The document discusses various aspects of accounting for small businesses, including:

- Types of business ownership like sole proprietorships, partnerships, corporations, and LLCs.

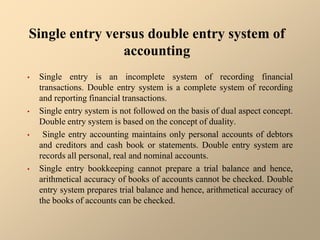

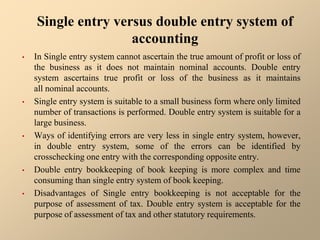

- Accounting systems like single entry and double entry accounting. Single entry records transactions only once while double entry uses debits and credits.

- Accounting methods like cash basis and accrual basis for recording revenues and expenses.

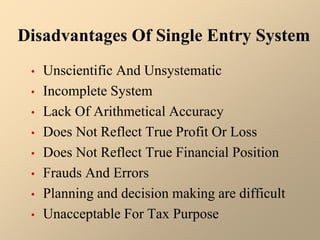

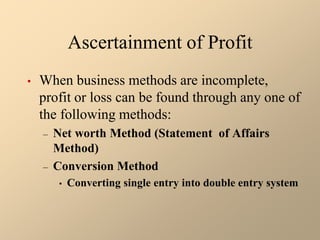

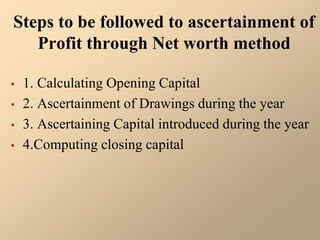

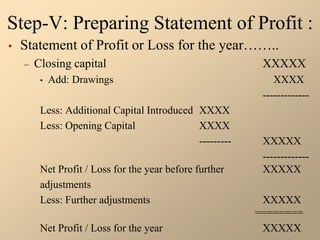

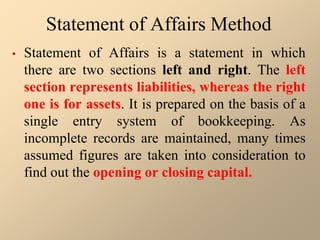

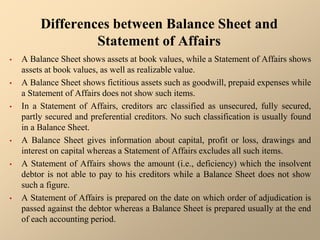

- Features of single entry accounting including its simplicity but incompleteness compared to double entry accounting. Methods for determining profit under single entry using net worth or conversion methods are also outlined.