1. Page 1 of 6

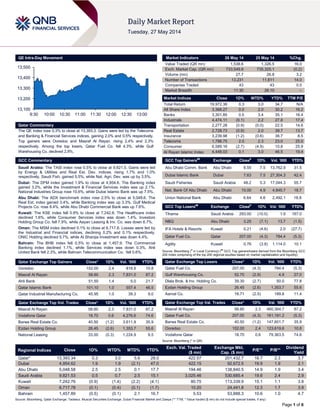

QE Intra-Day Movement

Qatar Commentary

The QE index rose 0.3% to close at 13,393.3. Gains were led by the Telecoms

and Banking & Financial Services indices, gaining 2.0% and 0.5% respectively.

Top gainers were Ooredoo and Masraf Al Rayan, rising 2.4% and 2.3%

respectively. Among the top losers, Qatar Fuel Co. fell 4.3%, while Gulf

Warehousing Co. declined 2.9%.

GCC Commentary

Saudi Arabia: The TASI index rose 0.5% to close at 9,821.5. Gains were led

by Energy & Utilities and Real Est. Dev. indices, rising 1.7% and 1.0%

respectively. Saudi Fish. gained 5.5%, while Nat. Agri. Dev. was up by 3.5%.

Dubai: The DFM index gained 1.9% to close at 4,954.6. The Banking index

gained 3.2%, while the Investment & Financial Services index was up 2.1%.

National Industries Group rose 10.6%, while Dubai Islamic Bank was up 7.5%.

Abu Dhabi: The ADX benchmark index rose 2.5% to close at 5,048.6. The

Real Est. index gained 3.4%, while Banking index was up 3.3%. Gulf Medical

Projects Co. rose 8.4%, while Abu Dhabi Commercial Bank was up 7.6%.

Kuwait: The KSE index fell 0.9% to close at 7,242.8. The Healthcare index

declined 1.6%, while Consumer Services index was down 1.4%. Investors

Holding Group Co. fell 7.9%, while Aayan Leasing & Inv. Co. was down 6.7%.

Oman: The MSM index declined 0.1% to close at 6,717.8. Losses were led by

the Industrial and Financial indices, declining 0.2% and 0.1% respectively.

ONIC Holding declined 5.7%, while Al Sharqia Investment was down 4.4%.

Bahrain: The BHB index fell 0.5% to close at 1,457.9. The Commercial

Banking index declined 1.1%, while Services index was down 0.3%. Ahli

United Bank fell 2.3%, while Bahrain Telecommunication Co. fell 0.6%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Ooredoo 152.00 2.4 818.9 10.8

Masraf Al Rayan 58.60 2.3 7,831.0 87.2

Ahli Bank 51.50 1.4 5.0 21.7

Qatar Islamic Bank 101.10 1.0 557.4 46.5

Qatar Industrial Manufacturing Co. 45.95 1.0 39.3 9.0

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Masraf Al Rayan 58.60 2.3 7,831.0 87.2

Vodafone Qatar 18.70 0.6 4,276.6 74.6

Barwa Real Estate Co. 40.50 (1.2) 3,611.9 35.9

Ezdan Holding Group 26.45 (2.6) 1,353.7 55.6

National Leasing 33.00 (0.3) 1,224.9 9.5

Market Indicators 26 May 14 25 May 14 %Chg.

Value Traded (QR mn) 1,538.6 1,326.5 16.0

Exch. Market Cap. (QR mn) 733,549.6 735,325.1 (0.2)

Volume (mn) 27.7 26.8 3.2

Number of Transactions 13,231 11,611 14.0

Companies Traded 43 43 0.0

Market Breadth 11:30 26:10 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,972.36 0.3 3.0 34.7 N/A

