Downloaded 18 times

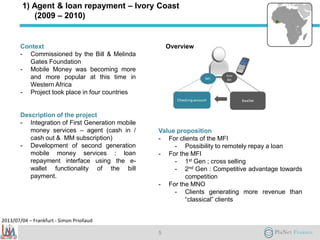

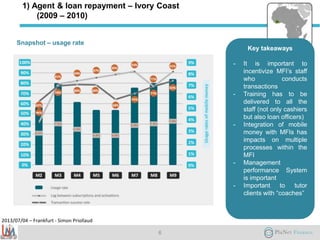

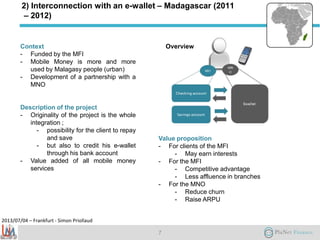

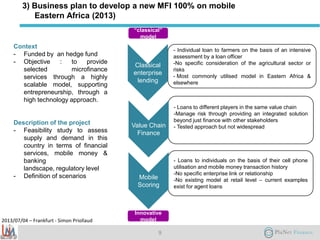

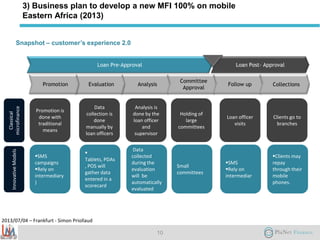

Simon Priollaud presented 4 case studies on mobile banking projects in Africa: 1) A project in Ivory Coast from 2009-2010 integrated mobile money services with microfinance institutions, allowing loan repayments via mobile and generating more revenue. Key lessons included incentivizing staff and thorough client training. 2) A 2011-2012 Madagascar project interconnected an e-wallet with a microfinance institution, enabling savings, loans, and transfers. Regulatory coordination and technical challenges required attention. 3) A 2013 study in East Africa analyzed demand for fully mobile microfinance. Scenarios included individual loans, value chain lending, and mobile scoring models. 4) A 2013 Morocco project tested us