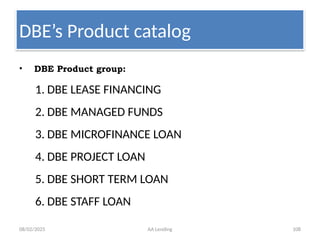

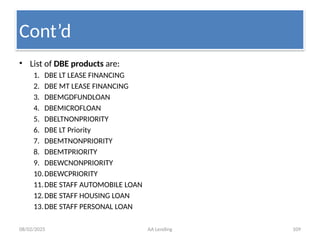

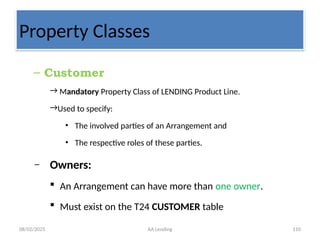

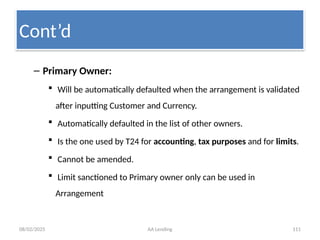

Overview of AA Lending, Product Building Concept

business components used in Product Building/Property classes/

Banks are increasingly adopting IT based solutions, for providing better services to their customers at a minimal cost

Core banking is a software based system that provides end to end functionalities for a bank’s main business process.

![E banking by sanjeev kumar chaswal [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/e-bankingbysanjeevkumarchaswalcompatibilitymode-130122093515-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)