All Share Index 3,368.27 0.0 2.0 30.2 16.2

Banks 3,301.85 0.5 3.4 35.1 16.4

Industrials 4,474.11 (0.1) 2.2 27.8 17.4

Transportation 2,277.28 (0.9) (0.0) 22.5 14.6

Real Estate 2,728.73 (0.9) 2.0 39.7 13.7

Insurance 3,239.98 (1.2) (0.6) 38.7 8.5

Telecoms 1,788.75 2.0 2.3 23.0 25.0

Consumer 6,589.16 (2.7) (4.9) 10.8 25.9

Al Rayan Islamic Index 4,448.03 0.1 3.0 46.5 19.4

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Abu Dhabi Comm. Bank Abu Dhabi 8.55 7.5 13,762.9 31.5

Dubai Islamic Bank Dubai 7.63 7.5 27,304.3 42.4

Saudi Fisheries Saudi Arabia 48.2 5.3 17,044.3 55.7

Nat. Bank Of Abu Dhabi Abu Dhabi 15.00 4.9 4,845.7 18.7

Union National Bank Abu Dhabi 6.64 4.6 2,492.1 18.8

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Tihama Saudi Arabia 293.00 (10.0) 1.9 167.0

NBQ Abu Dhabi 3.25 (7.1) 13.7 (1.5)

IFA Hotels & Resorts Kuwait 0.21 (4.6) 2.0 (27.7)

Qatar Fuel Co. Qatar 207.00 (4.3) 784.4 (5.3)

Agility Kuwait 0.76 (3.8) 1,114.0 10.1

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar Fuel Co. 207.00 (4.3) 784.4 (5.3)

Gulf Warehousing Co. 52.70 (2.9) 4.9 27.0

Dlala Brok. & Inv. Holding Co. 39.30 (2.7) 50.0 77.8

Ezdan Holding Group 26.45 (2.6) 1,353.7 55.6

Aamal Co. 16.71 (2.5) 189.8 11.4

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Masraf Al Rayan 58.60 2.3 460,364.7 87.2

Qatar Fuel Co. 207.00 (4.3) 161,181.2 (5.3)

Barwa Real Estate Co. 40.50 (1.2) 147,601.7 35.9

Ooredoo 152.00 2.4 123,619.6 10.8

Vodafone Qatar 18.70 0.6 79,363.5 74.6

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 13,393.34 0.3 3.0 5.6 29.0 422.57 201,432.7 16.7 2.3 3.7

Dubai 4,954.62 1.9 1.9 (2.1) 47.0 422.15 92,672.5 19.9 1.9 2.1

Abu Dhabi 5,048.58 2.5 2.5 0.1 17.7 194.46 138,840.5 14.9 1.9 3.4

Saudi Arabia 9,821.53 0.5 0.7 2.5 15.1 3,025.46 530,685.4 19.6 2.4 2.9

Kuwait 7,242.76 (0.9) (1.4) (2.2) (4.1) 80.75 113,339.9 15.1 1.1 3.8

Oman 6,717.78 (0.1) (0.4) (0.1) (1.7) 10.20 24,441.8 12.3 1.7 3.9

Bahrain 1,457.89 (0.5) (0.1) 2.1 16.7 5.53 53,888.3 10.6 1.0 4.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

13,100

13,200

13,300

13,400

13,500

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QE index rose 0.3% to close at 13,393.3. The Telecoms and

Banking & Financial Services indices led the gains. The index

rose on the back of buying support from non-Qatari shareholders

despite selling pressure from Qatari shareholders.

Ooredoo and Masraf Al Rayan were the top gainers, rising 2.4%

and 2.3% respectively. Among the top losers, Qatar Fuel Co. fell

4.3%, while Gulf Warehousing Co. declined 2.9%.

Volume of shares traded on Monday rose by 3.2% to 27.7mn

from 26.8mn on Sunday.However, as compared to the 30-day

moving average of 28.6mn, volume for the day was 3.1% lower.

