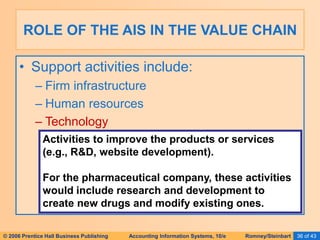

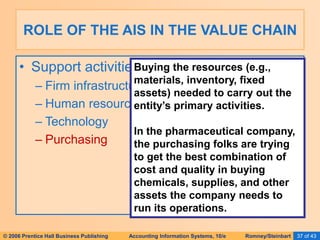

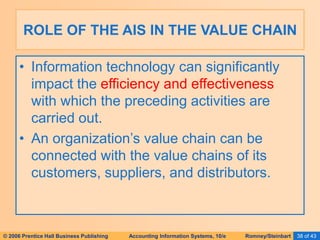

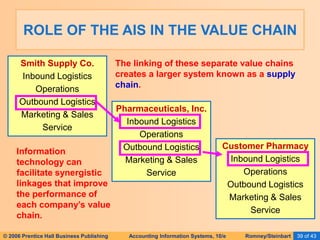

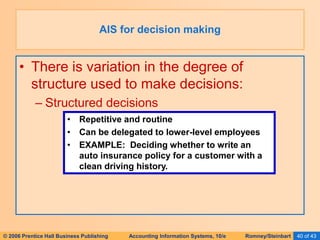

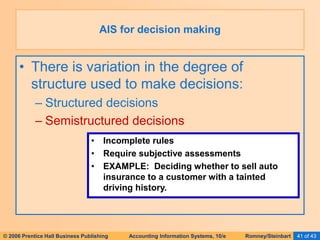

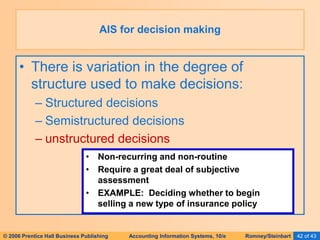

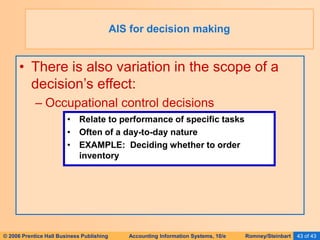

The document is an introductory chapter about accounting information systems from a textbook. It discusses key concepts like what a system, data, and information are. An accounting information system (AIS) is defined as a system that collects, records, stores, and processes data to produce information for decision makers. The chapter explains why studying AIS is important for accounting careers and discusses the role of the AIS in adding value within an organization's processes.