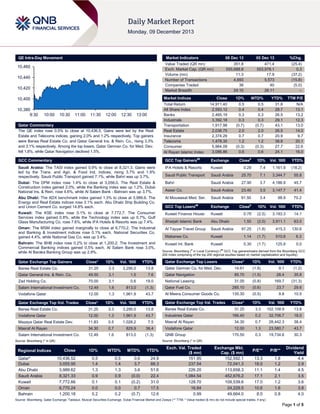

1. QE Intra-Day Movement

Market Indicators

10,460

10,440

10,420

05 Dec 13

%Chg.

351.8

555,688.8

11.3

4,693

38

24:10

471.4

553,978.1

17.9

5,573

40

26:11

(25.4)

0.3

(37.2)

(15.8)

(5.0)

–

Market Indices

10,400

10,380

9:30

08 Dec 13

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.5% to close at 10,436.5. Gains were led by the Real

Estate and Telecoms indices, gaining 2.0% and 1.2% respectively. Top gainers

were Barwa Real Estate Co. and Qatar General Ins. & Rein. Co., rising 3.3%

and 3.1% respectively. Among the top losers, Qatar German Co. for Med. Dev.

fell 1.8%, while Qatar Navigation declined 1.5%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,911.40

2,593.12

2,465.19

3,392.18

1,917.98

2,038.75

2,374.29

1,478.35

5,964.09

3,086.86

0.5

0.4

0.3

0.3

(0.7)

2.0

0.7

1.2

(0.3)

0.6

0.5

0.4

0.3

0.3

(0.7)

2.0

0.7

1.2

(0.3)

0.6

31.8

28.7

26.5

29.1

43.1

26.5

20.9

38.8

27.7

24.1

N/A

13.1

13.2

12.3

13.0

14.0

9.7

20.1

22.6

16.0

GCC Commentary

GCC Top Gainers##

Exchange

Saudi Arabia: The TASI index gained 0.9% to close at 8,321.3. Gains were

led by the Trans. and Agri. & Food Ind. indices, rising 3.7% and 1.9%

respectively. Saudi Public Transport gained 7.1%, while Bahri was up 3.7%.

IFA Hotels & Resorts

Kuwait

Saudi Public Transport

Dubai: The DFM index rose 1.4% to close at 3,056.0. The Real Estate &

Construction index gained 2.0%, while the Banking index was up 1.2%. Dubai

National Ins. & Rein. rose 4.6%, while Al Salam Bank - Bahrain was up 3.7%.

Abu Dhabi: The ADX benchmark index gained 1.3% to close at 3,989.6. The

Energy and Real Estate indices rose 3.1% each. Abu Dhabi Ship Building Co.

and Union Cement Co. surged 14.8% each.

Al Mouwasat Med. Ser.

GCC Top Losers

Exchange

Kuwait: The KSE index rose 0.1% to close at 7,772.7. The Consumer

Services index gained 0.8%, while the Technology index was up 0.7%. Gulf

Glass Manufacturing Co. rose 7.6%, while IFA Hotels & Resorts was up 7.4%.

Kuwait Finance House

Kuwait

0.79

(2.5)

3,193.3

14.1

Sharjah Islamic Bank

Abu Dhabi

1.50

(2.0)

3,911.1

63.0

Oman: The MSM index gained marginally to close at 6,770.2. The Industrial

and Banking & Investment indices rose 0.1% each. National Securities Co.

gained 4.4%, while National Gas Co. was up 3.4%.

Al Tayyar Travel Group

Saudi Arabia

97.25

(1.8)

415.3

130.6

Mabanee Co.

Kuwait

1.14

(1.7)

510.8

6.3

Kuwait Int. Bank

Kuwait

0.30

(1.7)

125.9

0.0

Bahrain: The BHB index rose 0.2% to close at 1,200.2. The Investment and

Commercial Banking indices gained 0.5% each. Al Salam Bank rose 3.0%,

while Al Baraka Banking Group was up 2.9%.

Barwa Real Estate Co.

Vol. ‘000

7.4

1,161.9

(18.2)

Saudi Arabia

25.70

7.1

3,344.7

55.8

Bahri

Saudi Arabia

27.90

3.7

4,188.9

45.7

Aseer Co.

