Call Girls In Yusuf Sarai Women Seeking Men 9654467111

20 May Daily market report

1. Page 1 of 6

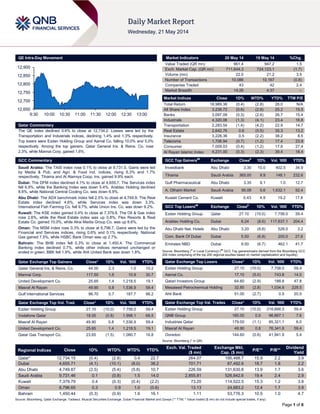

QE Intra-Day Movement

Qatar Commentary

The QE index declined 0.4% to close at 12,734.2. Losses were led by the

Transportation and Industrials indices, declining 1.4% and 1.3% respectively.

Top losers were Ezdan Holding Group and Aamal Co. falling 10.0% and 5.0%

respectively. Among the top gainers, Qatar General Ins. & Reins. Co. rose

2.3%, while Mannai Corp. gained 1.6%.

GCC Commentary

Saudi Arabia: The TASI index rose 0.1% to close at 9,731.5. Gains were led

by Media & Pub. and Agri. & Food Ind. indices, rising 6.3% and 1.7%

respectively. Tihama and Al Alamiya Coop. Ins. gained 9.9% each.

Dubai: The DFM index declined 4.1% to close at 4,655.7. The Services index

fell 6.9%, while the Banking Index was down 5.4%. Arabtec Holding declined

8.6%, while National Central Cooling Co. was down 6.9%.

Abu Dhabi: The ADX benchmark index fell 2.5% to close at 4,749.9. The Real

Estate index declined 4.6%, while Services index was down 3.3%.

International Fish Farming Co. fell 9.7%, while Union Ins. Co. was down 9.2%.

Kuwait: The KSE index gained 0.4% to close at 7,379.8. The Oil & Gas index

rose 2.6%, while the Real Estate index was up 0.8%. Flex Resorts & Real

Estate Co. gained 10.0%, while Alrai Media Group Co. was up 8.6%.

Oman: The MSM index rose 0.3% to close at 6,796.7. Gains were led by the

Financial and Services indices, rising 0.6% and 0.1% respectively. National

Gas gained 7.5%, while HSBC Bank Oman was up 2.7%.

Bahrain: The BHB index fell 0.3% to close at 1,450.4. The Commercial

Banking index declined 0.7%, while other indices remained unchanged or

ended in green. BBK fell 1.9%, while Ahli United Bank was down 1.8%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar General Ins. & Reins. Co. 44.00 2.3 1.0 10.2

Mannai Corp. 117.50 1.6 10.9 30.7

United Development Co. 25.65 1.4 1,218.5 19.1

Masraf Al Rayan 49.90 0.8 1,536.9 59.4

Gulf International Services 96.70 0.7 187.7 98.2

Qatar Exchange Top Vol. Trad. Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 27.10 (10.0) 7,758.0 59.4

Vodafone Qatar 18.05 (0.8) 1,998.1 68.5

Masraf Al Rayan 49.90 0.8 1,536.9 59.4

United Development Co. 25.65 1.4 1,218.5 19.1

Qatar Gas Transport Co. 23.65 (1.5) 1,080.7 16.8

Market Indicators 20 May 14 19 May 14 %Chg.

Value Traded (QR mn) 961.4 947.2 1.5

Exch. Market Cap. (QR mn) 711,644.3 724,123.1 (1.7)

Volume (mn) 22.0 21.2 3.5

Number of Transactions 10,086 10,167 (0.8)

Companies Traded 43 42 2.4

Market Breadth 14:26 4:37 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,989.36 (0.4) (2.8) 28.0 N/A

All Share Index 3,238.72 (0.6) (2.8) 25.2 15.5

Banks 3,097.09 (0.3) (2.6) 26.7 15.4

Industrials 4,320.06 (1.3) (4.1) 23.4 16.8

Transportation 2,283.54 (1.4) (4.2) 22.9 14.7

Real Estate 2,642.76 0.6 (0.5) 35.3 13.2

Insurance 3,228.36 0.5 (2.2) 38.2 8.5

Telecoms 1,706.94 (0.7) (1.2) 17.4 23.9

Consumer 7,009.03 (0.4) (1.2) 17.8 27.4

Al Rayan Islamic Index 4,231.00 (0.3) (2.3) 39.4 18.4

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Investbank Abu Dhabi 3.30 10.0 402.5 34.9