Masraf Al Rayan and Vodafone Qatar were the most active

stocks, contributing 28.3% and 15.4% to the total volume

respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn)1Q2014

% Change

YoY

Operating Profit

(mn) 1Q2014

% Change

YoY

Net Profit (mn)

1Q2014

% Change

YoY

Etihad Atheeb

Telecommunication Co.*

Saudi SR – – -250.5 – -249.3 NA

Tihama Advertising & Public

Relations Co.*

Saudi SR – – -44.8 – -52.5 NA

Saudia Dairy & Foodstuff

Co. (SADAFCO)*

Saudi SR – – 184.0 4.8% 171.5 4.1%

Al Dar National Real Estate

Co. (ADNEC)

Kuwait KD – – – – -0.9 NA

Source: Company data, DFM, ADX, MSM. (* FY2013-14)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

05/26 Germany GfK AG GfK Consumer Confidence June 8.5 8.5 8.5

05/26 Spain INE PPI MoM April 0.20% – 0.20%

05/26 Spain INE PPI YoY April 0.10% – -1.30%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Qatar allows raising foreign ownership in listed companies

to maximum of 49%, subject to amendment in company

statues – HH the Emir Sheikh Tamim bin Hamad al-Thani, who

is also President of the Supreme Council For Economic Affairs

and Investment (SCEAI), has given instructions to raise the

percentage of non-Qatari ownership in companies listed in the

Qatar Stock Exchange (QSE). HE Minister of Finance Ali Sherif

al-Emadi, who is also the SCEAI’s Secretary General, said that

the increase in the proportion of non-Qatari ownership in

companies listed on the QSE will be in accordance with the

effective legal procedures as follows: 1) The equality of the GCC

citizens with their Qatari counterparts as regards their

possession of shares of companies listed in QSE, 2) The Non-

Qatari citizens who are not members of the GCC may possess

shares of the companies listed on QSE and by a percentage not

exceeding 49%, and this will be up to the desire of each

company through amending its statute, 3) The proportion of non-

Qatari ownership, which was referred to in the previous item, in

shares of companies traded in the Qatar Exchange, shall be

calculated based on the total capital of each company and not

on its non-tradable shares and 4) The Ministry of Economy and

Commerce and Qatar Financial Markets Authority (QFMA) will

immediately take the measures to put this directive into effect.

(Gulf-Times.com)

QE hosts international investment sell-side companies in

London – The Qatar Exchange (QE) hosted a dinner event in

London for senior representatives of sell-side brokers and

institutions, ahead of the MSCI Emerging Markets inclusion for

Qatari companies. The purpose of the event was to meet with

key traders and sales executives who are responsible for the

international order flow into the Qatari market. This event

complimented the previous roadshow event where QE met with

key decision makers from a number of leading international buy-

side institutions. (QE)

Growth in Qatar’s telecom sector set to continue – HE the

Minister of Information & Communications Technology (ICT) Dr.

Hessa al-Jaber said Qatar’s telecommunications sector surged

11% in 2013 and is expected to continue growing at 9-12% over

the next five years. The minister reiterated the ICT’s important

role in realizing the Qatar National Vision 2030. Meanwhile, HE

the Minister of Finance Ali Sharif al-Emadi noted that 40% of

Qatar’s total budget for FY2014-15 was allocated for the

ongoing major projects in various parts of the country. He also

noted that the government had invested QR2.5bn for Qatar’s

satellite company Es’hailSat, a move that will further boost the

country’s ICT capability. He said that the GDP contribution from

this sector has increased to QR7.5bn in 2013 from QR5.5bn in

2010. (Gulf-Times.com)

Qatar, GCC trade balance worth QR43.3bn in 2013 – HE the

Minister of Economy & Commerce Sheikh Ahmed bin Jassim bin

Mohammed al-Thani said that trade balance between Qatar and

fellow GCC members was worth QR43.3bn in 2013. Sheikh

Ahmed said Qatar’s total exports stood at QR30bn, while

Overall Activity Buy %* Sell %* Net (QR)

Qatari 53.46% 65.76% (189,191,058.60)

Non-Qatari 46.54% 34.25% 189,191,058.60

3. Page 3 of 6

imports were at QR13.3bn. Speaking on the sidelines of the

15th GCC Joint Exhibition at the Sharjah Expo Centre, the

minister said that the exhibition was an opportunity to advance

economic integration and the convening of representatives of

the GCC private sector will boost joint investments and trade.

