Download to read offline

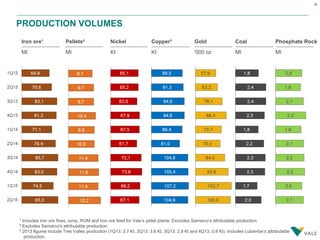

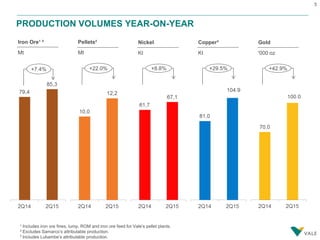

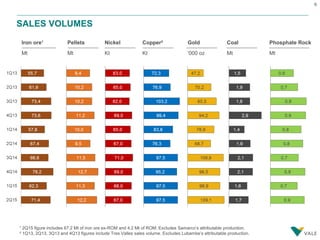

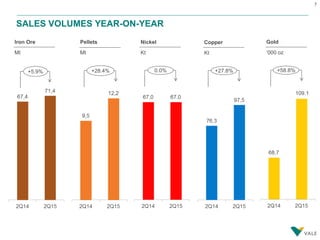

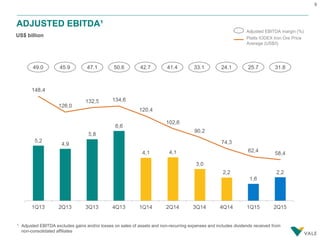

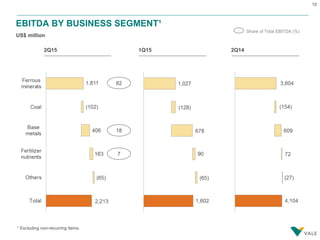

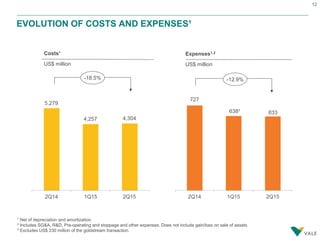

The document presents Vale's operational and financial performance for Q2 2015, highlighting production and sales volumes across various minerals, including iron ore, nickel, and gold, with year-on-year increases. It discusses financial metrics such as adjusted EBITDA and the impact of pricing systems on revenue, alongside capital expenditures and the company's debt position. Key risks and uncertainties affecting future performance are noted, including global economic factors and regional operational challenges.