The document provides an overview of the course material for ACC 410 Entire Course Material- Auditing. It includes 14 discussion questions and assignments covering topics such as:

- The differences between internal and external audit staff relationships with a company.

- Conditions under which different types of audit reports may be issued, such as unmodified or qualified reports.

- Cases involving compliance with generally accepted auditing standards and procedures for topics like analytical procedures, internal controls, audit programs, and ethics.

The material asks students to evaluate statements, analyze case studies, describe audit processes, and discuss standards in order to demonstrate understanding of fundamental auditing concepts. Students are also instructed to respond to classmates' postings on the various discussion

![any, will this situation have on your audit report for the current year? Remember to complete all

parts of the problems. Do not forget to show the necessary steps and explain how you attained

that outcome. Respond to at least two of your classmates’ postings.

Audit Reports. The auditors do not believe that certain lease obligations have been reflected in

conformity with generally accepted accounting principles in the client’s financial statements.

What type of opinion should the auditors issue if they decide that the exceptions are immaterial?

Material? Very material? Remember to complete all parts of the problems. Do not forget to show

the necessary steps and explain how you attained that outcome. Respond to at least two of your

classmates’ postings.

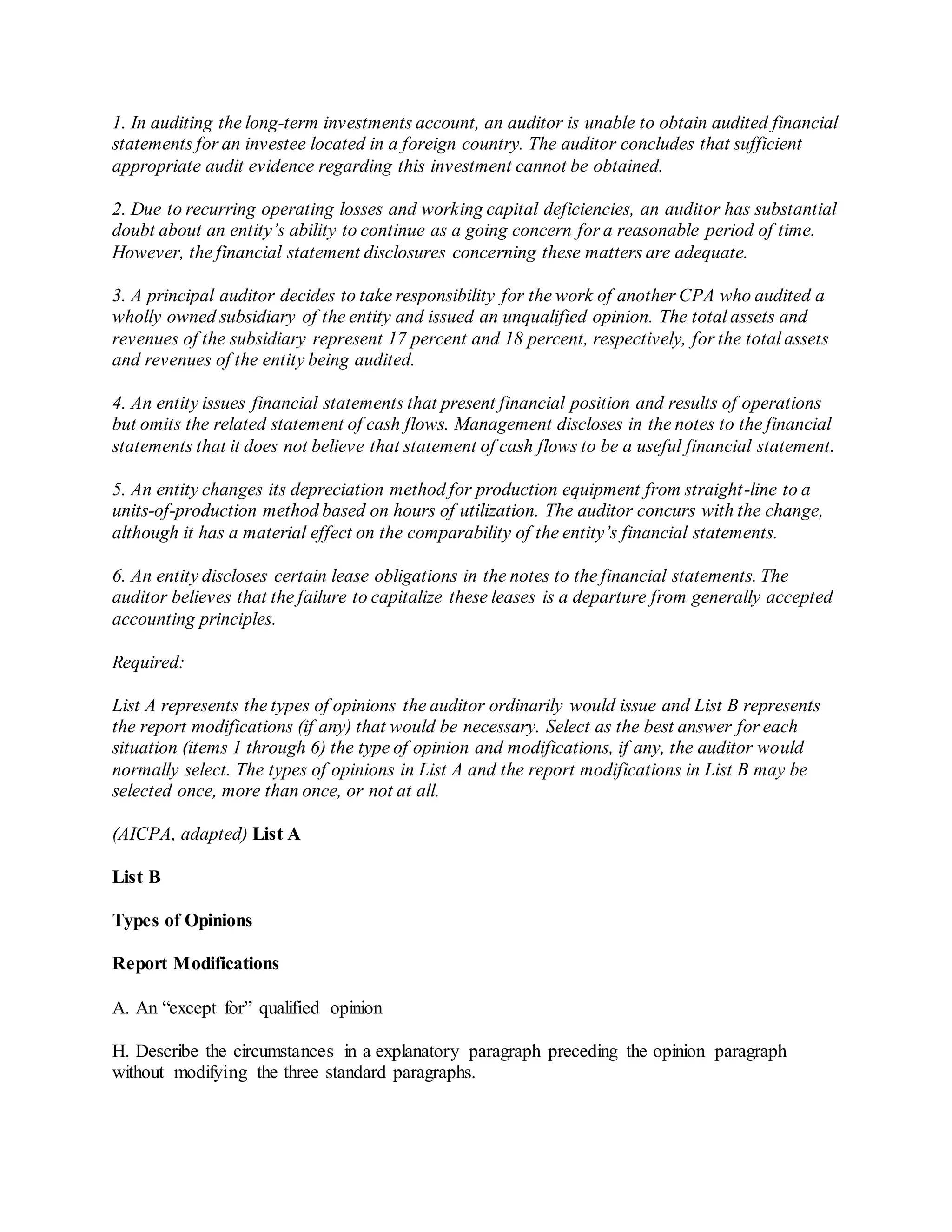

Audit Report Modifications. Complete problem below. List a represents the types of opinions

the auditor ordinarily would issue and List B represents the report modifications [if any] that

would be necessary. Select as the best answer for each situation [items 1 to 6] the type of opinion

and modifications, if any, the auditor would normally select. The types of opinions in List A and

the report modifications in List B may be selected once, more than once, or not at all. The paper

should be 2-3 pages.

Problem:

Items 1 through 6 present various independent factual situations an auditor might encounter in

conducting an audit. For each situation assume:

Assume:

The auditor is independent.

The auditor previously expressed an unqualified opinion on the prior year’s financial

statements.

Only single-year (not comparative) statements are presented for the current year.

The conditions for an unqualified opinion exist unless contradicted in the factual situations.

