Download to read offline

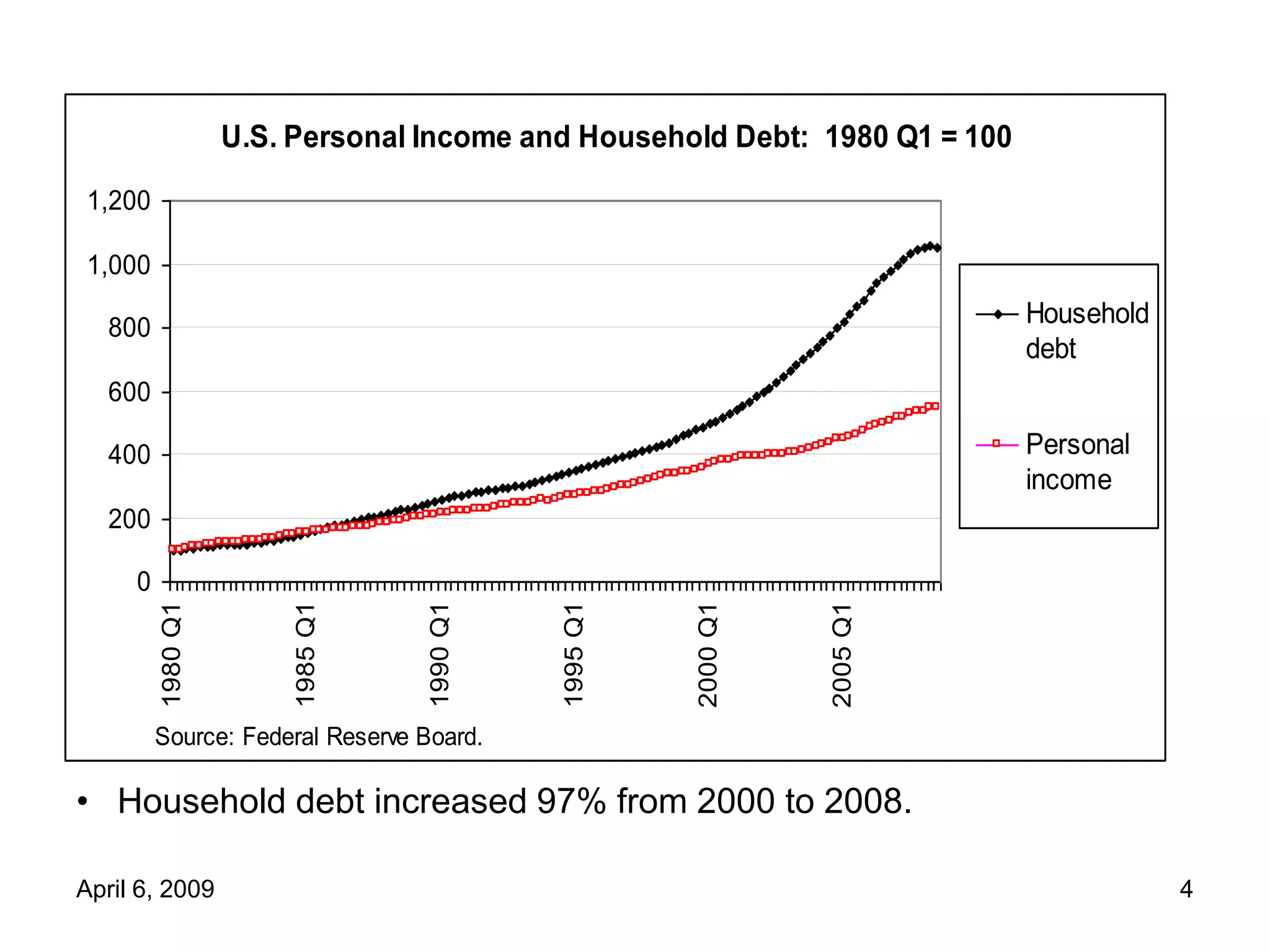

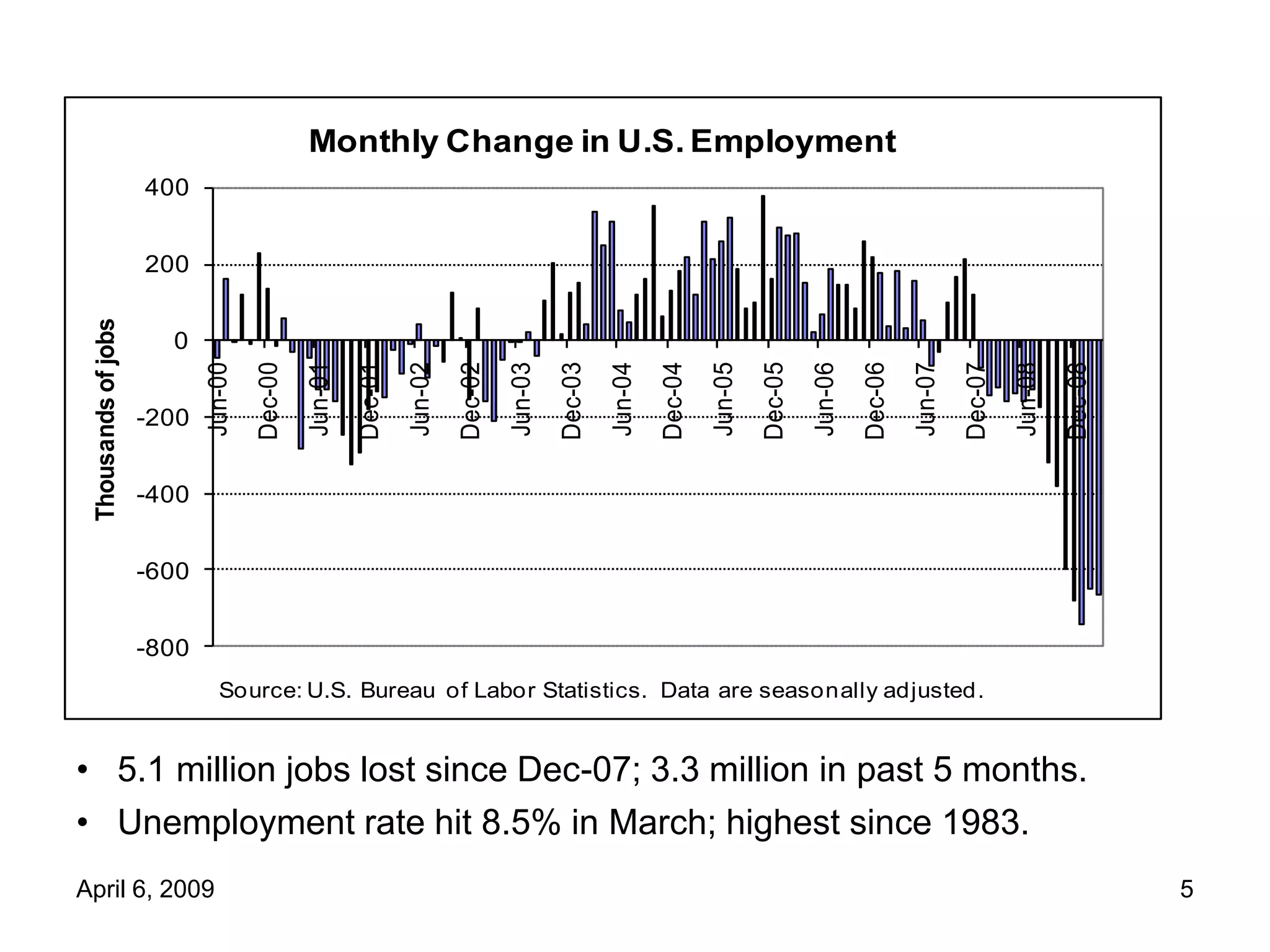

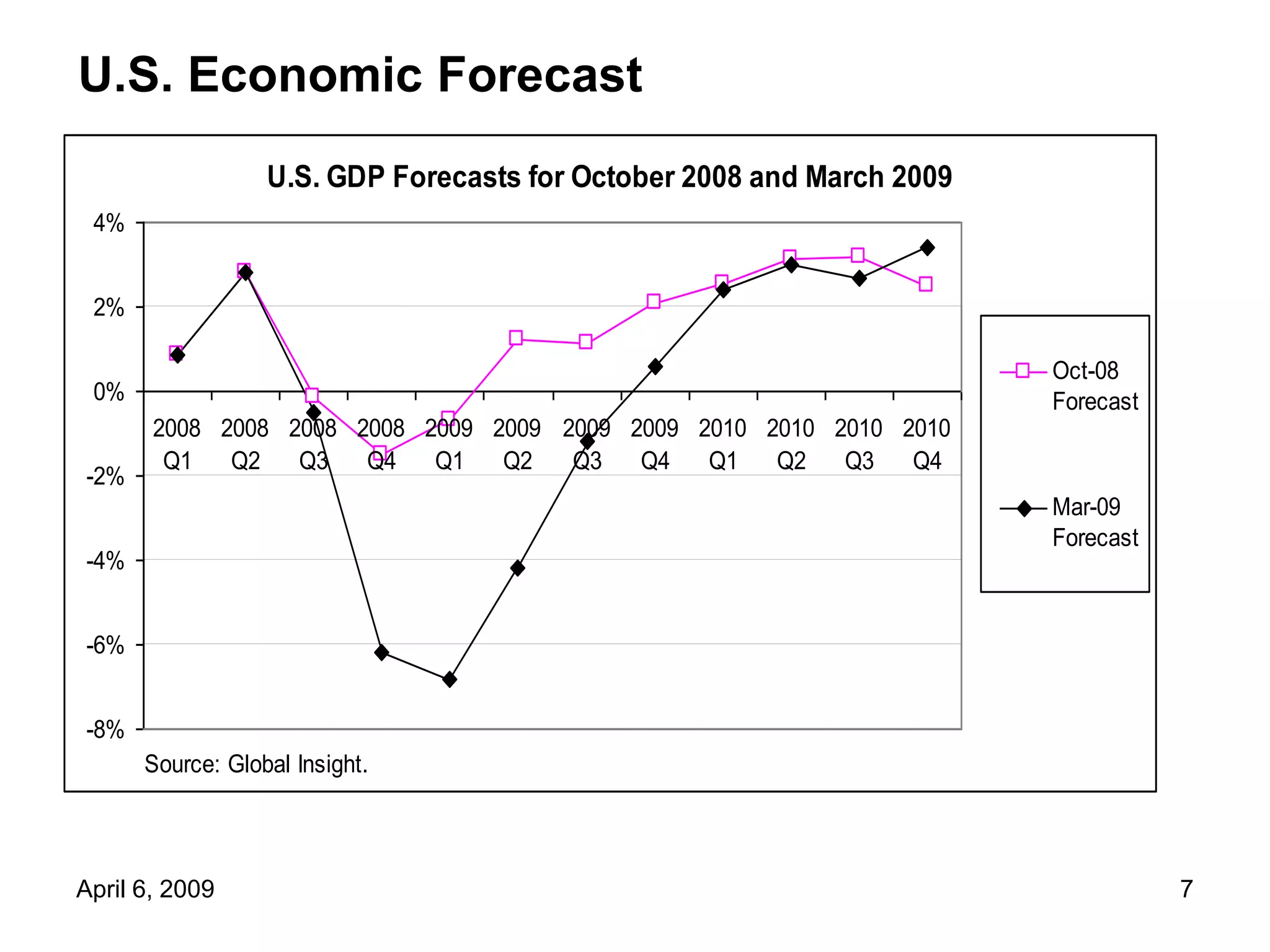