He added that the exhibition comes at the special occasion of 33

years of establishing the GCC and noted that such events will

have a positive impact on trade between GCC countries. (Gulf-

Times.com)

GWCS completes implementation of new warehouse

management system – Gulf Warehousing Company (GWCS)

has completed the implementation of INFOR WMS, an

enterprise warehouse management system geared at

automating its inventory base of over 450 customers under third

party and fourth party logistics services. (Gulf-Times.com)

QTA: Continued growth in tourism sector in 1Q2014 – The

Qatar Tourism Authority (QTA) 1Q2014 report has released data

capturing business and tourist visas that revealed continued

growth in Qatar’s expanding tourism industry. All key indicators

of the tourism sector demonstrated improvement over the

previous year’s comparable period. Regional and international

visitor arrivals totaled 387,022, representing a 9% YoY increase.

(Gulf-Times.com)

QBIC lists 15 projects for incubation and support – The

Qatar Business Incubation Center (QBIC) announced that 15

projects have been chosen to be incubated and receive its

support. QBIC will provide the winning entrepreneurs with a

range of support services such as office space and industrial

workshops, as well as administrative, technical and financial

assistance. (Peninsula Qatar)

Q-Coat becomes leading producer of ECR steel – Qatar

Metals Coating Company (Q-Coat), the sole supplier of anti-

corrosion epoxy coated rebar (ECR) in Qatar, has emerged as

one of the largest producers of the fusion bonded ECR steel in

the GCC region with an installed capacity of producing up to

100,000 tons per annum. Q-Coat, located in Mesaieed Industrial

City is a JV between Qatar Steel Company and Qatar Industrial

Manufacturing Company. (Peninsula Qatar)

QA to move all flights to HIA – Qatar Airways (QA) has

announced to move all its flights to the new Hamad International

Airport (HIA) on May 27, 2014 (today). The new airport will have

the capacity to handle 8,700 customers per hour, and will

feature 138 check-in counters, including 108 counters for QA’s

Economy class passengers and all other airlines. Around 16

counters will be dedicated to QA’s business class travelers and

14 check-in counters for QA’s first class passengers.

(Bloomberg)

International

Draghi says timing key as ECB watches for negative spiral

– The European Central Bank’s (ECB) President Mario Draghi

signaled that ECB policy makers are ready to take action in

June 2014, if they see low inflation becoming entrenched.

Draghi indicated that the ECB is focusing on liquidity measures

that can be deployed to help free up lending to companies and

households. These measures include interest-rate cuts and

liquidity injections, while there is the prospect of asset

purchases. The Frankfurt-based central bank is reviewing

lenders’ balance sheets to purge the system of unrecognized

losses before it takes over as supervisor in November. That

threatens to curb credit supply to the economy, slowing growth

and prices. The ECB president also said that a prolonged period

of low inflation can lead to higher debt burdens and prompt

lenders to tighten their credit standards. Inflation in the 18-nation

euro area has been below 1% since October, less than half the

ECB’s goal. (Bloomberg)

CBI: UK services companies’ confidence rose – According to

the Confederation of British Industry (CBI), confidence among

UK services companies rose to a record this quarter, indicating

continued expansion in the largest part of the economy. An

index of optimism among consumer businesses such as

restaurants and hotels jumped to 53 from 43, the highest since

the survey began in 1998. Sentiment among professional

services firms – such as accountants and legal companies –

rose to 54, also a record. The survey shows strength in an

industry that accounts for about 75% of the economy after

households were the driving force behind economic growth in

2013 and in the first quarter. GDP increased 0.8% in the three

months through March, with consumer spending adding 0.5%

point. (Bloomberg)

NDRC: China cuts bureaucracy for investment – The

National Development & Reform Commission (NDRC) has said

that China has simplified procedures for its government to

approve investment projects in order to increase transparency

and efficiency, marking its latest effort to streamline

administration and devolve more power to firms. According to

new rules, the government will only vet certain aspects of

projects that are considered strategic, such as those pertaining

to environmental protection, economic security and monopolies.