The conditions stated in the factual situations are material.

· No report modifications are to be made except in response to the factual situation.

Situations:](https://image.slidesharecdn.com/acc410entirecoursematerial-auditing-150408164639-conversion-gate01/75/c-8-2048.jpg)

![B. An unqualified opinion

I. Describe the circumstances in an explanatory paragraph following the opinion paragraph

without modifying the three standard paragraphs.

C. An adverse opinion

J. Describe the circumstances in an explanatory paragraph preceding the opinion paragraph, and

modify the opinion paragraph.

D. A disclaimer of opinion

K. Describe the circumstances in an explanatory paragraph following the opinion paragraph, and

modify the opinion paragraph.

E. Either an “except for” qualified opinion or an adverse opinion.

L. Describe the circumstances in an explanatory paragraph preceding the opinion paragraph, and

modify the scope and opinion paragraphs.

F. Either a disclaimer of opinion or an “except for” qualified opinion.

M. Describe the circumstances in an explanatory paragraph following the opinion paragraph, and

modify the scope and opinion paragraphs.

G. Either an adverse opinion or a disclaimer of opinion

N. Describe the circumstances within the scope paragraph without adding an explanatory

paragraph.

O. Describe the circumstances within the opinion paragraph without adding an explanatory

paragraph.

P. Describe the circumstances within the scope and opinion paragraphs without adding an

explanatory paragraph.

The final paper will be based on Appendix 6C Illustrative Audit Case: Keystone Computers at

pages 237-244 in your text. Write, in outline format but in complete sentences, a 6 to 10 page

audit plan. It is recommended that you look at Figure 18.8 on page 708, which shows the control

objectives related to accounts receivable.

In your audit plan cover the steps necessary to determine if you should select the client, the

internal control procedures which need to be reviewed, the substantive tests [using accounts

receivable a guide], and the final reporting steps. Based on the actual facts in the case determine

the emphasis you want to place on various accounts. Also reflect back over your entire

accounting program and think about how the accounts are interrelated. For example, when](https://image.slidesharecdn.com/acc410entirecoursematerial-auditing-150408164639-conversion-gate01/75/c-10-2048.jpg)

![[ON-DEMAND WEBINAR] Manufacturing Education Day 2020 Addresses PPP Loans, R&D...](https://cdn.slidesharecdn.com/ss_thumbnails/manufacturingdayslides-201005180957-thumbnail.jpg?width=640&height=640&fit=bounds)