Tihama Saudi Arabia 365.00 9.9 148.1 232.6

Gulf Pharmaceutical Abu Dhabi 3.35 9.1 1.0 12.7

A. Othaim Market Saudi Arabia 95.08 5.6 1,632.1 52.4

Kuwait Cement Co. Kuwait 0.43 4.9 19.2 17.8

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Ezdan Holding Group Qatar 27.10 (10.0) 7,758.0 59.4

Arabtec Holding Co. Dubai 6.24 (8.6) 117,637.1 204.4

Abu Dhabi Nat. Hotels Abu Dhabi 3.20 (8.6) 526.0 3.2

Com. Bank Of Dubai Dubai 5.50 (6.8) 200.0 27.6

Emirates NBD Dubai 9.00 (6.7) 462.1 41.7

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 27.10 (10.0) 7,758.0 59.4

Aamal Co. 17.10 (5.0) 743.8 14.0

Qatari Investors Group 64.60 (2.9) 188.8 47.8

Mesaieed Petrochemical Holding 32.85 (2.8) 1,034.8 228.5

Ahli Bank 51.00 (2.7) 0.5 20.5

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Ezdan Holding Group 27.10 (10.0) 216,666.5 59.4

QNB Group 185.00 0.0 96,667.1 7.6

Industries Qatar 179.00 (1.1) 85,321.1 6.0

Masraf Al Rayan 49.90 0.8 76,341.8 59.4

Ooredoo 144.60 (0.6) 41,941.9 5.4

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,734.15 (0.4) (2.8) 0.4 22.7 264.07 195,488.7 15.9 2.2 3.9

Dubai 4,655.71 (4.1) (10.1) (8.0) 38.2 701.71 87,492.9 18.7 1.8 2.2

Abu Dhabi 4,749.87 (2.5) (5.4) (5.8) 10.7 226.59 131,630.8 13.9 1.7 3.6

Saudi Arabia 9,731.46 0.1 (0.8) 1.5 14.0 2,855.81 526,842.6 19.4 2.4 2.9

Kuwait 7,379.79 0.4 (0.3) (0.4) (2.2) 73.20 114,522.5 15.3 1.2 3.8

Oman 6,796.65 0.3 0.9 1.0 (0.6) 13.13 24,683.2 12.4 1.7 3.9

Bahrain 1,450.44 (0.3) (0.9) 1.6 16.1 1.11 53,776.3 10.5 1.0 4.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,650

12,700

12,750

12,800

12,850

12,900

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QE index declined 0.4% to close at 12,734.2. The

Transportation and Industrials indices led the losses. The index

fell on the back of selling pressure from Qatari shareholders

despite buying support from non-Qatari shareholders.

Ezdan Holding Group and Aamal Co. were the top losers, falling

10.0% and 5.0% respectively. Among the top gainers, Qatar

General Ins. & Reins. Co. rose 2.3%, while Mannai Corp. gained

1.6%.

Volume of shares traded on Tuesday rose by 3.5% to 22.0mn

from 21.2mn on Monday. However, as compared to the 30-day

moving average of 30.1mn, volume for the day was 27.1% lower.

Ezdan Holding Group and Vodafone Qatar were the most active

stocks, contributing 35.3% and 9.1% to the total volume

respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Bank Al Bilad Moody’s

Saudi

Arabia

LCR /FCR/ BFSR – A2 / P-1 / C- – Stable

–

Source: News reports (* LT – Long Term, ST – Short Term, BFSR- Banking Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support

Rating, LC – Local Currency)

Earnings Releases

Company Market Currency

Revenue

(mn)1Q2014

% Change

YoY

Operating Profit

(mn) 1Q2014

% Change

YoY

Net Profit (mn)

1Q2014

% Change

YoY

Egypt Kuwait Holding Co.

(EKH)

Kuwait KD – – – – 6.0 20.5%

Arabi Holding Group Co.