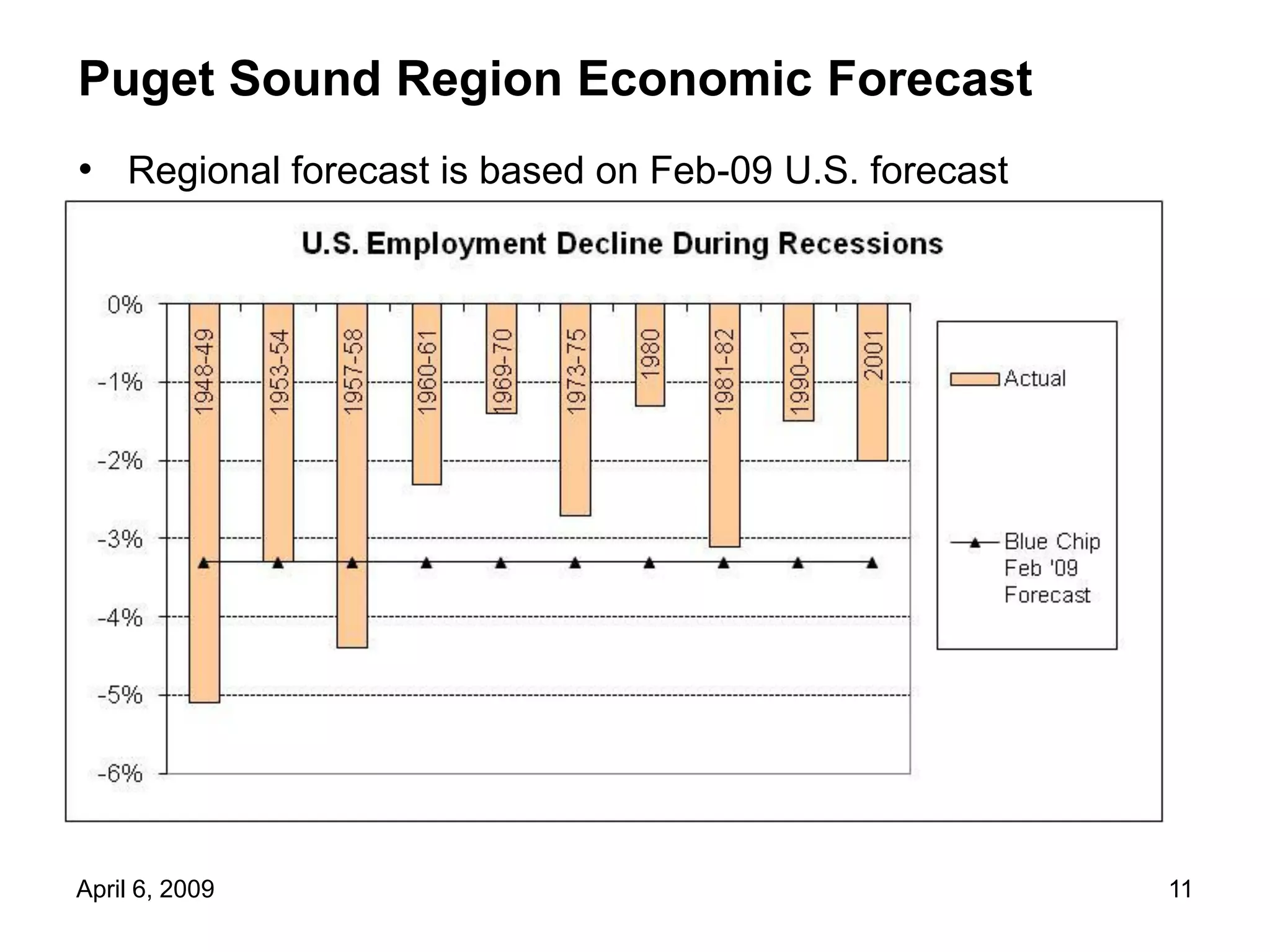

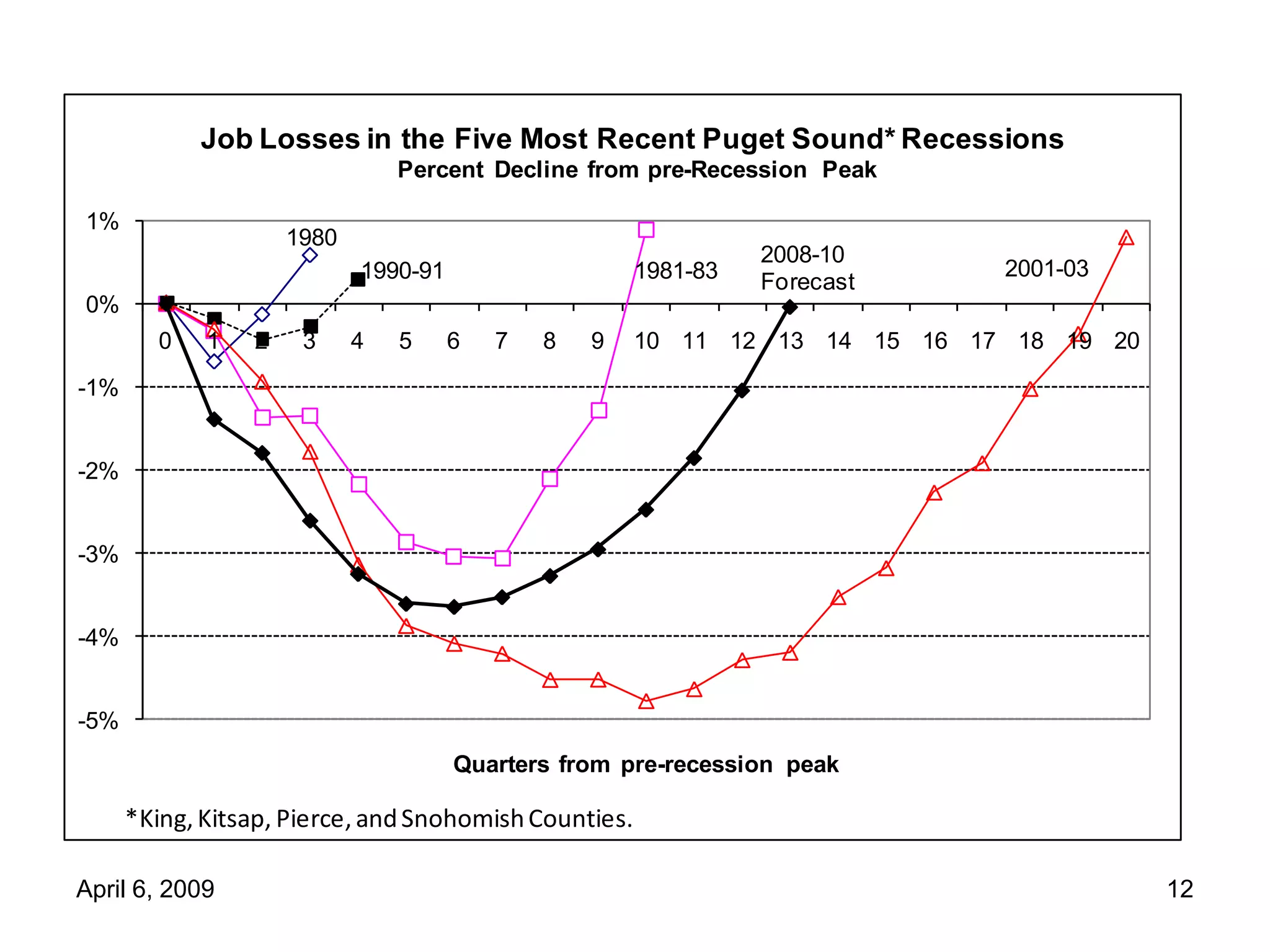

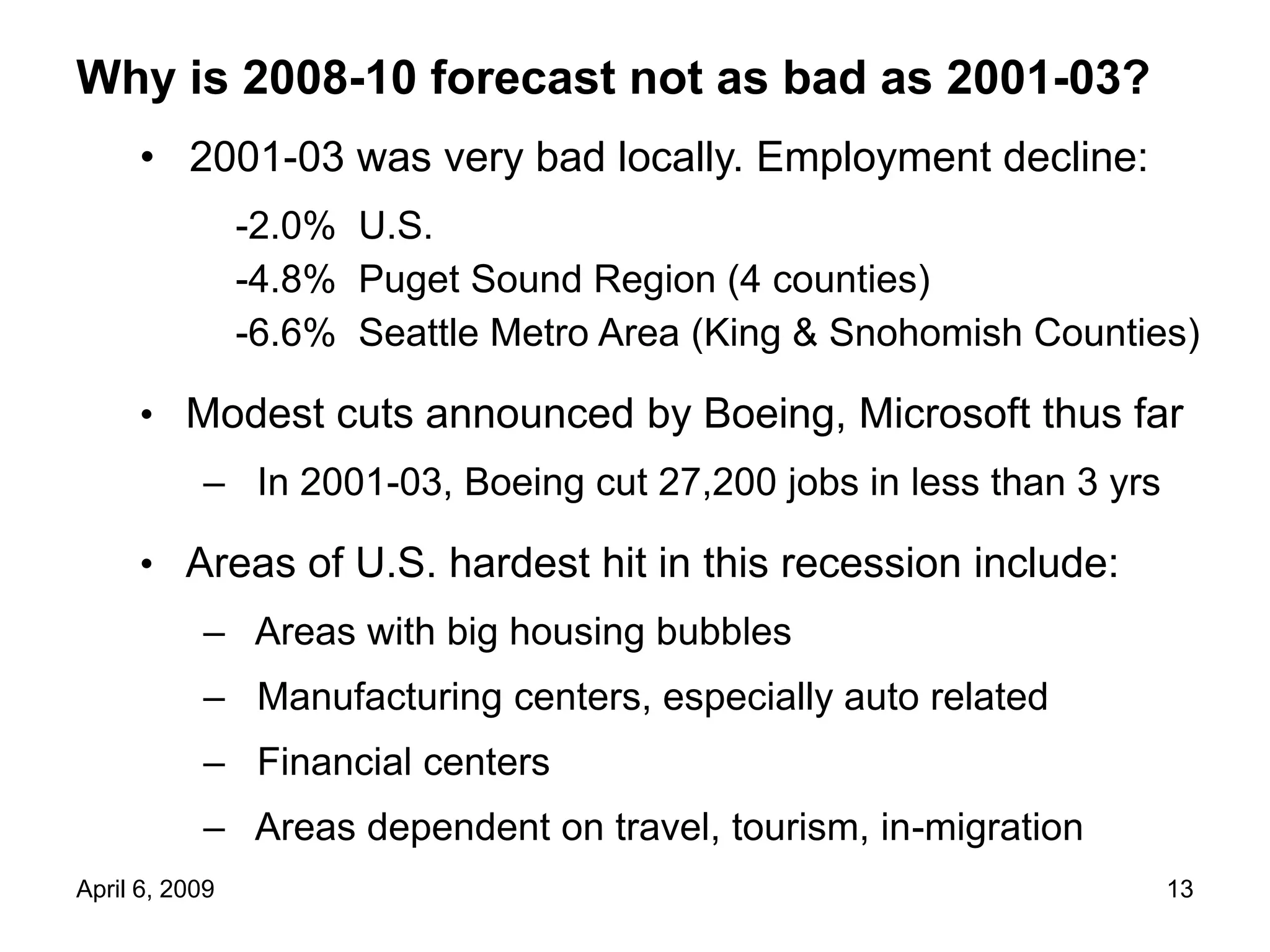

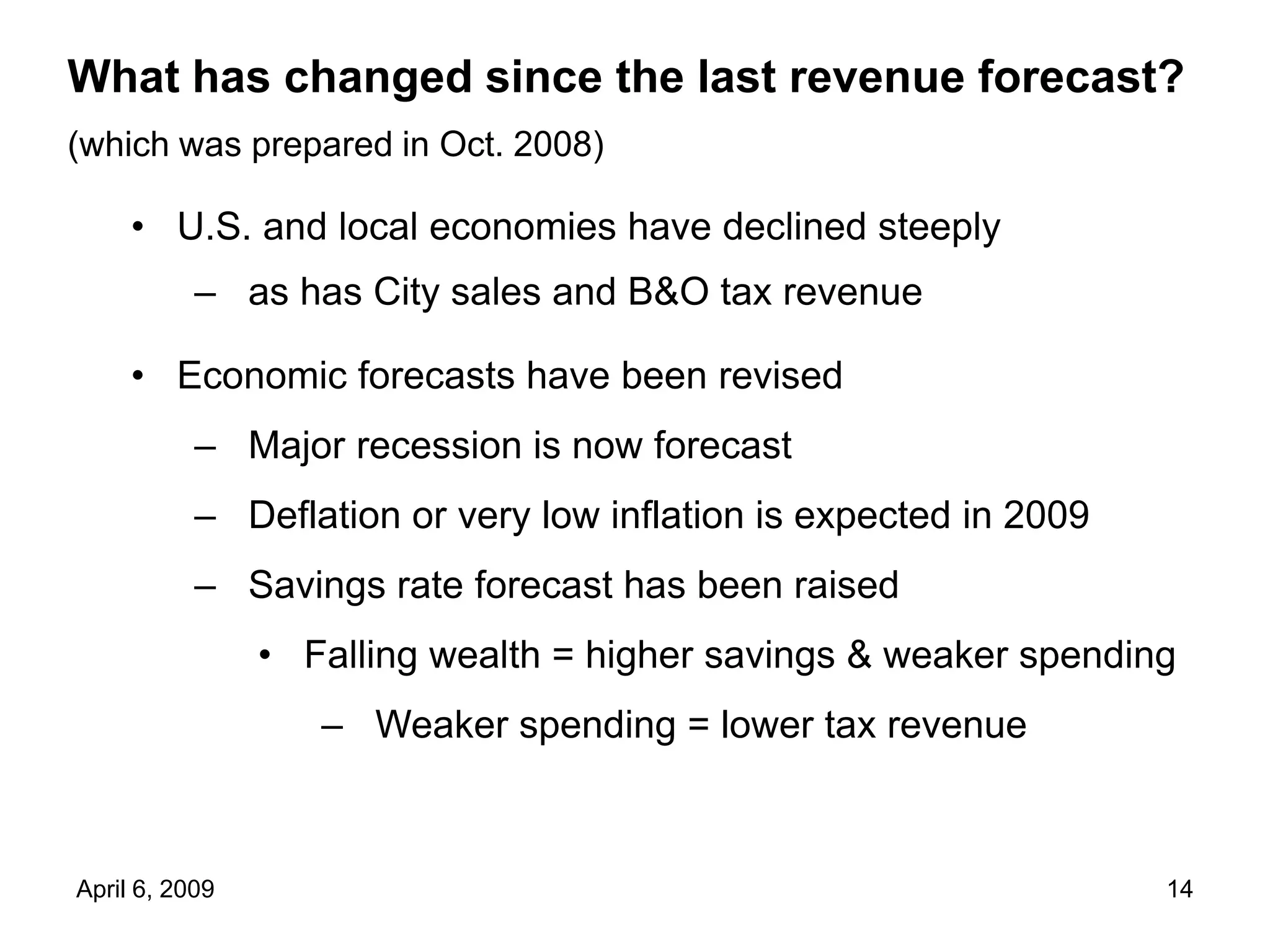

