Download as PDF, PPTX

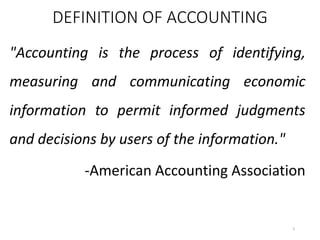

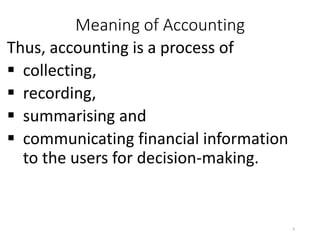

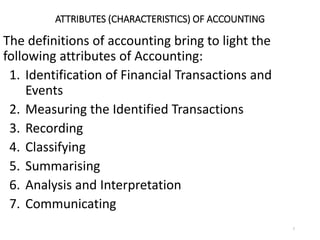

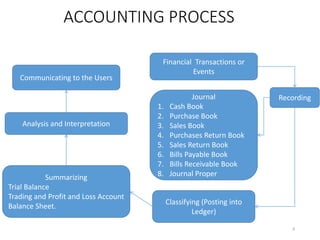

The document serves as an introduction to accounting, detailing its definitions, processes, and objectives. It differentiates between bookkeeping and accounting, explaining that bookkeeping is a subset focused on record-keeping, while accounting encompasses broader functions like analysis and reporting. Various accounting systems, concepts, and conventions are outlined, emphasizing the importance of accurate financial communication and decision-making.

![MEFA_UNIT-IV_Part-1[1].pptx kkkkkkkkkkkkkkkkkkkkkkk](https://cdn.slidesharecdn.com/ss_thumbnails/mefaunit-ivpart-11-250504093650-39e41996-thumbnail.jpg?width=640&height=640&fit=bounds)