(AGHC)

Kuwait KD – – – – 0.3 24.6%

Mushrif Trading &

Contracting Co. (MTCC)

Kuwait KD – – – – 0.7 27.5%

Al-Massaleh Real Estate Co. Kuwait KD – – – – 0.0 -92.9%

Salbookh Trading Co. (STC) Kuwait KD – – – – 0.1 91.9%

Wethaq Takaful Insurance

Co.

Kuwait KD – – – – 0.3 153.0%

Combined Group

Contracting Co. (CGC)

Kuwait KD – – – – 0.6 -78.0%

Kuwait & Middle East

Financial Investment Co.

(KMEFIC)

Kuwait KD – – – – 0.2 -46.0%

Gulf Finance House (GFH) Kuwait KD – – – – 0.1 -79.6%

Kuwait Real Estate Co.

(KREC)

Kuwait KD – – – – 1.8 9.2%

Alshamel International

Holding Co.

Kuwait KD – – – – 0.1 -81.8%

Global Investment House Bahrain KD 6.1 86.0% – – 3.1 NA

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

05/20 Germany Destatis PPI MoM April -0.10% 0.00% -0.30%

05/20 Germany Destatis PPI YoY April -0.90% -0.90% -0.90%

05/20 UK ONS CPI MoM April 0.40% 0.30% 0.20%

05/20 UK ONS CPI YoY April 1.80% 1.70% 1.60%

05/20 UK ONS CPI Core YoY April 2.00% 1.80% 1.60%

05/20 UK ONS Retail Price Index April 255.7 256.1 254.8

05/20 UK ONS RPI MoM April 0.40% 0.50% 0.20%

05/20 UK ONS RPI YoY April 2.50% 2.60% 2.50%

05/20 UK ONS RPI Ex Mort Int.Payments (YoY) April 2.60% 2.70% 2.50%

05/20 UK ONS PPI Input NSA MoM April -1.10% -0.20% -0.40%

05/20 UK ONS PPI Input NSA YoY April -5.50% -4.90% -6.30%

05/20 UK ONS PPI Output NSA MoM April 0.00% 0.20% 0.20%

05/20 UK ONS PPI Output NSA YoY April 0.60% 0.70% 0.50%

05/20 UK ONS PPI Output Core NSA MoM April 0.00% 0.10% 0.20%

Overall Activity Buy %* Sell %* Net (QR)

Qatari 53.20% 56.22% (28,900,515.95)

Non-Qatari 46.79% 43.79% 28,900,515.95

3. Page 3 of 6

05/20 UK ONS PPI Output Core NSA YoY April 1.00% 1.00% 1.10%

05/20 UK ONS ONS House Price YoY Mar 8.00% 9.60% 9.20%

05/20 Italy ISTAT Industrial Sales MoM March 0.30% – -1.40%

05/20 Italy ISTAT Industrial Sales WDA YoY March 2.70% – 1.30%

05/20 Italy ISTAT Industrial Orders MoM March 1.30% 0.30% -3.20%

05/20 Italy ISTAT Industrial Orders NSA YoY March 2.80% 3.50% 2.80%

05/20 Italy Banca D'Italia Current Account Balance March 1005M – 298M

05/20 Japan MITI All Industry Activity Index MoM March 1.50% 1.60% -1.10%

05/20 Japan ESRI Leading Index CI March 107.1 – 106.5

05/20 Japan ESRI Coincident Index March 114.5 – 114.0

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

VFQS’ March 31, 2014 customer base reaches 1,327,000,

which is right in line with our estimate – Vodafone Qatar

(VFQS) continues to expand its mobile customer base in Qatar,

growing its number of customers by 22% YoY to reach

1,327,000 customers as at March 31, 2014. VFQS’ CEO Kyle

Whitehill said that 62% of Qatar’s population is using VFQS’

services every month, which is a great achievement for the

company’s shareholders, staff and partners. Reported mobile

subscriber base came in around 1% below our estimate of

1,340,149. VFQS reports FY2014 results after its board meeting

on May 27, 2014 and we continue to expect improving financial

metrics. We are projecting QR543mn in revenue for 4QFY2014

(+7% QoQ, +25% YoY). We model net loss to decline to

QR50mn versus QR53mn and QR74mn in December 2013 and

March 2013 quarters, respectively. Finally, we continue to

expect VFQS to pay QR0.10 in DPS for FY2014. We rate VFQS

an Underperform with a price target of QR13.95. (VFQS Press

release, QNBFS Research)