Saudi Arabia

23.40

3.5

3,147.7

41.4

Saudi Arabia

91.50

3.4

98.9

70.2

##

#

Close

1D% Vol. ‘000

YTD%

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Close*

1D%

Vol. ‘000

YTD%

14.61

(1.8)

9.1

(1.2)

7.6

Qatar Navigation

85.70

(1.5)

28.4

35.8

1D%

Vol. ‘000

YTD%

3.3

3,295.0

13.8

1.5

1D%

0.29

Qatar German Co. for Med. Dev.

Close*

31.25

Qatar Exchange Top Gainers

Close#

Qatar Exchange Top Losers

Qatar General Ins. & Rein. Co.

49.50

3.1

Zad Holding Co.

70.00

3.1

0.6

19.0

National Leasing

31.05

(0.8)

169.7

(31.3)

Salam International Investment Co.

12.49

1.6

813.0

(1.3)

Qatar Fuel Co.

285.10

(0.6)

23.7

29.6

Vodafone Qatar

12.00

1.3

1,961.9

43.7

Al Meera Consumer Goods Co.

135.30

(0.5)

9.8

10.5

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

31.25

3.3

102,108.9

13.8

Close*

1D%

Vol. ‘000

YTD%

Barwa Real Estate Co.

31.25

3.3

3,295.0

13.8

Barwa Real Estate Co.

Vodafone Qatar

12.00

1.3

1,961.9

43.7

Industries Qatar

166.40

0.2

32,706.7

18.0

Mazaya Qatar Real Estate Dev.

11.83

0.5

1,028.2

7.5

Masraf Al Rayan

34.30

0.7

28,442.3

38.4

Masraf Al Rayan

34.30

0.7

829.9

38.4

Vodafone Qatar

12.00

1.3

23,580.7

43.7

Salam International Investment Co.

12.49

1.6

813.0

(1.3)

QNB Group

170.50

0.3

19,734.6

30.3

Qatar Exchange Top Vol. Trades

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Close

1D%

WTD%

MTD%

YTD%

10,436.52

3,055.95

3,989.62

8,321.33

7,772.66

6,770.24

1,200.18

0.5

1.4

1.3

0.9

0.1

0.0

0.2

0.5

1.4

1.3

0.9

0.1

0.0

0.2

0.6

3.7

3.6

(0.0)

(0.2)

0.7

(0.7)

24.9

88.3

51.6

22.4

31.0

17.5

12.6

Exch. Val. Traded

($ mn)

151.95

237.54

226.20

1,084.54

128.70

16.84

0.99

Exchange Mkt.

Cap. ($ mn)

152,592.1

72,041.3

113,658.3

452,676.2

109,539.6

24,229.5

49,664.0

P/E**

P/B**

13.3

18.0

11.1

17.1

17.0

10.6

8.0

1.8

1.2

1.4

2.1

1.2

1.6

0.8

Dividend

Yield

4.4

2.9

4.5

3.5

3.6

3.8

4.0

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 5

2. Qatar Market Commentary

The QE index rose 0.5% to close at 10,436.5. The Real Estate

and Telecoms indices led the gains. The index rose on the back

of buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Barwa Real Estate Co. and Qatar General Ins. & Rein. Co. were

the top gainers, rising 3.3% and 3.1% respectively. Among the

top losers, Qatar German Co. for Med. Dev. fell 1.8%, while

Qatar Navigation declined 1.5%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

70.51%

78.67%

(28,692,297.95)

Non-Qatari

29.49%

21.34%

28,692,297.95

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Sunday declined by 37.2% to

11.3mn from 17.9mn on Thursday. Further, as compared to the

30-day moving average of 11.8mn, volume for the day was 4.6%

lower. Barwa Real Estate Co. and Vodafone Qatar were the

most active stocks, contributing 29.3% and 17.4% to the total

volume respectively.

Ratings

Ratings Updates

Company

HSBC Bank Oman

Agency

Market

Type*

Fitch

Oman

IDR Grade/ SR/ VR*

Old Rating

New Rating

Rating Change

Outlook

Outlook Change

A+/A+/BB

A+/A+/BB+*

*

–

–

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC –

Local Currency) (*– Rating revised)

News

Qatar

QNB: Qatar’s non-energy sector to form half of GDP by

2015 – QNB Group’s Head of Economics Joannes Mongardini

said that the country’s diversifying economy will soon reach a

key milestone with its non-hydrocarbon sector being worth more

than half of Qatar’s GDP by 2015. In 2012, Qatar’s GDP stood

at $192bn, of which the hydrocarbon (oil & gas) sector

accounted for 58%. Qatar’s non-hydrocarbon sector is slated to

grow from 42% in 2012 to more than 50% by 2015 due to the

mega infrastructure projects being implemented for the FIFA

World Cup 2022. Meanwhile, Qatar’s real GDP is expected to

grow by 6.5% in 2013 and 6.8% in 2014, with 240,000 jobs

expected to be added in 2014. (Bloomberg)

