Downloaded 322 times

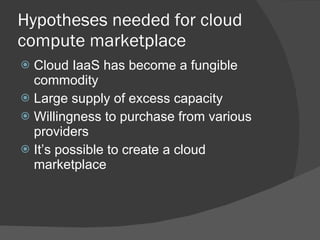

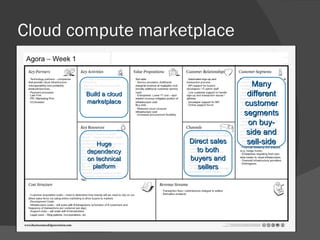

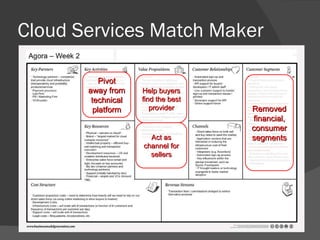

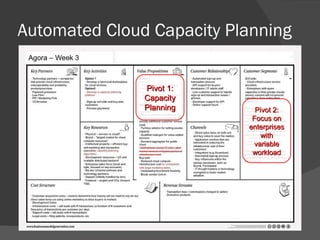

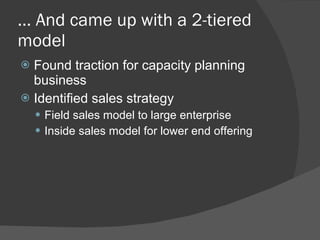

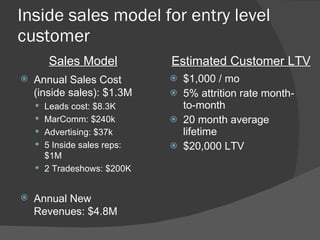

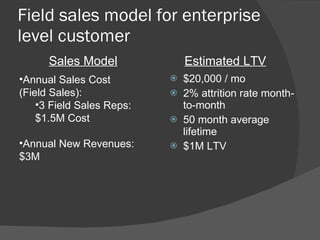

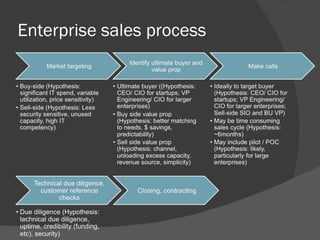

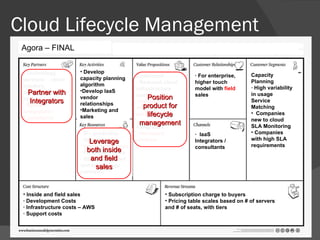

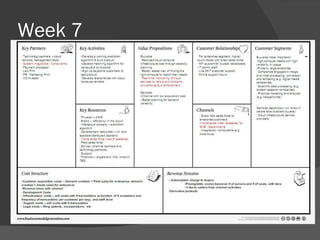

The document discusses the development of a business model for a cloud computing marketplace. It describes how the founders conducted customer interviews, analyzed the market, and pivoted their business model and product focus multiple times based on feedback. They ultimately developed a two-tiered sales model focusing on capacity planning and cloud lifecycle management, targeting enterprises through both inside and field sales with the help of cloud consulting partners.

![Xoom park bmc_international_new_sp [autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/xoomparkbmcinternationalnewspautosaved-120212053250-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)