fees paid to attorneys, appraisers, notaries, and witnesses, in addition to court costs and legal document recording fees. Laboratory and testing fees: Includes outside laboratory fees and fees paid to outside agencies for testing services other than medical services. Consultant expense reimbursements: Includes travel costs paid to consultants and other non- employees. 7. Other Contractual Services Insurance and fidelity bonds: Includes the cost of all casualty and liability insurance and fidelity bond coverage. Dues: Includes approved dues for company memberships in professional organizations. Subscriptions: Includes the cost of subscriptions to newspapers, magazines, and periodicals. Computer software acquisitions: Includes the initial cost of acquiring operating or systems software packages. Included is the purchase price, related freight, and software manuals. Computer software maintenance: Includes the annual maintenance fees to maintain purchased software systems. 8. Maintenance Supplies Land improvement supplies: Includes asphalt, cement, joint fillers, curbing, and so forth used in repairing or replacing roads, sidewalks, and parking lots on company property. Building construction supplies: Includes lumber, caulking, steel, fabricated metal parts, flooring, ceiling tiles, plaster, lime, and other materials used in repairing or renovating buildings. Paints and preservatives: Includes interior and exterior paints, wood preservatives, and road striping materials used for remodeling or maintenance. Hardware, plumbing, and electrical supplies: Includes all hardware, plumbing parts and accessories, and electrical wire or parts, including lights used in maintaining or renovating buildings. Custodial supplies and cleaning agents: Includes all custodial supplies of an expendable nature, such as cloths, brooms, cleaning compounds, mops, or pails. 9. Office Supplies Printing, binding, and padding: Includes the cost of printing, binding, and padding paid to outside contractors. Duplication and reproduction: Includes the paper, toner, and other supplies used in the company copy machines. Office supplies: Includes all office supplies and materials, such as pens, paper, pencils, staples, paper clips, and so forth. 10. Equipment Supplies Fuels: Includes vehicle fuels (gasoline, diesel fuel, propane) purchased for motor pool vehicles or airplanes.

- 39. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes Lubricating oils and greases: Includes lubricating oils and greases used for all vehicles and machinery. Tires and tubes: Includes the purchase of tires and tubes for all vehicles in the company motor pool. Repair and replacement parts: Includes the purchase of vehicle and machinery repair and replacement parts and supplies. Shop supplies: Includes the cost of shop supplies, such as shop rags, windshield cleaner, glues and cements, brushes, degreasers, solvents, and so forth, used in equipment repair and maintenance operations. Small tools: Includes small tools used in manufacturing operations that are below the corporate capitalization limit. TASK B In addition to its Australian business, Big Red Bicycle is considering manufacturing a new range of cheaper bicycles in Indonesia. The following information is available: The Indonesian plant has capacity to manufacture 8,000 units. • Big Red Bicycle's strategic goal is to generate a pre-tax profit of $1,000,000 for the next financial year for Indonesian operations. • Clients will pay a maximum of $500 per bicycle • Possibility exists for move to Indian plant with capacity for 10,000 units. • Market for bicycles is growing rapidly and BRB will be able to sell all units produced. • Limited ability to renegotiate costs with suppliers. • Pricing and cost information is as follows. a. How many units at current variable cost would need to be produced to achieve profit target (show calculations). Profit target --> $1,000,000 Bicycle sales price --> $500 Current variable cost --> $250 Fixed costs --> $1,280,000 Units = ( fixcost+ profit sales price— cost ) ( 1,280,000+1,000,000 500 — 250 ) = 9,120 units b. What the variable costs per unit would need to be to achieve profit target at current manufacturing capacity (show calculations). Gross margin = sales price — variable cost

- 40. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes = 500 — 250 = 250 dollars New gross margin = ( fix cost+ profit units ) = ( 1,280,000+1,000,000 8,000 ) = 285 dollars New variable cost = sales price — new gross margin = 500 — 285 = 215 dollars 2.Make one written recommendation based on your analysis. To support your recommendation ensure you refer to the organisational needs or situation, and any analytical techniques used. You may also suggest possible actions for BRB to take depending on possible future scenarios. Based on calculations above and on the Indonesian scenario, BRB should produce 9,120 bicycles to achieve the profit target. As the Indonesian plant has the capacity of producing 8,000 bicycles, the profit will not be achieved. Then, the variable cost of should decrease in 14%. To decrease the variable cost we could look at fixed costs: suppliers. Even though it has a limited ability to negotiate with suppliers, it should be reviewed: material, cost of manufacturing, and also offering an extended contract with suppliers if they reduce their costs. TASK C Soon you will need to prepare a Business Activity Statement (BAS) for the first quarter on 2012/13. Bicycle price per unit $500 (excl. GST) Current variable costs per unit $250 Fixed costs $1,280,000 1. State how many years you will need to keep GST records in order to satisfy ATO requirements. It is necessary to keep GST records to accomplish ATO requirements for five years.