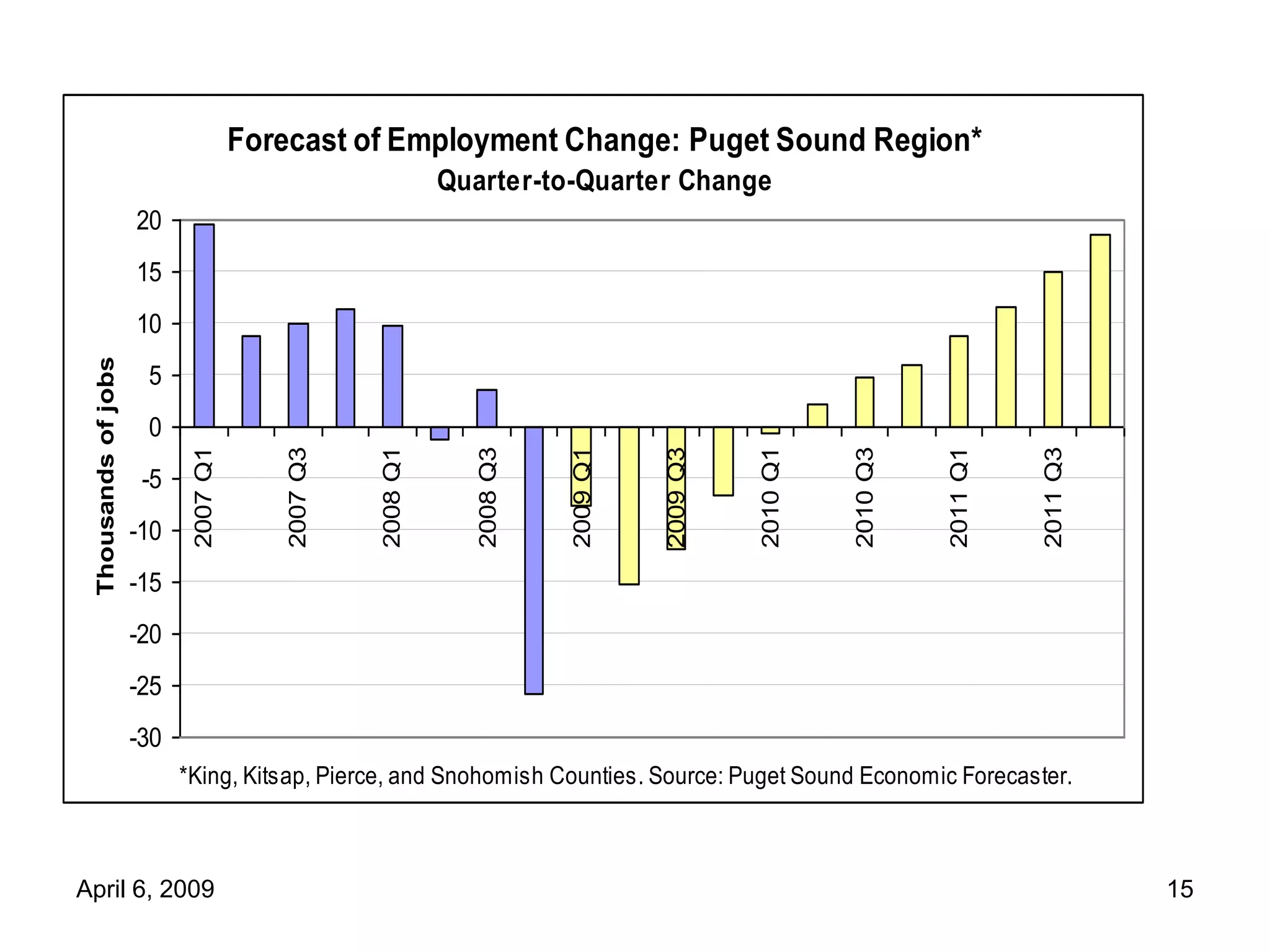

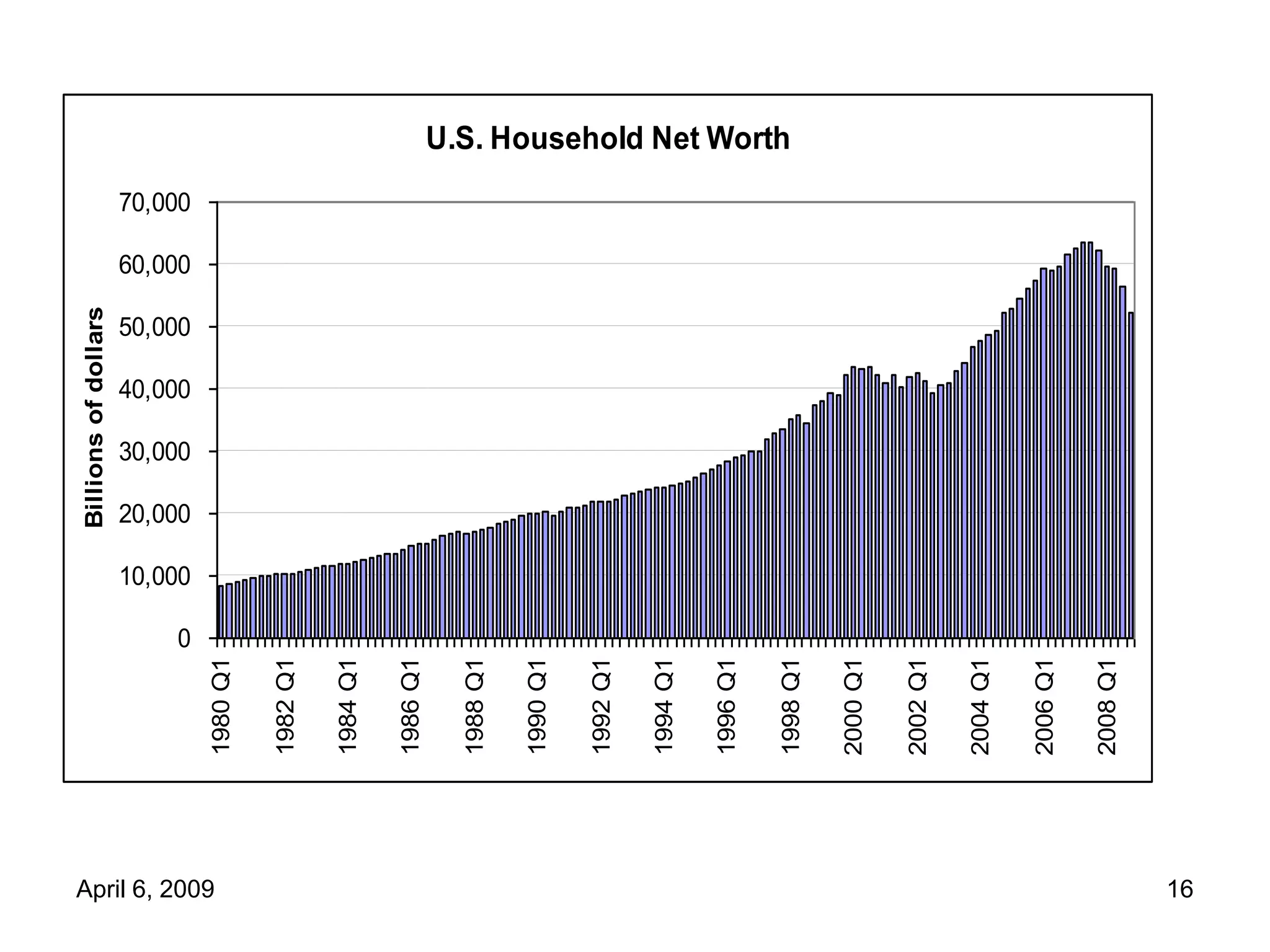

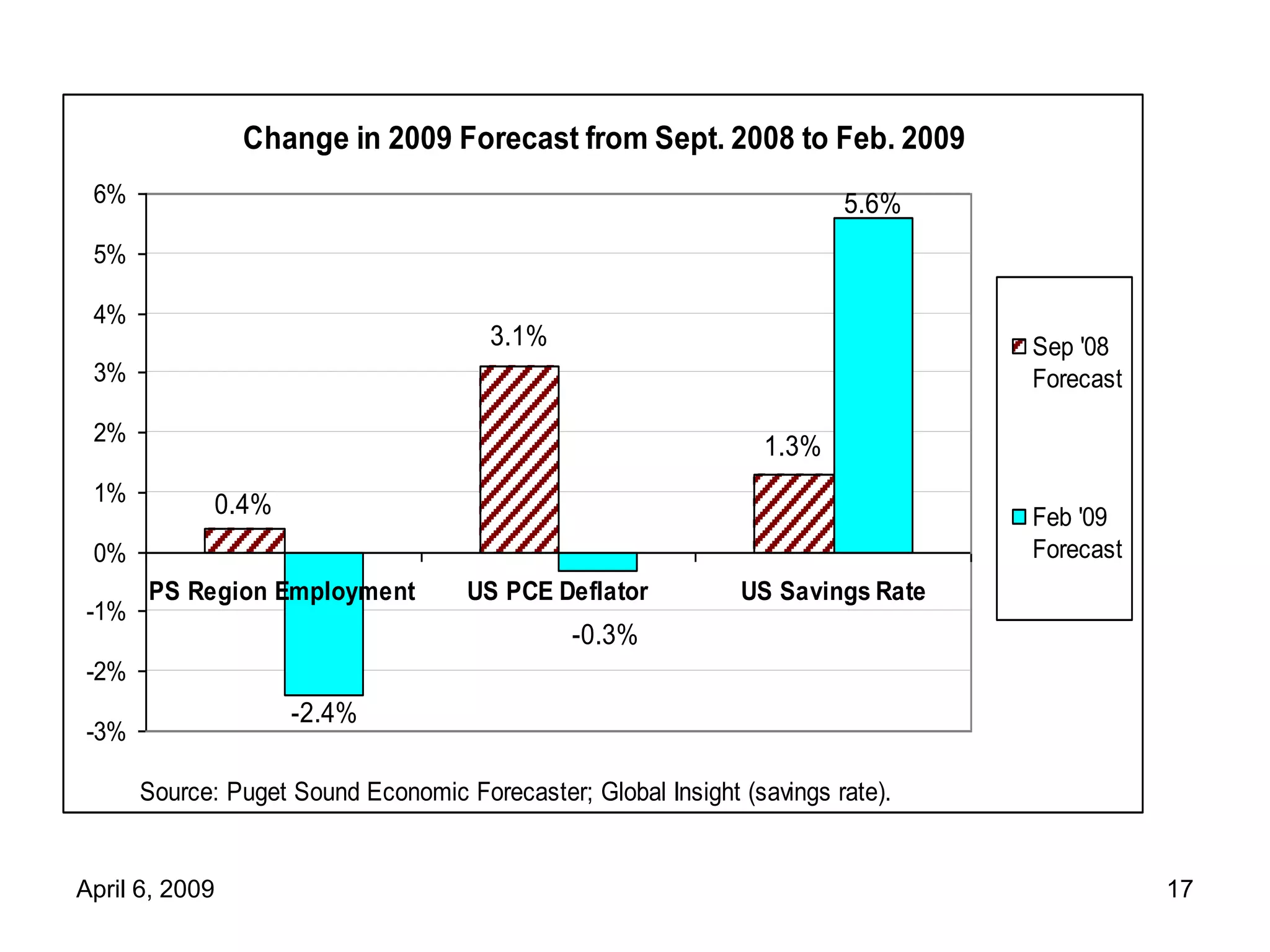