QP signs MoU to construct butadiene extraction, elastomer

complex – Qatar Petroleum (QP) has entered into a MoU with

Zeon Corporation and Mitsui & Co. Ltd for the construction of its

butadiene extraction and elastomer complex in Qatar’s industrial

city of Ras Laffan. This plant will produce rubber from chemicals

made at the planned petrochemical complex. (Bloomberg)

QGRI to study converting QGHC into private shareholding –

The Qatar General Insurance & Reinsurance Company’s

(QGRI) management has decided to carry out a study to convert

the Qatar General Holding Company (QGHC) from a “one

person company” to a “private shareholding company”. This

move will separate its real estate and investment activities into a

separate legal entity. (QE)

Economic Zones Company renamed as Manateq – The

state-owned Economic Zones Company will be known as

“Manateq” from now on. Manateq and its economic zones will

focus on creating the right environment for the smooth and longterm operation of its clients along with facilitating opportunities

for excellent returns. (Gulf-Times.com)

Qatar, UAE markets’ upgrade to bring in $350mn from ETFs

– According to Abu Dhabi Investment Company (Invest AD), the

global index compiler MSCI's upgrading of Qatar and the UAE

markets to “emerging” status would bring in around $350mn

from exchange traded funds (ETFs) alone. The MSCI upgrade

from frontier status to emerging market status for the UAE and

Qatar would also encourage greater participation by active

emerging market institutional investors over the long term. (GulfTimes.com)

NLCS’ BoD to meet on December 11 – Alijarah Holding’s

(NLCS) board of directors will meet on December 11, 2013 to

discuss routine agenda matters. (QE)

QU’s Al-Jarrah appointed as Commercial Bank Chair of

Banking – The Commercial Bank of Qatar appointed Idries

Mohamed al-Jarrah, Professor of Finance at Qatar University’s

Department of Finance & Economics, as the “Commercial Bank

Chair of Banking”. Professor al-Jarrah holds the position of

endowed professor and works in Qatar University’s College of

Business and Economics. As the Chair of Banking, Professor alJarrah will lead studies in the field of banking and finance, which

will provide the Qatari banking industry with suitably qualified

graduates. (Gulf-Times.com)

International

HSBC considers floating UK banking business – According

to the Financial Times, HSBC Holdings Plc is considering the

flotation of up to 30% of its British retail and commercial banking

arm, in a move to cope with the proposed new rules that force

British banks to ring-fence their retail arms. FT said the plan was

at an early stage, but the matter had been discussed with

investors and informally at the board level. The FT report added

that investors estimate such a business could float with a market

capitalization of around £20bn ($32.7bn).

European banks trim risk but fail to raise provisions ahead

of EU review – Most of Europe's big banks shed their risky

assets in the quarter ended September 2013, but they are yet to

take extra provisions against doubtful loans in time for a critical

review by regulators. A Reuters analysis of the third-quarter

results of Europe's 30 largest banks found that almost two-thirds

of the 27 that report detailed quarterly figures said their balance

sheets were less risky at the end of September than at the end

of June, which means that they need less capital. However,

almost two-thirds of the banks took lower charges for loan

Page 2 of 5

3. losses in the third quarter than a year earlier, and the coverage

ratio rose only marginally. More action is expected in the fourth

quarter, as banks learn more about the standards the ECB will

apply in the Eurozone and national regulators will apply

elsewhere. (Reuters)

Japan posts slower growth in 3Q2013, surprise currentaccount deficit – Japan’s third-quarter growth was slower than

initially estimated, as annualized GDP growth was revised

downwards to 1.1% QoQ from 1.9% earlier. Further, the nation

posted a surprise ¥128bn ($1.2bn) current-account deficit, while

the median estimate was a surplus of ¥149bn. (Bloomberg)

Nobel Economics winner Fama feels risk of global

recession in 2014 – According to Eugene Fama – this year's

Nobel Prize winner for Economics – highly indebted

governments in the US and Europe posed a constant threat to

the global economy. Fama said that a time will come when the

financial markets will say none of their debts is credible anymore

and they can't finance themselves. Fama stated that he was not

reassured from the strong US labor market data, as

unemployment rate has fallen to 7% because people have given

up looking for jobs. (Reuters)

Regional

IATA: Mideast carriers post strongest traffic growth in

October – The International Air Transport Association (IATA)

said airlines in the Middle East have recorded their strongest

YoY traffic growth in October 2013, on the back of growing

demand in business and leisure travel. The load factor of Middle

East airlines stayed at 75.5% in October 2013. IATA said that

Middle Eastern carriers have stayed ahead of their global peers

by registering a 14% growth in October 2013 and are set to

contribute a significant share in carrying a record high number of

3bn passengers in the global airline industry in 2013.