Companies will be given more autonomy in deciding matters

such as investment returns and financing, without providing

more details. Cutting government red tape is part of China's

wide-ranging plans to reform its economy into one that is more

driven by market forces. (Reuters)

BoR: Russia to grow by 0.5% in 2014 – The Russian central

bank’s governor Elvira Nabiullina has said that the country’s

economy is likely to grow by around 0.5% this year, but the

overall threat to stability from the crisis in Ukraine would not be

large scale. Nabiullina said in an interview that the Bank of

Russia (BoR) will probably revise its 2014 GDP growth forecast

to around 0.5%, as compared to its earlier forecast of 0.9%.

Earlier in February, the BoR had predicted the economy would

grow by 1.5-1.8% in 2014. The central bank's earlier GDP

growth forecast of 0.9% had not been made public, which

indicates that two downward revisions have been made since

Russia engaged in Ukraine and annexed Crimea. The Russian

economy is on the brink of recession after its GDP fell by 0.5%

in the first quarter, impacted by sanctions and instability

resulting from the stand-off with Ukraine. (Reuters)

Japan risks low growth even as easing spurs inflation –

Japan’s risk of spurring inflation without boosting the nation’s

growth potential is raising the stakes for the Prime Minister

Shinzo Abe’s next round of economic restructuring measures,

due in June. The Bank of Japan (BoJ) Deputy Governor Kikuo

Iwata stated that an economy with low real growth rates under

mild inflation is possible, if the government fails to deliver. The

BoJ’s stimulus helped lift core inflation (excluding fresh food), to

1.3% in March from -0.4% in April 2013 when the central bank

started easing a campaign of monetary easing. Investors are

seeking lower corporate taxes, labor-market flexibility and

progress on a US-led trade pact as Shinzo Abe prepares for the

next phase of the so-called ‘Third Arrow of Abenomics’ –

economic restructuring to boost long-term growth prospects.

(Bloomberg)

Regional

New Saudi-Bahrain oil pipeline to be ready by 3Q2016 –

Saudi Aramco said that the tenders for the engineering,

procurement & construction (EPC) contract for a new crude oil

4. Page 4 of 6

pipeline between Saudi Arabia and Bahrain are expected to be

issued by the end of 2014. The pipeline is expected to be

commissioned by 3Q2016 at an estimated cost of $350mn. The

115km-long pipeline would run overland for 74km, with the

remaining 31km being sub-sea. It will transport crude from

Aramco’s Abqaiq plant to Bahrain. With a capacity of 350,000

bpd, the new link will replace an ageing 230,000 bpd pipeline. Its

completion is a key pre-requisite for Bahrain Petroleum

Company’s planned Sitra refinery expansion to up to 500,000

bpd total capacity, which is estimated to cost around $6bn.

(GulfBase.com)

QA, Burgan Bank launch co-branded credit card – Qatar

Airways (QA) and Kuwait-based Burgan Bank (BB) have

launched new co-branded MasterCard credit card. The new

MasterCard with its platinum and gold variants will be offered on

the MasterCard network platform, allowing customers access to

combined benefits offered by BB, QA and MasterCard. This

initiative will allow customers to convert their everyday banking

transactions, into flight rewards, while enjoying an array of

exclusive privileges and world class services. (GulfBase.com)

STC hires managers for debut Sukuk issuance – The Saudi

Telecom Company (STC) has hired Standard Chartered,

JPMorgan Chase and NCB Capital to market its debut Sukuk

issuance program. The banks will manage the potential sale

under a SR5bn Sukuk program. The size of the private local

placement will depend on market conditions. (GulfBase.com)

PDC, BSF sign SR528mn murabaha bridge funding – Ports

Development Company (PDC) and Banque Saudi Fransi (BSF)

have signed an agreement governing an SR528mn Murabaha

bridge financing for the expansion of King Abdullah Port. It is the

first privately developed and operated port in the Kingdom.