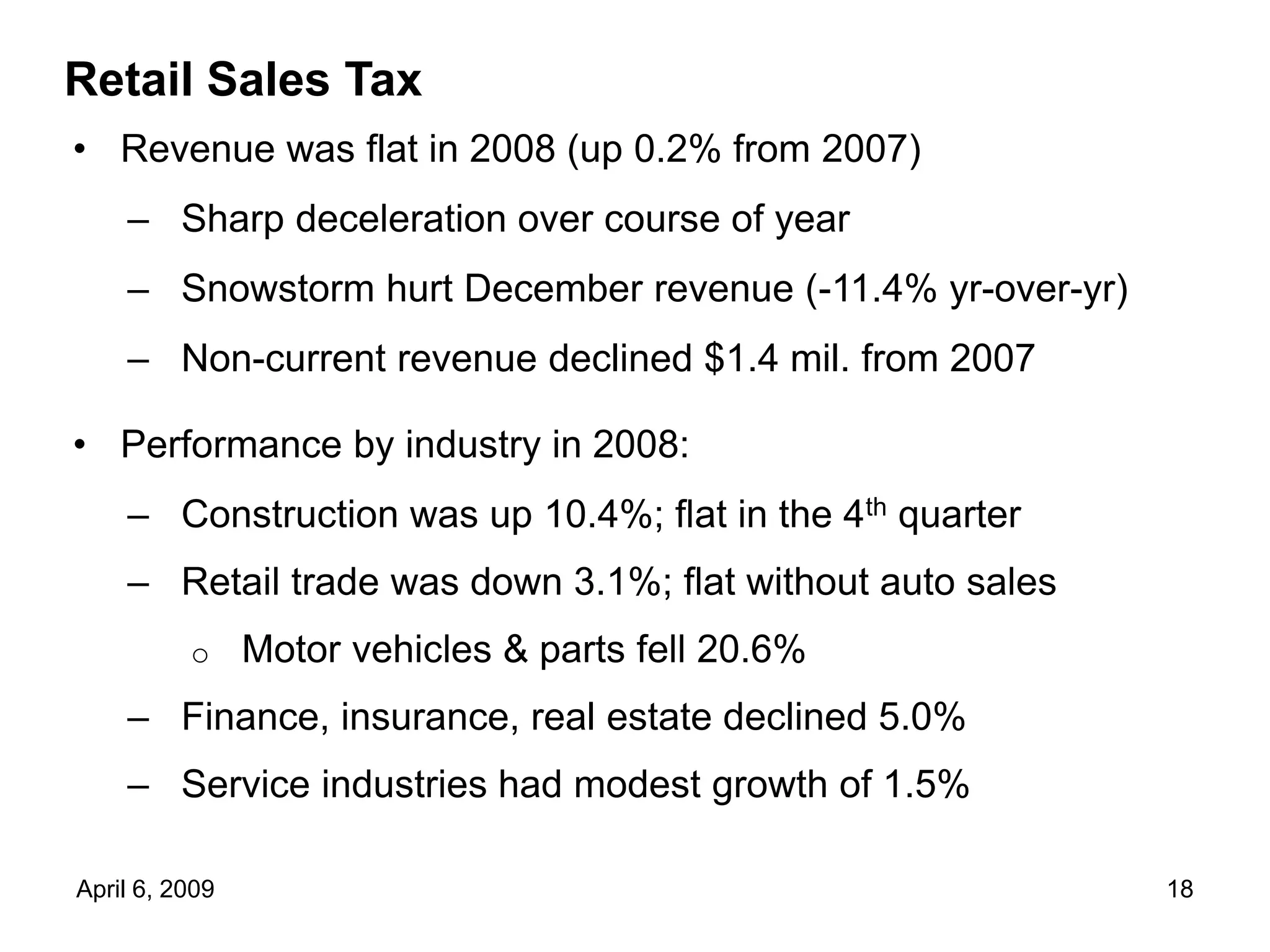

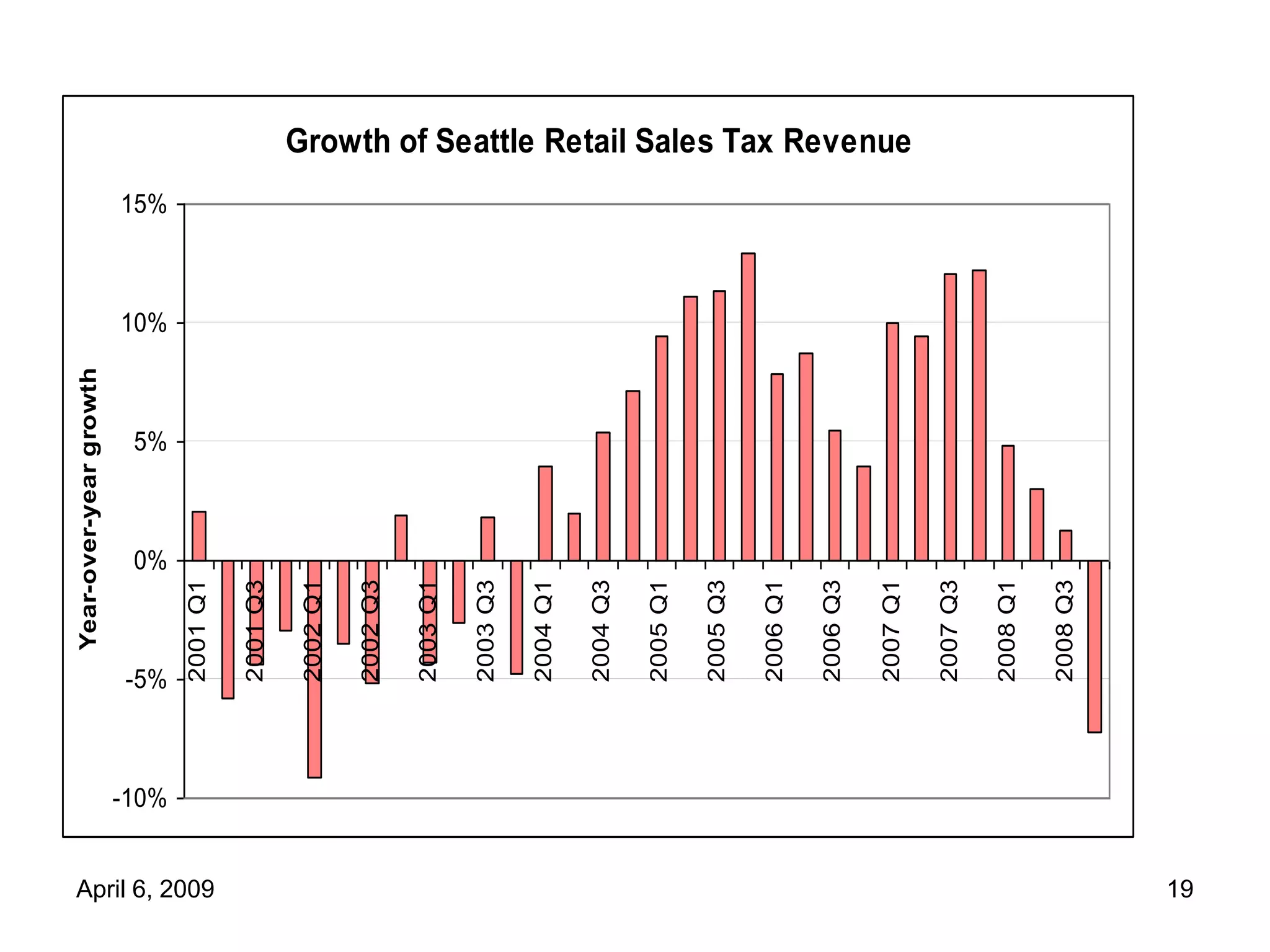

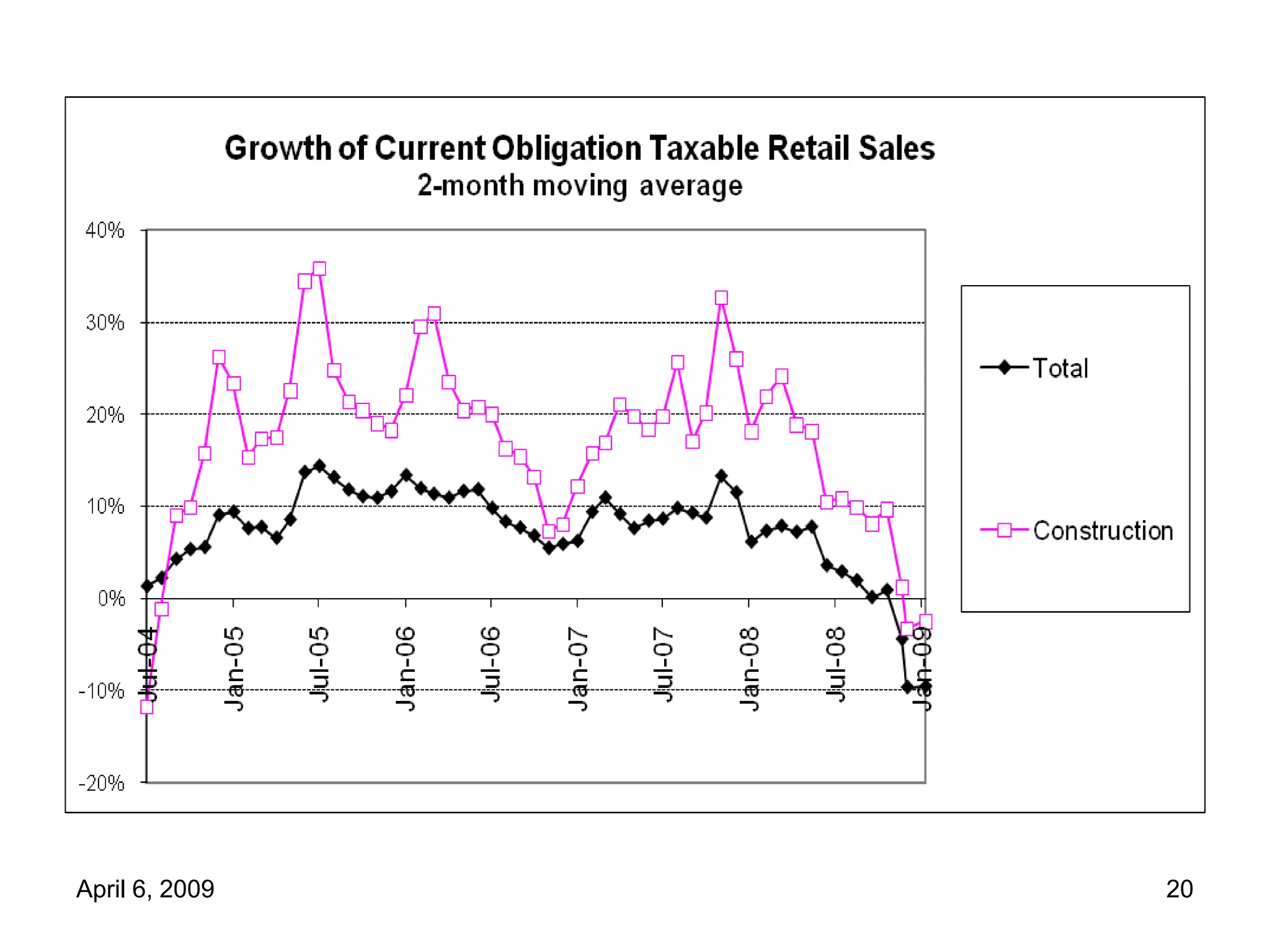

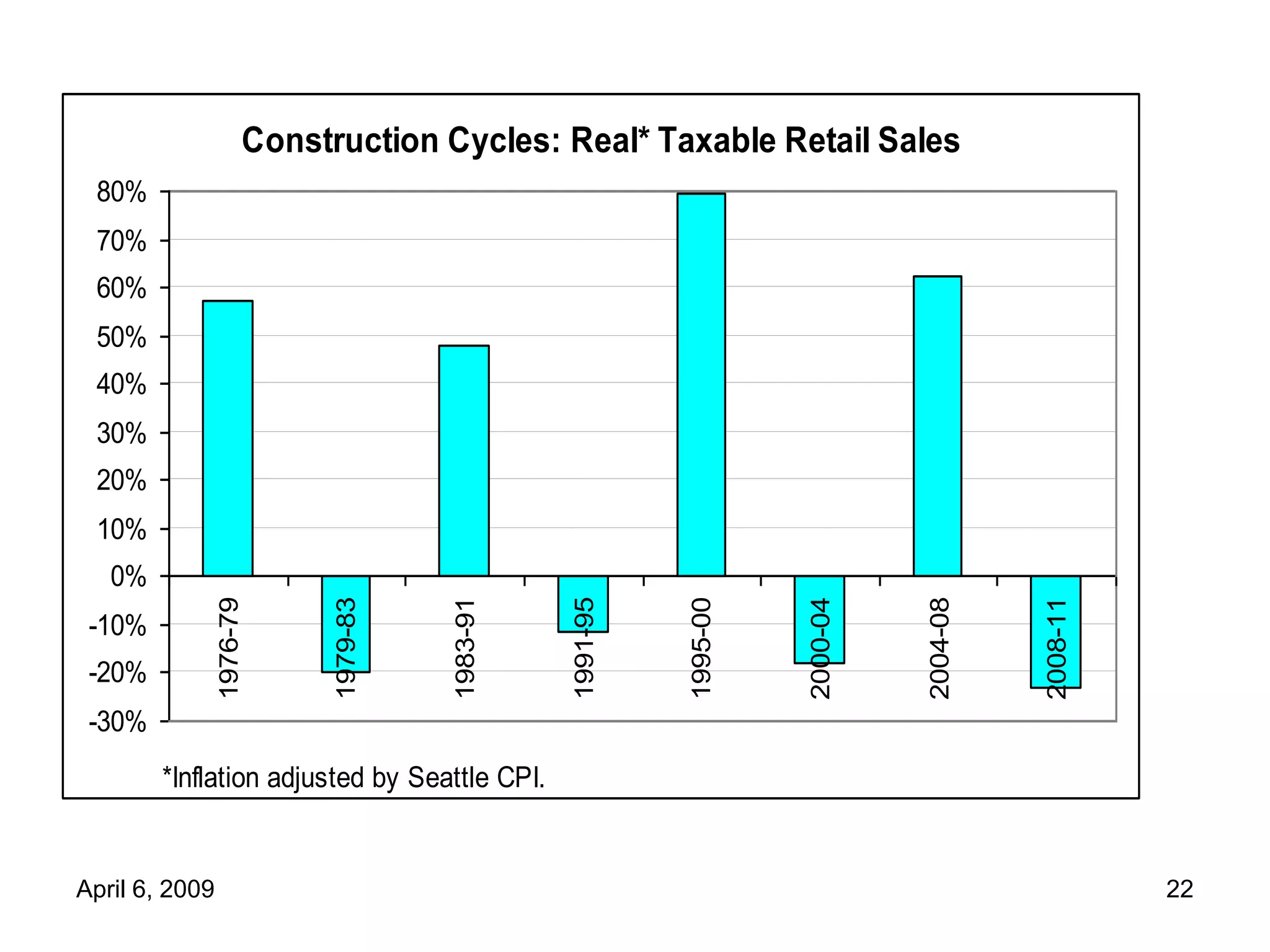