(GulfBase.com)

E&Y: MENA authorities move to strengthen corporate tax

regime – According to Ernst & Young (E&Y), tax authorities in

the Middle East & North Africa (MENA) region have enhanced

scrutiny and compliance enforcement regarding withholding tax

laws. MENA tax authorities have increased scrutiny and

enforcement of compliance on withholding tax laws to ensure

that foreign companies who do business without a business

facility in the country are also subject to tax on incomes earned

from the country. Further, there has been an increased focus on

transfer pricing regulations to ensure that business transactions

between related parties are conducted at an arm’s length. (GulfTimes.com)

WTO deal to strengthen competitive position of Saudi

products – Saudi Arabia has welcomed the $1tn World Trade

Organization (WTO) agreement signed in Bali recently. Saudi

Commerce & Industry Minister Tawfiq Al Rabiah said this

agreement will strengthen the competitive position of Saudi

products and boost global trade. Further, he stated the deal will

enable Saudi exporters to supply their goods in targeted

markets at shorter time and at a lesser cost. (GulfBase.com)

IMF: Saudi bank credits poised to grow by 15.3% in 2014 –

According to a report by the International Monetary Fund (IMF),

bank credits destined for the private sector in Saudi Arabia are

poised to grow by 15.3% in 2014 as compared to 15.6% in

2013, which is the highest among the GCC countries. As per the

IMF report, Qatar has the second largest bank credit growth

among the GCC countries forecasted at 14.7% in 2014 (12.9%

in 2013), followed by Oman at 12.6% (14.3%), and the UAE at

8.4% (6%). The report showed that despite low interest rates,

there is a discrepancy in the growth of bank credits offered to

the private sector in the GCC region. However, financial

institutions in the GCC region are characterized by solid

positions despite the increasing rates of non-performing loans

(NPLs) in Bahrain and the UAE in 2013. Further, the report

showed that banking institutions in the GCC countries are well

positioned in their capitals and have enough provisions for bad

loans. IMF has appreciated banking measures taken by Saudi

Arabia, which was the first GCC country to apply Basel II rules.

(GulfBase.com)

Pentair to set up manufacturing, service facility in Dammam

– Swiss-based Pentair has entered into a term sheet with Ali

Abdullah Al Tamimi Company to set up a manufacturing and

service facility in Dammam. Through this new partnership,

Pentair will be able to locally manufacture some of its premium

products for serving both the local and export markets.

(GulfBase.com)

Almarai to acquire MJN’s shares in IPNC for SR15mn –

Almarai Company announced that it will acquire the shares held

by Mead Johnson Nutrition (MJN) in the International Pediatric

Nutrition Company (IPNC) for SR15mn. This purchase will be

financed from Almarai’s operational cash flows. (Tadawul)

SCC’s BoD recommends SR126.48mn dividends – The

Saudi Chemical Company’s (SCC) board of directors has

recommended the distribution of dividends worth SR126.48mn

(SR2 per share), representing 20% of the face value on January

30, 2014. SCC’s shareholders, who are registered with the

Securities Depository Center on January 16, 2014, will be

eligible for this dividend. (Tadawul)

Dubai foreign trade hits AED1tn by end of September 2013

– Dubai's non-oil foreign trade reached a total volume of

AED1.009tn by the end of Q3, compared to AED918bn for the

same period in 2012. Dubai Customs statistics show that

Dubai's non-oil foreign trade growth was the result of the

increase in imports till Q3 of 2013; reaching AED610bn, as

compared to AED546bn in the same period last year. In

addition, exports and re-exports rose to AED399bn, compared

to AED372bn. (Gulfbase.com)

Dubai’s non-oil foreign trade crosses AED1tn for 9M2013 –

Dubai's non-oil foreign trade has crossed the AED1tn mark

during January-September 2013 as compared to AED918bn in

January-September 2012. According to data released by Dubai

Customs, the Emirate’s imports reached AED610bn, as

compared to AED546bn in the year-earlier period, with exports

and re-exports rising to AED399bn from AED372bn.