CEBR: Qatar must boost manufacturing base, labor

productivity – According to a report by the Centre for

Economics & Business Research (CEBR), a partner of the

global body of chartered accountants (ICAEW), with global oil

prices expected to decline in the long term, Qatar must step up

efforts to strengthen its manufacturing base and enhance labor

productivity. CEBR said commodities account for 93% of Qatar’s

total goods exports by value, while manufacturing activities

account for less than 10% of goods export revenues. ICAEW’s

Executive Director Vernon Soare said strong investment will

continue to see growth in Qatar outpacing the rest of the world.

But the prospect of falling oil prices due to increasing global

supply, will put pressure on the Gulf country to diversify and

grow its high-tech manufacturing industries. (Gulf-Times.com)

Real estate market sees revival again – After weeks of

stagnation, Qatar’s real estate market has begun to show signs

of revival, which is evident from QR1.63bn worth of transactions

concluded in the week ended on May 15, 2014. Around 242

transactions were recorded by the Real Estate Registration

Department at the Ministry of Justice in the week from May 11 to

15, 2014. According to sources, the total value was QR1.63bn,

up from less than QR1bn worth of deals in the previous weeks.

Meanwhile, real estate expert, Khalifa Al Muslemani said that

the demand for real estate was high at the moment and the

sector is set to witness 25% growth in the first half of this year

over the corresponding period of 2013, fuelled by demand.

(Peninsula Qatar)

Mesaimeer tunnel work begins – The Public Work Authority’s

(Ashghal) President Engineer Nasser bin Ali Al Mawlawi

inaugurated the excavation works for Mesaimeer Surface &

Ground Water Tunneling, a significant project undertaken to

enhance Qatar’s drainage network. Excavation is being carried

out by technologically advanced tunnel boring machines that are

being used for the first time in Qatar. The tunnel will run under

F-Ring Road, stretching 9.7 kilometers. It will run 5.4 kilometers

from Al Thummama to the west and 4.3 kilometers to the east to

the planned pumping station near the new Hamad International

Airport. The tunnel will alleviate Doha’s storm water by

transporting it from a 170km catchment area, covering southern

and western parts of greater Doha. (Peninsula Qatar)

International

US export control reforms help US firms – According to a US

Commerce Department official, export control reforms are

helping companies in the US to sell more goods overseas at a

time when US defense spending is declining. Commerce

Undersecretary Eric Hirschhorn said that moving some items

from the State Department's tightly controlled munitions list to

the Commerce Department's list of items that could be more

easily exported to allies was speeding up the export process

and helping US companies. He said it would also eliminate the

ability of US competitors to market their products as ITAR-free

or not requiring tough reviews required under the US

International Traffic in Arms Regulations (ITAR) law. Hirschhorn

added there has been more receptiveness among European

allies to buy parts that are under the Commerce Department's

jurisdiction. (Reuters)

ONS: UK inflation rises for first time in 10 months in April –

British inflation rose in April for the first time in 10 months, but as

the increase was partly due to a late Easter holiday, which

pushed up transport costs, it was unlikely to alter interest rate

expectations. Data from the Office for National Statistics (ONS)

showed that growth in house prices eased in March, potentially

tempering concerns about a bubble brewing in the property

market, although more up-to-date surveys have shown prices

are picking up again. ONS said the consumer price index rose

more than expected to an annual rate of 1.8% in April, from

1.6% in March, which had been its lowest level in four years. It

was the first rise in the CPI since June 2013, which was above a

Reuters poll forecast of 1.7% in April. (Reuters)

MoF: Japan’s export growth remains tepid, dims outlook –

Exports from Japan rose for the 14th straight month in April, but

shipments to the US slowed, underlining concerns that the

world's third-largest economy remains vulnerable to any fall in

external demand. Data from the Ministry of Finance (MoF)

showed that exports rose 5.1% in YTD-April 2014, as compared

to a 4.8% gain expected by economists and a 1.8% rise in

March. On a seasonally adjusted basis, exports rose a meager

0.6% in April from the previous month. With export growth below

last year's levels as the effect of a weaker yen wears off,

policymakers are becoming less confident of a lasting export

upturn that would cushion a dip in domestic spending after

Japan raised its sales tax to 8% from 5% on April 1, 2014.