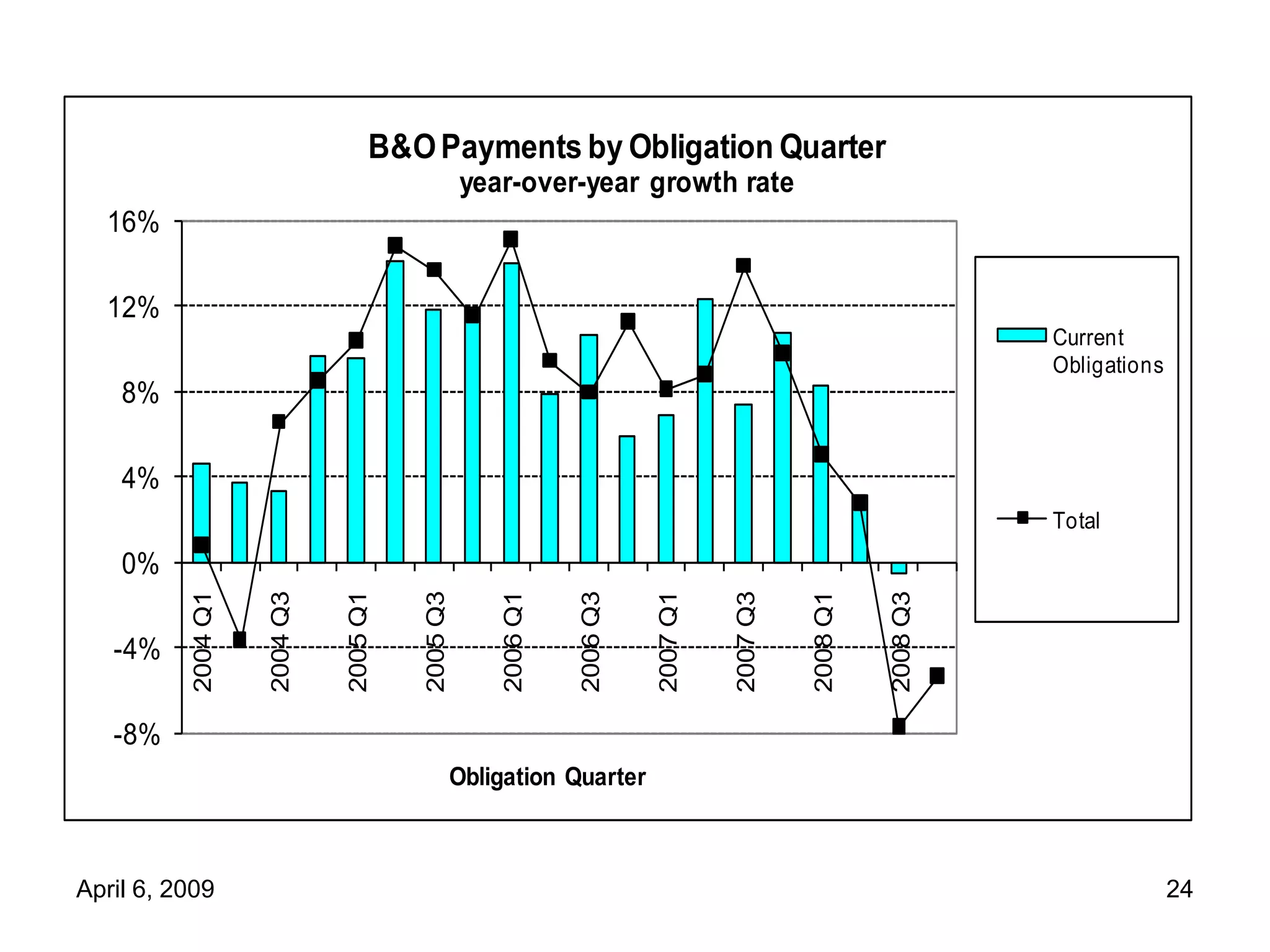

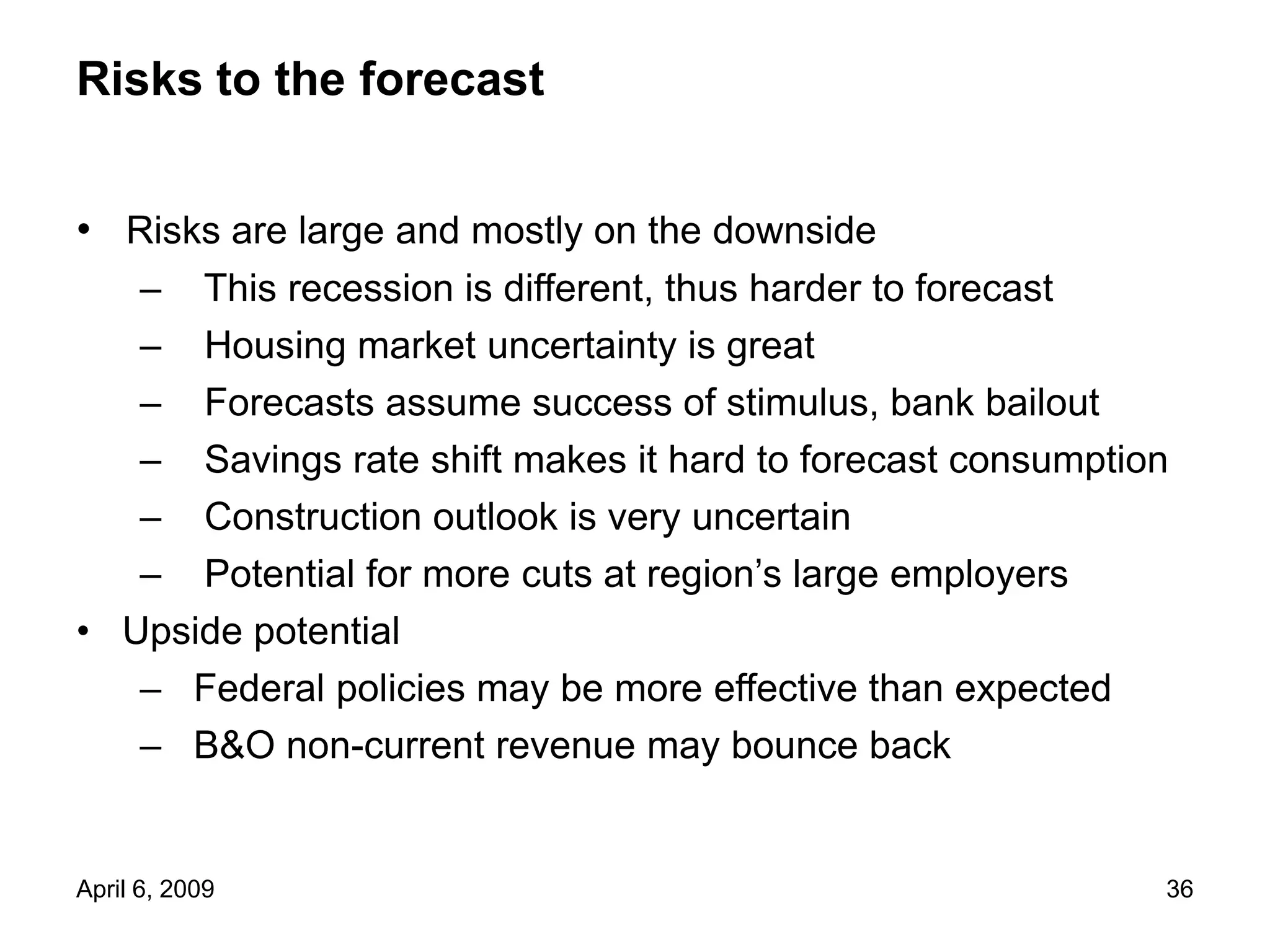

This document provides an economic forecast and analysis for the City of Seattle. It summarizes key factors that led to the current recession, including asset bubbles, cheap credit, loose lending standards, and the bursting of the housing bubble. It then analyzes recent economic indicators and forecasts a major regional recession for the Puget Sound area, with peak job losses of over 30,000. Revenue forecasts predict declines for sales tax, B&O tax, and natural gas utility tax due to weakness in construction, retail, and energy prices.