- 41. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes 2. Complete the GST budget on the following page to anticipate GST liability. July August September Budgeted cash receipts Incurring GST: Cash sales 20,000 10,000 10,000 Cash revenue (besides sales) 0 0 0 Cash receipts from sale of assets (not stock) 0 0 0 Total receipts for GST 20,000 10,000 10,000 Budgeted non-cash receipts Incurring GST: Debtors sales 180,000 230,000 150,000 Total non-cash receipts 180,000 230,000 150,000 Total budgeted receipts incurring GST 200,000 240,000 160,000 Budgeted cash payments incurring GST: Cash purchases of stock 0 0 0 Cash expenses 4,300 5,200 5,250 Total cash receipts incurring GST 4,300 5,200 5,250 Budgeted credit payments incurring GST: Credit purchases of stock incurring GST 25,000 30,000 25,000 Credit purchases of assets (besides stock) 4,300 5,200 5,250 Total cash payments incurring GST 29,300 35,200 30,250 Total budgeted cash payments incurring GST 33,600 40,400 35,500

- 42. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes July August September GST cash budget calculations a) Cash receipts $ 2,430 $ 1,520 $ 1,525 b) Cash payments $ 2,930 $ 3,520 $ 3,025 c) GST liability $ 5,360 $ 5,040 $ 4,550

- 43. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes Task D: An action plan to implement and monitor the recommendation. Ensure you include appropriate activities, monitoring, timelines and accountabilities. Recommendation Training of staff in credit terms Rational To reduce the % of debtors for longer than 30 Rational days and ensure that company's policies are followed Action Budget Person responsible Time Monitor To find out reason why debtors are going longer than 30 days $800 Stuart LaRoux Op. Gn. Manager 1 weeks Analyse report and create a spreadsheet with the common reasons To train staff in credits policies and procedures $2,000 Holly Burke HR manager 1 weeks Evaluate them with an internal audition To track that staff members who struggle with credit terms information and the topics $1,000 Holly Burke HR manager 2 weeks To audit staff members on credit information To create a training based on team needs and to train the team $4,500 Sam Gellar Sales G. Manager 4 weeks: 2 to create + 2 training Control their performance and create a fortnight report with their sales and payments conditions To evaluate team member after training $2000 Sam Gellar Sales G. Manager 2 weeks Monthly evaluation to keep track of those who still struggle

- 44. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes Task E Reflecting on the tasks you have undertaken and on your knowledge of financial management and planning principles: 1. Describe basic accounting principles Capital budgeting has five principles that play a crucial role in the allocation of money and the process of capital budgeting. The five principles are; (1) decisions are based on cash flows, not accounting income, (2) cash flows are based on opportunity cost, (3) The timing of cash flows are important, (4) cash flows are analyzed on an after tax basis, (5) financing costs are reflected on project’s required rate of return. (1) Relevant cash flows are based on incremental cash flows. This represents the changes in cash flow if the project is undertaken. Aspects of cash flow that affect capital budgeting are sunk costs and externalities. These are both costs that cannot be avoided. Sunk costs are costs that are unavoidable, even if the project is undertaken. Externalities are side effects of a project that affect other firm cash flows. (2) Cash flows are based on opportunity cost. In other words, it is the cash flow that will be lost due to the financing of a project. These are cash flows that are accumulated by assets the firm already owns and would be sunk if the project under consideration is undertaken. (3) The timing of cash flow is crucial because it is dependent on the time value of money. Cash flow that is received now will be worth more in the future if it were to be received later. (4) Cash flows are measured on an after tax basis. It is useless to measure cash flow before taxes because it is not its present value. Firm's value is based on cash flow that a firm gets to keep, not the money that is sent to the government. (5) Financing costs are reflected on project's required rate of return. Rate of return is an aspect of financing that has potential risks. Project's that are expected to have a higher rate of return than their cost of capital will increase the value of the firm. 2. Describe cash flows Cash flow is the net amount of cash and cash-equivalents moving into and out of a business. Positive cash flow indicates that a company's liquid assets are increasing, enabling it to settle debts, reinvest in its business, return money to shareholders, pay expenses and provide a buffer against future financial challenges. Negative cash flow indicates that a company's liquid assets are decreasing. Net cash flow is distinguished from net income, which includes accounts receivable and other items for which payment has not actually been received. Cash flow is used to assess the quality of a company's income, that is, how liquid it is, which can indicate whether the company is positioned to remain solvent. 3. Describe ledgers and financial statements Ledger is a book (or record) for collecting chronological transaction data from a journal, and organizing entries by account. The ledger provides information on the transaction history and current balance in each account, throughout the accounting period. At the end of the period, ledgers