Analysts say the Bank of Japan may act if the trade

4. Page 4 of 6

performance falls short – a side effect of many firms moving

production facilities offshore to escape the yen's strength.

(Reuters)

China employment situation stable in first four months –

The Chinese labor ministry said that employment in China was

basically stable in the first four months of 2014, with around

4.7mn new jobs created in cities. The ministry said that its

priority is to help new graduates find work. Beijing has

repeatedly stressed that employment is the first priority for the

government, and economists also say it is the top factor that

may trigger big-scale stimulus measures, if the economy

continues to lose momentum. (Reuters)

Regional

Kingdom to spend additional SR80bn on education – Saudi

Education Minister, Prince Khaled Al-Faisal, said that the

Kingdom will spend an additional SR80bn to overhaul the

country’s education system under a five-year plan. King

Abdullah approved the plan, which includes building 1,500

nursery schools, training about 25,000 teachers, and

establishing educational centers. Further, King Abdullah has

approved an executive plan for a public education development

project, which covers the provision of education through the

private sector, linking schools with a broadband internet system,

smart classrooms, computer systems for e-learning, setting up

specialized schools, support for clubs, construction of new

buildings, maintenance of existing schools, and enhancing

safety systems. (GulfBase.com)

WALAA appoints advisor to manage rights issue – Saudi

United Cooperative Insurance Company (WALAA) has assigned

Al Jazira Capital as the financial advisor to manage its offering

rights issue. (Tadawul)

UCA appoints advisor to manage rights issue – United

Cooperative Assurance Co. (UCA) has assigned BMG Financial

Group as the financial advisor to manage its offering rights

issue. (Tadawul)

Zamil Towers & Galvanizing wins SR120mn contract from

AETCON – Zamil Industrial Investment Company’s subsidiary,

Zamil Towers & Galvanizing Company Ltd., has been awarded a

contract worth SR120mn by the Arabian Electrical Transmission

Line Construction Company (AETCON). The contract is for

supply of lattice transmission line towers and gantries for the

380kV overhead transmission lines between Tabarjal Bulk

Supply Point (BSP) and Waad Al Shamaal BSP, as well as

between Qurayyat BSP and Waad Al-Shamaal BSP, owned by

the Saudi Electricity Company (SEC). The duration of the

contract is 16 months, with the company set to begin supply of

the towers and gantries in 3Q2014. (Tadawul)

Saudi CMA approves Bahri’s SR787.5mn capital increase –

Saudi CMA’s board has approved the National Shipping

Company of Saudi Arabia’s (Bahri) request to increase its

capital from SR3.15bn to SR3.94bn. The company intends to

use the proceeds to merge the fleet and operations of Vela

International Marine Ltd with itself. (Tadawul)

Al-Khodari Sons signs ICF agreement for SR300mn; renews

ICF deal with ARB – Abdullah A. M. Al-Khodari Sons Company

(Al-Khodari Sons) has signed an Islamic credit facilities (ICF)

agreement with Bank Al Bilad for SR300mn. 33% of the facilities

shall be utilized under Murabaha financing and 67% are for

multi-bonds and documentary credit till the expiry of credit

agreement, which may be renewed after March 29, 2015.

Similarly, Al-Khodari Sons signed a renewal of its Islamic credit

facilities agreement with Al Rajhi Bank (ARB) for SR245mn.

