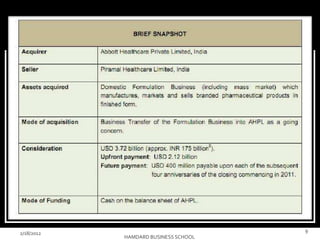

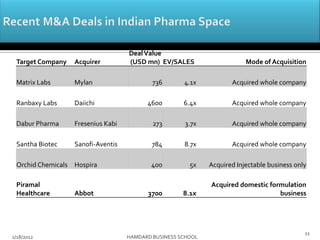

The document summarizes the acquisition of Piramal Healthcare Limited's domestic formulation business by Abbott Healthcare Private Limited. Some key details include: - Abbott acquired Piramal's domestic branded generics business for $3.72 billion to expand in the growing Indian market. - The deal will make Abbott a leader in various therapeutic segments in India such as gastrointestinal, vitamins/nutrients, and dermatology. - The valuation for the deal was 8.1 times sales, higher than typical generics valuations but provides Abbott access to India's large population and growth opportunities.