- 45. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes become the authoritative source of data for building a firm's financial accounting reports, including the income statement and balance sheet. Financial statements for businesses usually include income statements, balance sheets, statements of retained earnings and cash flows. It is standard practice for businesses to present financial statements that adhere to generally accepted accounting principles (GAAP) to maintain continuity of information and presentation across international borders. Financial statements are often audited by government agencies, accountants, firms, etc. to ensure accuracy and for tax, financing or investing purposes. 4. Describe profit and loss statements. A profit and loss statement (P&L) is a financial statement that summarizes the revenues, costs and expenses incurred during a specific period of time, usually a fiscal quarter or year. These records provide information about a company's ability—or lack thereof—to generate profit by increasing revenue, reducing costs, or both. The P&L statement is also referred to as "statement of profit and loss", "income statement," "statement of operations," "statement of financial results," and "income and expense statement." Summarise your reflections in a short, written statement and submit this to your assessor. You may revisit the five fundamental principles of accounting. For example, the list is said to be crucial to effective management decision-making: 1. Control — managers need to control and monitor the business. 2. Relevance — decision-makers need information that is timely, useful etc. 3. Compatibility — the accounting systems should match the aims of a company. 4. Flexibility — the accounting systems need to adapt to the company's needs. 5. Cost-benefit — the benefits of the accounting information system need to outweigh the cost. What do you think? For an effective management of budget and financial plans it is very important to look at the many principles, techniques and information of accounting. A good management that sets plans and policies which are, formally established and expressed in financial results, allows the managers know the operating results of the company, and then perform the necessary controls to ensure that these results are achieved and the possible variations are analyzed, evaluated and corrected.

- 46. BSBFIM501- DIPLOMA OF LEADERSHIP AND MANAGEMENT ASSESSMENT BSBFIM501 — MANAGE BUDGETS AND FINANCIAL PLANS Assessment task 4 - review and evaluate financial management processes Reference List Corporations Act 2001— Wikipedia — Viewed on 10/1/2018 (https://en.wikipedia.org/wiki/Corporations_Act_2001) Australian Securities and Investments Commission Act 2001— Federal Register of Legislation — Viewed on 10/1/2018 (https://www.legislation.gov.au/Details/C2011C00004) Our role — Australian Securities & Investments Commission — Viewed on 10/10/2018 (http://asic.gov.au/about-asic/what-we-do/our-role/#what) Record keeping — Australian Taxation Office—Viewed on 10/1/2018 (https://www.ato.gov.au/Non-profit/your-organisation/records,-reporting-and-paying-tax/record- keeping/) Principles of Capital Budgeting —Valuation Academy — Viewed on 10/1/2018 (http://valuationacademy.com/principles-of-capital-budgeting/) Budgeting Techniques— Fleming & Co. Certified Public Accountants— Viewed on 10/1/2018 (http://cparus.com/tax-information/business/budgeting-techniques/) Accounting Basics: Financial Statements — Investopedia — Viewed on 11/1/2018 (http://www.investopedia.com/university/accounting/accounting5.asp) Improving cash flow using credit management —Chartered Institute of Management Accountants —Viewed on 11/1/2018 (http://esyne.gr/wp-content/uploads/2016/01/CIMA_improving_cashflow_using_credit_mgm.pdf) Accounting term and definitions for chart of accounts — Accounting Financial and Tax— Viewed on 11/1/2018 (http://accounting-financial-tax.com/2008/08/accounting-term-and-definitions-for-chart-of- accounts/) Cash Flow — Investopedia — Viewed on 14/1/2018 (http://www.investopedia.com/terms/c/cashflow.asp) Ledger, General Ledger, and Nominal Ledger Explained — Building the Business Case — Viewed on 16/1/2018 (https://www.business-case-analysis.com/ledger.html) Financial Statements — Investopedia — Viewed on 14/1/2018 (http://www.investopedia.com/terms/f/financial-statements.asp) Profit and Loss Statement (P&L) Definition —Investopedia — Viewed on 14/1/2018 (http://www.investopedia.com/terms/p/pIstatement.asp#ixzz40We0Bm5W)