61% of the facilities shall be utilized under Murabaha financing

and 39% are for multi-bonds and documentary credit till their

expiry, which may be renewed after March 31, 2015. Both the

facilities are secured by promissory notes and assignment of the

contract proceeds of specific financed projects. The company

intends to use the proceeds for providing bonding commitments,

fund capital requirements, working capital and for general

corporate purposes. (Tadawul)

Saudi central bank sees gradual easing of inflation in

2Q2014 – Saudi's central bank is expecting the country’s annual

inflation rate to continue easing gradually in 2Q2014. Consumer

price growth in Saudi Arabia has been easing gradually since

hitting a peak of 4.0% in April 2013. It edged up marginally to

2.7% in April 2014 from 2.6% in March. (Reuters)

Saudi Aramco to build three new refineries – The Saudi

Arabian Oil Company (Saudi Aramco) is planning to build three

fully-transformative refineries at 400,000 bpd each. The

company is building the refineries in Jazan, Satorp, a JV with

Total, Yaserf, a JV with Sonic, in addition to building or

expanding two world-class chemical complexes: Sadara

complex, a JV with Daewoo Chemical and Petro Rabigh

complex, a JV with Somitomo Chemical. (GulfBase.com)

GS E&C wins $1.44bn UAE crude oil processing plant

contract – South Korea-based GS Engineering & Construction

Corporation (GS E&C) has won a $1.44bn contract for crude oil

processing plant in the UAE by forming a consortium with a local

partner. The third phase of the Rumaitha-Shanayel oil field

expansion project calls for GS E&C to build most of the facilities

related to oil processing, with its partner Dodsal to handle the

design and construction of the oil & gas pipelines and support

facilities. GS E&C will hold a 51% stake, while the remaining

stake will be held by Dodsal. GS E&C share of the project,

ordered by the Abu Dhabi Company for Onshore Oil Operations,

stands at $730mn. (Bloomberg)

Etisalat bids for minority stakes in Maroc Telecom –

Emirates Telecommunications Corporation (Etisalat) has made

a full bid for minority shareholdings in Maroc Telecom. Etisalat

had recently bought Vivendi’s 53% stake in Maroc Telecom for

€4.14bn. Further, the company has agreed to sell its operations

in several West African countries to Maroc Telecom for $650mn

in a move to unify its African units. (Reuters)

Emirates GBC signs SLA with DCL – Emirates Green Building

Council (Emirates GBC) has signed a service level agreement

(SLA) with the Dubai Central Laboratory (DCL) for testing of

green building materials and products. As per the agreement,

DCL will perform the required tests and certify the products and

materials of Emirates GBC’s members as per international

standards. (GulfBase.com)

ADPC Marine Services moves entire fleet to Tasneef – Abu

Dhabi Ports Company (ADPC) has moved its entire fleet of tug

boats operated by its subsidiary ADPC Marine Services to the

UAE’s classification society, Tasneef. The new contracts will

cover each vessel for five years and will give Tasneef the

authority to inspect the vessels for adherence to international

accredited technical standards. Tasneef will carry out regular

surveys of vessels to ensure continuing compliance.

(GulfBase.com)

ADIB signs preliminary deal in $2bn Amlak debt overhaul –

Abu Dhabi Islamic Bank (ADIB) has signed a tentative

agreement for $2bn debt overhaul with mortgage company,

Amlak Finance. The prospective accord includes a temporary

waiver on a certain part of the principal. ADIB is a part of a six-

member creditor committee negotiating Amlak’s debt

restructuring. The committee, chaired by Emirates NBD,

5. Page 5 of 6

includes Standard Chartered, Dubai Islamic Bank, Dubai’s

Department of Finance and the National Bonds Corp.

(Bloomberg)

Al Batinah Power, Al Suwadi Power IPOs open – Al Batinah

Power Company and Al Suwadi Power Company have

announced the opening of their IPOs for subscription in Oman,

which will culminate with a listing of their respective shares on

the Muscat Securities Market. The founding shareholders are

selling these shares to the public to comply with their obligations

in project founders’ agreements signed with government-owned

Electricity Holding Company in 2010. Their IPOs, which opened

on May 11, 2014, will close on June 09, 2014. It is open for both

Omani and non-Omani investors. (Bloomberg)

CBO approves stake raising requests from Omnivest, OHTC

– The Central Bank of Oman (CBO) has approved Oman

International Development & Investment Company’s (Omnivest)

request to increase its stake in the National Finance Company

from 24.22% to 35%. Additionally, CBO has approved Oman

Hotels & Tourism Company’s (OHTC) application to raise its

holding in the United Finance Company from 20.44% to 35%.

