Download to read offline

![HYPERLINK \"

http://waytoohigh.wordpress.com/2009/02/06/25-issues-affecting-credit-card-interchange-fees/\"

\o \"

Permanent Link: 25 Issues Affecting Credit Card Interchange Fees\"

25 Issues Affecting Credit Card Interchange Fees1) Merchants’ interchange fees have risen even though network fees are decreasing.2) The credit card companies have an unbridled ability to raise fees at will. Member banks of the credit card associations are in our opinion, co-conspirators.3) From 1999 – 2005, the PIN debit fees rose 267 percent.4) In the early 1990s there were about a dozen separate interchange fees, today there are nearly one hundred. These interchange fees seemingly always increase and have not decreased. 5) Visa and MasterCard fix uniform credit card interchange fees, which are agreed to and used by all Visa and MasterCard banks.6) This collective horizontal price fixing violates Section 1 of the Sherman Act.7) Even the cost for paying out reward benefits to affinity card holders has declined and is getting more stingy. Ex: American Airlines now charges a fee of $250 each- way to cash in frequent flier mileage to upgrade from coach to business-class on international flights. This is an audacious game few understand.The credit card associations are extending loyalty and kick-back programs to consumers which few can actually figure out the value of. If merchants could even figure their actual cost – from nearly one-hundred separate rates – and listed the actual Interchange fee as a separate item on the customers’ receipt, people would be less likely to want frequent flier mileage rewards once they understood how much more they are actually paying for those perks.9) This is a hidden tax on consumers and merchants.10) With today’s technologies, the interchange structure is now inefficient. In our opinion, consumers don’t benefit and merchants don’t benefit.11) Part of this inefficiency relates to credit card companies where only 1 in 2000 of their mail solicitations lead to signing up just one new cardholder. Credit card companies mailed out about 5.24 billion mail solicitations in 2005 yet only 4-10ths of 1% reply. This means 5 billion pieces of mail are garbage. What other industry has such huge profits that they can afford to throw away 5 billion pieces of junk mail every year?12) Why does it cost so much to use a credit and debit card, rather than with writing a check? There is a zero interchange fee for checks, the money goes directly from the consumer to the retailer. Example: The checking system works without any of these fees. The difference between credit card and check fees are also a study in competition; banks impose various fees on account holders and on merchants for writing and processing checks, from zero to a variety of rates in order to stay competitive.13) Today, the card associations have lower costs and even no float expense when debit cards are used. With technology, there is less fraud and no need for paper receipts. Processing and telecommunication fees are lower and now automated. With interest rates so low for so long, even the cost of the the regular float has declined.14) Merchants shouldn’t have to cover the cost for card holder credit risks. Defaults by card holders should not be paid by merchants, but rather, issuers should be more careful who they extend credit to.15) There is no ability to bypass the credit card network. For instance, ScanMyPhotos.com(a lead defendant in the merchant interchange litigation) operates an international online photo scanning and digital imaging service where all online orders require transactions to be completed with credit cards, this parallels the entire online retail segment.16) Part of the proof that the card association and their interchange fees are a monopoly is that even though rates continue to rise, merchants are forced to use their products.17) Trickery and confusion. Even though there are lower interchange rates for debit cards, it is increasingly more difficult to distinguish debit cards. It’s difficult to see the “debit” or “check card” reference and retail clerks can easily ring up the sale as a charge card, thus paying higher rates.18) When consumers present merchants with faulty magnetic strips on their cards it cannot be swiped by the card reader. This causes merchants to then manually enter the number, which costs more even though there is an identical risk to the card association. But, the charge for manually entering a card is excessively higher, and even higher if the address and zip code are not entered.19) In 1994, the Visa and MasterCard interchange fees on a $100 transaction for the largest non-supermarkets was about 1% and 1.33%, today it is about 1.70% and higher. For the smallest non-supermarket merchants, the charge was about 1% and 1.31% in 1994; today it is higher too.20) There is no added direct value or benefit to the merchant by accepting an affinity card or any other card, such as the Visa Signature card.21) Australia, the European Union and the United Kingdom are samples where interchange regulations work. The U.S. is the only market where interchange fees are increasing. Canada, for example, has a zero interchange fee for debit cards and their PIN Network is the most popular way to transaction business. U.S. Interchange fees are 3-times higher than in Australia and two-times higher than in the UK. Australia is a great example – since the nation regulated these rates, merchants paid $500 million less. This translates into lower costs to consumers. The Australian CPI actually declined and there was an increase in card usage.22) The only leverage merchants have is in choosing their payment processor. Those fees are highly competitive, yet the Interchange fees cannot be negotiated.23) Because banks are now permitted to issue Amex and Discover cards, MBNA and Citibank plan to issue Amex cards, which means, merchants will be flooded with the higher costing premium cards (this translates into a 50% increase in costs from about 140 bp [basis points] to 210 bp. I anticipate they will then convert their classic cards to higher priced “signature” “affinity” and “business” cards.24) The argument by Amex was that their card holders spend more money. Perhaps this is based on buying diamonds and luxury items, but when you are at a convenience store, the amount charged from a Visa card is typically the same as for Amex. As MBNA and Citibank switch from Visa to Amex, they are appealing to the same group of cardholders with the same spending patterns.25) How can groups like “Americans for Consumer Education and Competition” be expected to be objective? [(ACEC was financially supported by VISA USA]. They suggest merchants want to pass along the interchange fees to consumers. The fact is that this litigation has nothing to do with “shifting’ costs from merchants to consumers, but rather it is about reforming the system so that competition works and will drive total costs down so that both merchants and cardholders have lower costs.](https://image.slidesharecdn.com/25issuesaffectingcreditcardinterchange-12538051702271-phpapp03/85/25-Issues-Affecting-Credit-Card-Interchange-1-320.jpg)

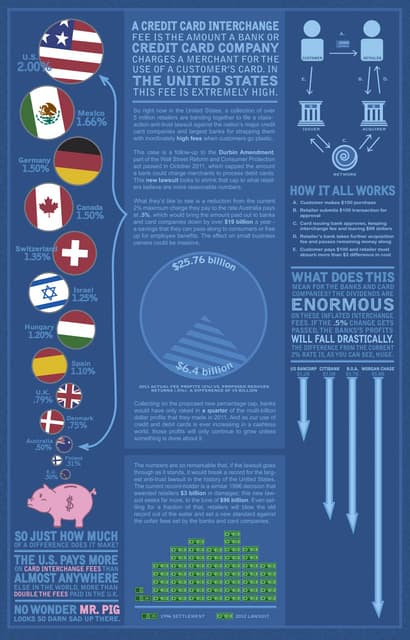

This document outlines 25 issues with credit card interchange fees that negatively impact both merchants and consumers. Key issues discussed include interchange fees rising significantly over time even as processing costs have decreased, a lack of transparency in the complex fee structure, and an inability for merchants to negotiate fees or bypass the credit card networks. The document argues that regulating interchange fees as done in other countries would lower costs for both merchants and consumers while not reducing card usage.