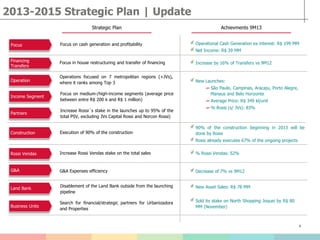

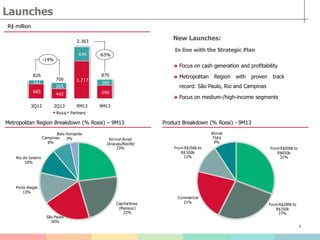

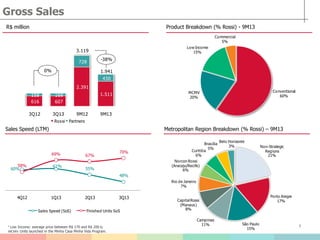

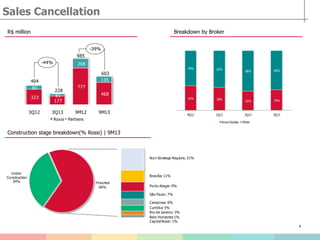

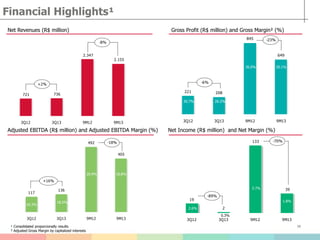

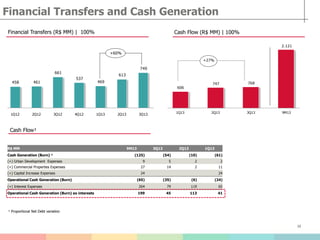

Rossi Residencial reported its 3Q13 and 9M13 operational and financial results. Operationally, new launches totaled R$665 million in 3Q13, in line with the company's strategic plan to focus on more profitable metropolitan regions. Gross sales were R$616 million in 3Q13. Financially, net revenue was R$492 million in 9M13, while adjusted EBITDA was R$405 million. The company generated R$199 million in operational cash flow excluding interest in 9M13.