Further, the CBO’s board approved an application of finance

companies to allow them to extend finance for building

warehouses. (Bloomberg)

CBO: Omani banks can withstand severe shocks – The

Central Bank of Oman (CBO) said Omani banks have enough

capital to withstand the impact of severe shocks to the country’s

economy, after conducting stress tests on the banking system.

Oman, which pegs its rial to the US dollar, has a conservative

approach to financial regulation and many banks operating in

the country are mainly focused on the Sultanate or the Gulf

region, which limits exposure to external shocks. The country is

also grappling with rising pressure on its public finances after it

ramped up spending by more than 27% from 2011 to 2013,

mainly on welfare schemes and thousands of new state jobs.

(Peninsula Qatar)

GIB raises SR2bn with bond issue – Bahrain-based Gulf

International Bank (GIB) has announced the successful

completion of a senior unsecured SR2bn five-year floating rate

notes issuance. The notes were issued at a spread of 72.5 basis

points above three-month Saudi Arabia Interbank Offered Rate

(SAIBOR). The order book was more than 1.7 times

oversubscribed, reaching SR3.4bn. The joint lead managers and

book runners for the offering were GIB Capital, NCB Capital

Company, Samba Capital and the Investment Management

Company and Saudi Fransi Capital. (GulfBase.com)

Investcorp hires JPMorgan for Esmalglass sale – According

to sources, Investcorp Bank has hired JPMorgan Chase &

Company to sell Spanish ceramics-products maker, Esmalglass.

The transaction may value Esmalglass at about €800mn.

Investcorp’s preferred option is a sale to a private-equity firm or

another manufacturer, but there is also a possibility of an IPO. In

August 2012, Investcorp bought a majority stake in Esmalglass

from 3i Group in a deal valued at about €200mn. (Bloomberg)

ABG plans sukuk issues – Al Baraka Banking Group (ABG) is

planning to issue subordinated Islamic bonds through its South

African and Pakistani units to boost its regulatory capital.

(GulfBase.com)

6. Contacts

Saugata Sarkar Keith Whitney Sahbi Kasraoui

Head of Research Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

0.1%

(0.4%)

0.4%

(0.3%)

0.3%

(2.5%)

(4.1%)(4.8%)

(3.6%)

(2.4%)

(1.2%)

0.0%

1.2%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,294.37 0.1 0.1 7.4 DJ Industrial 16,374.31 (0.8) (0.7) (1.2)

Silver/Ounce 19.41 0.3 0.2 (0.3) S&P 500 1,872.83 (0.6) (0.3) 1.3

Crude Oil (Brent)/Barrel (FM

Future)

109.69 0.3 (0.1) (1.0) NASDAQ 100 4,096.89 (0.7) 0.2 (1.9)

Natural Gas (Henry

Hub)/MMBtu

4.52 0.2 2.2 4.1 STOXX 600 338.32 (0.1) (0.2) 3.1

LPG Propane (Arab Gulf)/Ton 102.75 1.0 2.4 (18.8) DAX 9,639.08 (0.2) 0.1 0.9

LPG Butane (Arab Gulf)/Ton 120.13 0.2 1.2 (11.5) FTSE 100 6,802.00 (0.6) (0.8) 0.8

Euro 1.37 (0.1) 0.1 (0.3) CAC 40 4,452.35 (0.4) (0.1) 3.6

Yen 101.33 (0.2) (0.2) (3.8) Nikkei 14,075.25 0.5 (0.2) (13.6)

GBP 1.68 0.1 0.2 1.7 MSCI EM 1,029.91 (0.5) (0.2) 2.7

CHF 1.12 0.0 0.1 0.1 SHANGHAI SE Composite 2,008.12 0.1 (0.9) (5.1)

AUD 0.92 (0.9) (1.3) 3.7 HANG SENG 22,834.68 0.6 0.5 (2.0)

USD Index 80.04 0.1 (0.0) 0.0 BSE SENSEX 24,376.88 0.1 1.1 15.1

RUB 34.52 (0.1) (0.7) 5.0 Bovespa 52,366.19 (1.8) (3.0) 1.7

BRL 0.45 (0.4) (0.1) 6.7 RTS 1,298.64 0.7 2.9 (10.0)

183.0

151.5

138.6