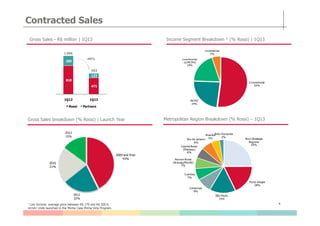

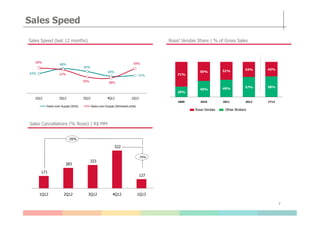

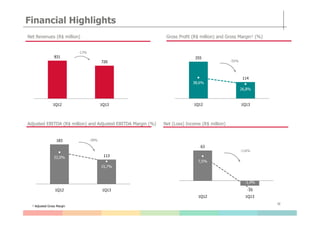

- Rossi reported operational and financial results for 1Q13 that showed improvements from the prior year, including a 46% increase in gross sales and a 55% decrease in net losses.

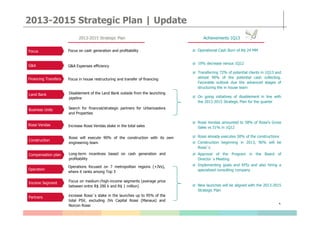

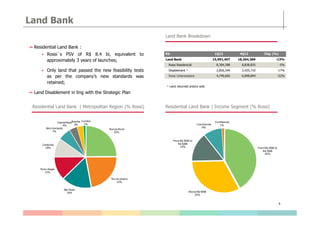

- The company continued progress on its 2013-2015 strategic plan, focusing on cash generation, profitability, and reducing exposure to non-core assets and regions.

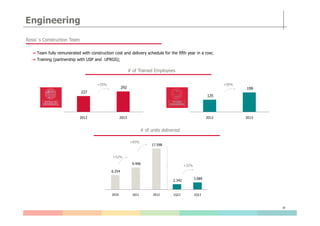

- Engineering initiatives increased the portion of construction executed by Rossi's in-house team to 50% in 1Q13, with a goal of 90% for 2013.