(GulfBase.com)

RCJY signs 2 deals worth SR467.9mn for Jubail, Ras Al-

Khair projects – The Royal Commission for Jubail and Yanbu

(RCJY) has signed two contracts worth SR467.9mn. Under the

first contract, the Saudi Services for Electro-Mechanic Works

Company (SSEM) will establish a pumping station for drinking

water and four water tanks in the industrial city of Ras Al-Khair.

The project will take two years and two months to complete. The

second contract has been signed with SSEM to develop the

King Fahd Industrial Port’s power plant in Jubail industrial city

and undertake design & supply for lifting power lines. The work

on this project will take three and a half years. (GulfBase.com)

Shaker Co. completes 2% stake sale in LG Shaker – Al

Hassan Ghazi Ibrahim Shaker Company (Shaker Co.)

announced that the company has sold 2% of its shares in LG

Shaker to LG Electronics for a value of SR3.8mn. The official

formalities regarding the transaction have been completed to

reflect the company’s new ownership structure. With this, LG’s

shareholding in LG Shaker Company has reached 51%, while

Shaker Co. holds 49%. (Tadawul)

Saudi CMA approves Shuaa’s capital decrease – Saudi

CMA’s board has approved the Shuaa Capital’s (Shuaa) request

to decrease its capital from SR150mn to SR75mn. (Tadawul)

SABIC signs $595mn JV deal with SK – Saudi Basic

Industries Corporation’s (SABIC) fully owned company, SABIC

Industrial Investment Company, and the Korean petrochemical

company, SK Global Chemical (SK), have signed a 50-50 joint

venture (JV) agreement for a total investment of $595mn. The

JV involves SABIC owning SK’s cutting edge Nexlene

technology and a plant that has been recently completed at SK’s

complex in Ulsan, South Korea, with an expected annual

capacity of 230,000 tons. Located in Singapore, the JV will

manufacture a range of high-performance polyethylene

products. (Tadawul)

Maaden appoints advisor for rights issue – The Saudi

Arabian Mining Company (Maaden) has assigned HSBC Saudi

Arabia as the financial advisor to manage its proposed rights

issue. (Tadawul)

Tamlik, Green Falcon sign affordable housing deal – Tamlik

and Green Falcon have concluded a memorandum of

participation in collating efforts to embark on affordable housing

development in the Kingdom. The agreement aims to contribute

to the Ministry of Housing’s efforts to achieve the delivery of

500,000 affordable housing units. Green Falcon is an exclusive

licensed company to build affordable houses outside France by

Geoxia. (GulfBase.com)

SBG’s CPC acquires Sphinx Glass for $190mn –

Construction Products Holding Company (CPC) – a part of

Saudi Binladin Group (SBG) – has acquired Egypt-based glass

manufacturer Sphinx Glass for $190mn. CPC acquired 73.3%

stake from Citadel Capital for $112mn, while remaining stake

has been bought from other investors. (Reuters)

F&S: UAE logistics market to expand by 15.4% in 2015 –

According to Frost & Sullivan (F&S), the UAE logistics market is

estimated to have reached $23.4bn in 2013, representing

around 6% of the country’s GDP. It is expected to grow 15.4% in

2015 to reach $27bn. A surge in import and export trade

volumes is expected in 2015. Further, a steady upward trend of

local manufacturing is expected. (GulfBase.com)

S&P: UAE real estate to remain healthy – According to

Standard & Poor’s (S&P), real estate prices in the UAE are

predicted to be steady after strong growth over the past two

years, particularly in Dubai. Low interest rates are attracting

strong external demand for Dubai real estate from regional and

international investors. S&P has used land sales as a proxy for

total demand and has forecast the UAE’s GDP to grow at 3.8%

in 2014 and 2015. Total value of land and housing real estate

transactions in 2013 reached AED236bn compared with

AED154bn in 2012. This demand was almost evenly split

between local (AED122bn) and external demand (AED114bn).

