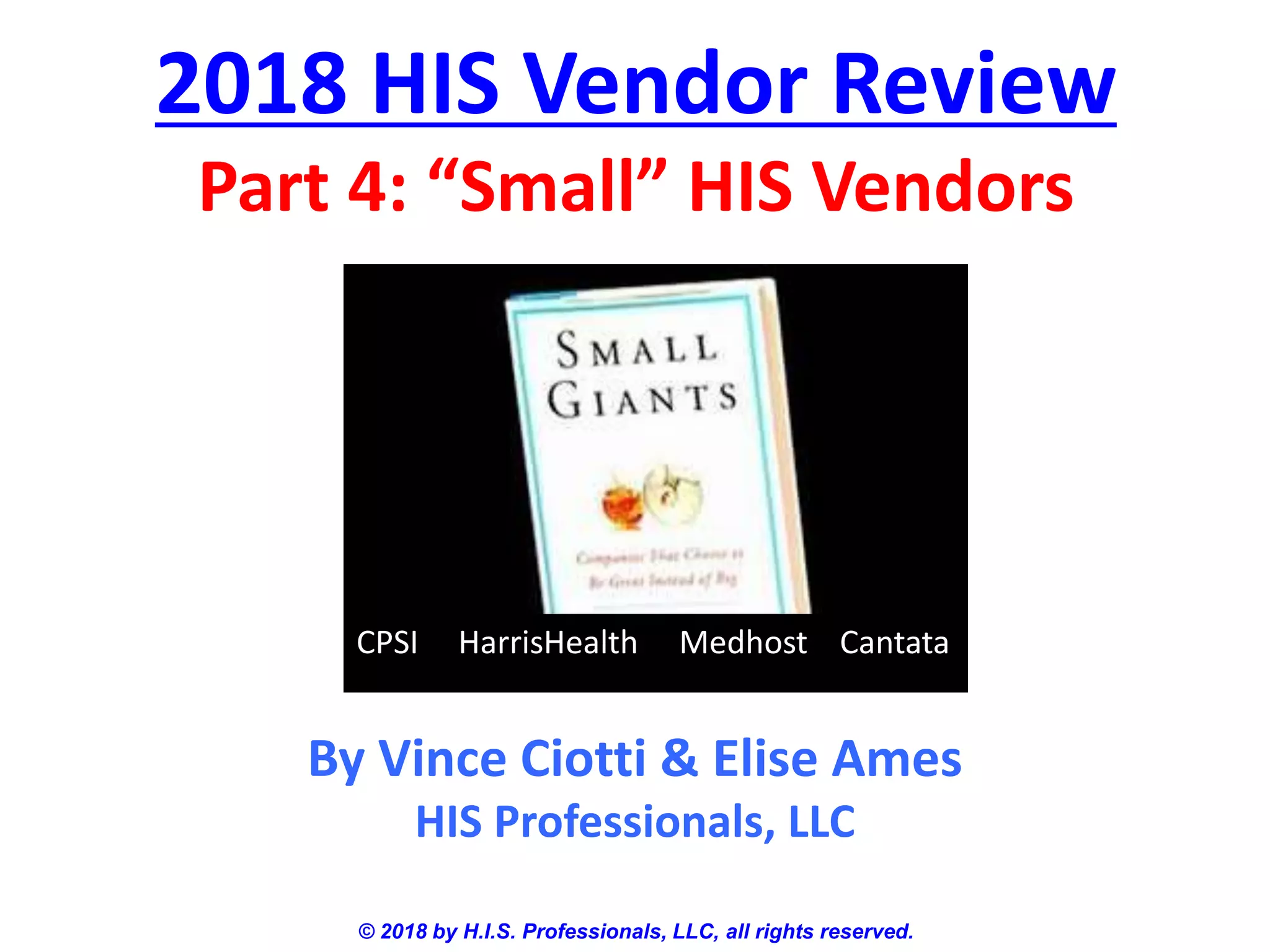

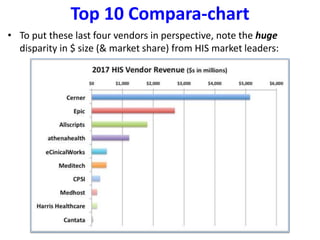

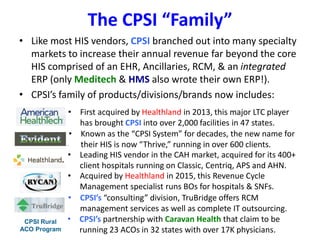

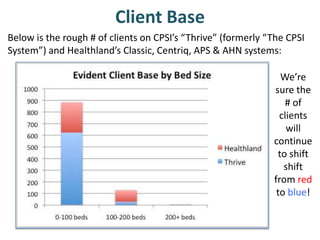

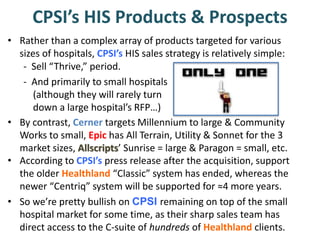

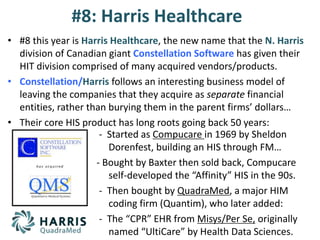

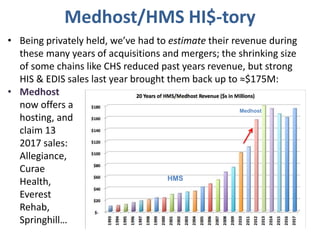

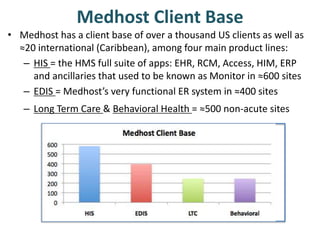

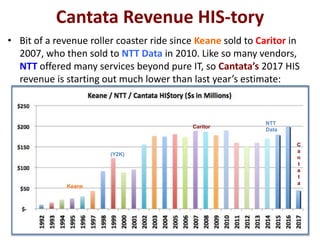

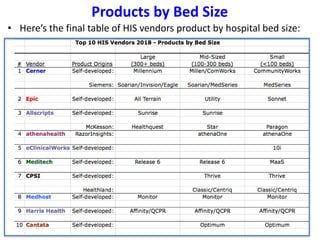

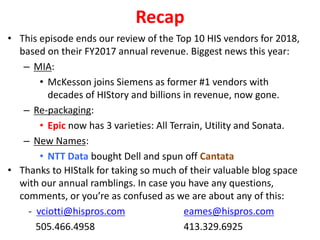

This document summarizes and analyzes the top 10 healthcare IT vendors based on 2017 annual revenue. It discusses the estimated $300M or less annual revenue of the last four vendors - CPSI, Harris Healthcare, Medhost, and Cantata. For each, it provides a brief history, product lines, client base, and future prospects. It concludes that the biggest news this year was McKesson and Siemens no longer being in the top 10, and Epic now having three product varieties for different hospital sizes.

![PERI-PROSTHETIC FRACTURE NAIL-PLATE CONSTRUCT [NPC].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/drarunkumardrmohamedashrafperiprostheticfrasturenail-plateconstructnpc-260209164459-7e9d15a1-thumbnail.jpg?width=640&height=640&fit=bounds)

![CTEV [ clubfoot] DR ARUN LAL ,DR MOHAMED ASHRAF travancore medical college k...](https://cdn.slidesharecdn.com/ss_thumbnails/ctevclubfootdrarunlaldrmohamedashraftravancoremedicalcollegekollamkeralaindia-260208063247-18fc466c-thumbnail.jpg?width=640&height=640&fit=bounds)