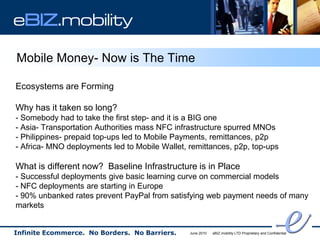

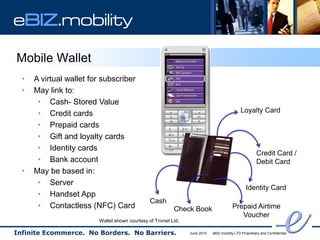

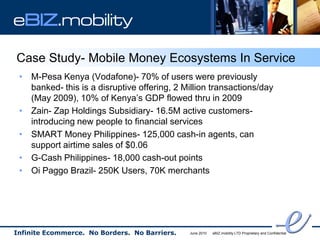

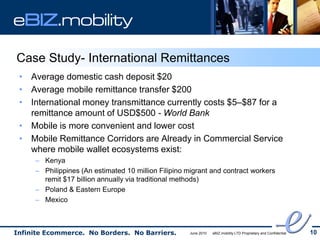

The document discusses how mobile network operators can earn revenue from mobile financial services. It provides examples of existing mobile money ecosystems, international remittance services, mobile payments for online purchases and gambling. The document argues that mobile payments can facilitate e-commerce in developing markets where credit card usage is low. It also suggests that mobile banking can reduce costs for financial institutions. Overall, the document advocates for collaboration between mobile operators, financial institutions, and merchants to establish ubiquitous mobile wallet platforms and payment standards.

![S365 M Commerce Africa Overview June 09 Linkedin.Ppt [Compatibility Mode]](https://cdn.slidesharecdn.com/ss_thumbnails/s365mcommerceafricaoverviewjune09linkedinpptcompatibilitymode-124465131045-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)