(GulfBase.com)

Emaar to sell 25% of Malls Group in IPO – Emaar Properties

announced its intention to sell up to 25% of its equity in Emaar

Malls Group and list the unit on the Dubai Financial Market

(DFM). Emaar has received the required approval from the

Securities & Commodities Authority. The funds raised from the

proposed IPO will be primarily distributed as dividend to the

company’s shareholders. The timing of the public offering and

listing will be announced at a later date. (GulfBase.com)

Agility declares 40% cash dividend, 5% bonus shares –

Agility Public Warehousing Company’s AGM has approved the

distribution of 40% cash dividend (40 fils per share) and 5%

bonus shares for the year ended December 31, 2013. (DFM)

DI, Sanofi to promote new generics portfolio – Dubai

Investments (DI) has entered into an agreement with French

pharmaceutical company, Sanofi for promoting a new generic

drugs portfolio in the Middle East through DI’s subsidiary,

Globalpharma. Products will be commercialized under a joint

entity to meet the needs of patients within the UAE and the

wider region. (DFM)

Imdaad signs waste management deal with EZW – Imdaad

has signed a long-term agreement with Economic Zones World

(EZW) for waste management. Under the agreement, an

AED100mn technologically advanced material recovery facility

5. Page 5 of 6

will be set up at TechnoPark in Jebel Ali to recover the

recyclables from solid waste collected by Imdaad. The facility

will have an initial operating capacity of 1,000 tons/day, with a

possibility to double the operation in the future. It will also cater

to waste collected by other companies. Imdaad is a provider of

integrated facilities management solutions in GCC, while EZW is

a developer of economic zones, technology, logistics and

industrial parks under the Dubai Property Group. (Bloomberg)

Brndstr raises $1.6mn in funding – Dubai-based startup,

Brndstr has raised $1.6mn in new funding to help launch its

software that better connects social media users and the brands

they follow. The company is currently in a pilot phase with

private-chauffeur company Uber and is also in talks with other

brands and media buying companies in Dubai. (Bloomberg)

Dubai Customs, Tanmia signs cooperation deal – Dubai

Customs and the National HR Development & Employment

Authority (Tanmia) have entered into a joint cooperation

agreement on forging strategic partnerships at various levels

especially in providing work opportunities for Emirati nationals.

The agreement includes exchange of information and expertise,

and the utilization of each entity's resources towards increasing

the capacity and efficiency of the human capital at both sides.

(Bloomberg)

Etisalat gets $500mn grant from Abu Dhabi for Maroc

Telecom deal – Abu Dhabi has given a $500mn grant for

Etisalat’s €4.14bn purchase of 53% of Maroc Telecom. The

grant provides further evidence of the Emirate’s support for the

foreign expansion of its companies and could attract complaints

from rival operators. Another Abu Dhabi-based Company Etihad

Airways benefited from a $3bn interest-free loan from the

emirate’s ruling family, leading to complaints from rival airlines

about state subsidies distorting competition. The grant was

mentioned in Etisalat’s prospectus for a bond issue to help

repay some of the debt taken on to complete the Maroc

Telecom transaction. According to sources, Etisalat could start

marketing the bond as early as next week, having chosen four

banks to arrange the issue. (Gulf-Times.com)

NCSI, MoH, ORA to launch real estate price index – The

National Centre for Statistics & Information (NCSI), in

coordination with the Ministry of Housing (MoH) and Oman Real

Estate Association (ORA), is planning to introduce a

comprehensive real estate price index. This plan is against an

earlier proposal for a simple index. The index will be launched in

few months. (GulfBase.com)

Oman plans to launch strategy for real estate sector – The

Omani government is planning to introduce a national strategy

for the real estate sector, which is aimed at bringing world

standards in construction practices as well as better

coordination between basic infrastructure planning and property

development. Oman’s real estate sector has grown from

OMR292mn in 1998 to OMR610mn in 2012, indicating an

average annual growth of 4.5%. Meanwhile, FDI in the real

estate sector has grown from OMR190mn in 2006 to

OMR414mn in 2012, an average annual growth of 14%.