(Bloomberg)

DED: Tourist spending in Dubai to reach AED33bn by 2017

– Dubai’s Department of Economic Development (DED) Director

General Sami Al Qamzi said the tourist spending in Dubai is

expected to reach around AED33bn by 2017, while total sales

are expected to increase 5.7% annually during 2013-2017. Al

Qamzi said that Dubai was well on course to achieve its Tourism

Vision for 2020 of attracting 20mn tourists and AED300bn in

tourism revenues annually, of which a major share will come

from retail sales. (Bloomberg)

DIFCA signs strategic deal with TFSA – The Dubai

International Financial Centre Authority (DIFCA) has signed a

strategic agreement with the Toronto Financial Services Alliance

(TFSA) to foster business collaboration in their respective

financial centers. Under this agreement, DIFCA and TFSA will

explore avenues to jointly promote the offerings of Toronto and

Dubai financial services sectors across the globe. (Bloomberg)

Dewa’s operational budget to reach AED13.151bn in 2014 –

The Dubai Electricity & Water Authority’s (Dewa) CEO Saeed

Page 3 of 5

4. Mohammed Al Tayer said Dewa’s operational budget will reach

AED13.151bn in 2014, while its capital administrative budget will

touch AED352mn. Al Tayer said that expenditure on projects

and purchases will reach AED7.057bn in 2014. The growing

budget expenditure represents Dewa’s pursuit to ensure

adequate electricity and water requirements for supporting the

Emirate’s ambitious development plans. (GulfBase.com)

Al Noor Hospitals plans to expand in Dubai – Al Noor

Hospitals Group’s Chief Strategy Officer Sami Alom said the

group is planning to expand in Dubai after the Emirate

announced plans for making health insurance mandatory. This

expansion will be most likely done through acquisitions.

(GulfBase.com)

ADPC to take charge of Zayed Port in January – The Abu

Dhabi Ports Company (ADPC) will take charge of the

management and operations of the Zayed Port from January 1,

2014 from Abu Dhabi Terminals (ADT). (GulfBase.com)

CBO issues tenders for OMR222mn CDs – The Central Bank

of Oman (CBO) has issued tenders for Certificates of Deposit

(CD) worth OMR222mn. These CDs, which will mature on

January 1, 2014, carry an average rate of interest of 0.13%,

while the maximum accepted interest rate is 0.13%.

(GulfBase.com)

Page 4 of 5

5. Rebased Performance

Daily Index Performance

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

1.3%

150.0

0.9%

119.5

0.5%

QE Index

Oct-11

May-12 Dec-12

S&P Pan Arab

Jul-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Yen

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

1,229.05

0.0

0.0

(26.6)

DJ Industrial

19.51

0.0

0.0

(35.7)

S&P 500

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

1.37

0.0

0.0

0.0

111.61

4.14

127.00

139.50

0.5

20.9

41.1

(21.0)

3.9

102.91

GBP

1.63

0.0

0.0

CHF

1.12

0.0

0.0

0.91

0.0

0.0

(12.4)

80.32

0.0

0.0

32.72

0.0

0.0

0.43

0.0

0.0

USD Index

RUB

BRL

0.0%

Close

1D%

WTD%

YTD%

16,020.20

0.0

0.0

22.3

1,805.09

0.0

0.0

26.6

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

4,129.37

0.0

0.0

13.4

0.0

47.2

Source: Bloomberg

0.0

AUD

0.2%

Dubai

Aug-10 Mar-11

Kuwait

0.0%

Qatar

0.1%

Abu Dhabi

0.5%

Oman

1.0%

Bahrain

131.5

Saudi Arabia

Jan-10

1.4%

1.5%

NASDAQ 100

STOXX 600

DAX

FTSE 100

CAC 40

316.50

9,172.41

6,551.99

34.5

13.2

20.5

11.1

15,299.86

0.0

0.6

MSCI EM

1,002.20

0.0

0.0

(5.0)

2.6

SHANGHAI SE Composite

2,237.11

0.0

0.0

(1.4)

HANG SENG

23,743.10

0.0

0.0

4.8

0.7

BSE SENSEX

20,996.53

0.0

0.0

8.1

7.2

Bovespa

50,944.27

0.0

0.0

(16.4)

1,390.61

0.0

0.0

(8.9)

18.6

(12.0)

Source: Bloomberg

Nikkei

4,062.52

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5