(GulfBase.com)

AIB appoints CEO – Alizz Islamic Bank (AIB) has appointed

Salaam Said Al Shaksy as the CEO. Salaam has five years of

banking experience, and has held the position of General

Manager and CEO in several reputed local and international

banks. (MSM)

T-Linx Technology signs deal with LZ Group – Bahrain-

based T-Linx Technology Solutions Architects has signed a

cooperation agreement with a Dutch IT firm, LZ Group. A two-

year collaboration between the two companies will see smart

parking technology solutions being brought to Bahrain and the

wider GCC region with the introduction of monPARK. Developed

by LZ Group, monPARK is a wireless solution that combines

mobile-based parking payment platforms and applications to

reduce traffic congestion. (GulfBase.com)

SIO launches subsidiary to manage properties – The Social

Insurance Organization (SIO) has launched a subsidiary named,

Amlak, to manage the long-term sustainable growth of its real

estate portfolio. Amlak will focus on maintaining optimal risks

and deliver above-the market returns for all SIO’s properties.

Other than building investment opportunities, Amlak will be

evaluating current properties and devising a development plan

to boost property values. (GulfBase.com)

MoT: Bahrain plans IPO for KSB port operator – According to

Ministry of Transportation (MoT), Bahrain is planning an IPO of

shares of the company operating its Khalifa Bin Salman port

(KSB port). KSB port has a capacity to handle about one million

20-foot equivalent units (TEUs) of container cargo annually and

is operated by APM Terminals Bahrain under a 25-year

concession. The company is 80% owned by Netherlands-based

APM Terminals and 20% by YBA Kanoo Holdings, a family-

controlled Bahraini business group. MoT said that under the

operating agreement for the port, the operator was to convert

from a closed joint-stock company to an open joint-stock

company within five years of the start of commercial operations.

(Bloomberg)

6. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg, * Markets closed on May 25, 2014

Source: Bloomberg, (* Market closed on May 26, 2014) Source: Bloomberg, (* Market closed on May 26, 2014)

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

0.5% 0.3%

(0.9%)

(0.5%)

(0.1%)

2.5%

1.9%

(1.6%)

(0.8%)

0.0%

0.8%

1.6%

2.4%

3.2%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,292.75 0.0 0.0 7.2 DJ Industrial* 16,606.27 0.0 0.0 0.2

Silver/Ounce 19.44 (0.1) (0.1) (0.2) S&P 500* 1,900.53 0.0 0.0 2.8

Crude Oil (Brent)/Barrel (FM

Future)

110.32 (0.2) (0.2) (0.4) NASDAQ 100* 4,185.81 0.0 0.0 0.2

Natural Gas (Henry

Hub)/MMBtu *

4.38 0.0 0.0 0.9 STOXX 600 343.69 0.6 0.6 4.7

LPG Propane (Arab Gulf)/Ton* 105.63 0.0 0.0 (16.3) DAX 9,892.82 1.3 1.3 3.6

LPG Butane (Arab Gulf)/Ton* 118.00 0.0 0.0 (13.6) FTSE 100* 6,815.75 0.0 0.0 1.0

Euro 1.36 0.1 0.1 (0.7) CAC 40 4,526.93 0.8 0.8 5.4

Yen 101.94 (0.0) (0.0) (3.2) Nikkei 14,602.52 1.0 1.0 (10.4)

GBP 1.68 0.1 0.1 1.7 MSCI EM 1,041.84 (0.1) (0.1) 3.9

CHF 1.12 0.1 0.1 (0.2) SHANGHAI SE Composite 2,041.48 0.3 0.3 (3.5)

AUD 0.92 0.1 0.1 3.6 HANG SENG 22,963.18 (0.0) (0.0) (1.5)

USD Index* 80.39 0.0 0.0 0.4 BSE SENSEX 24,716.88 0.1 0.1 16.8

RUB 34.20 0.1 0.1 4.0 Bovespa 52,932.91 0.6 0.6 2.8

BRL 0.45 (0.1) (0.1) 6.2 RTS 1,335.73 0.7 0.7 (7.4)

192.5

154.8

140.9