Downloaded 89 times

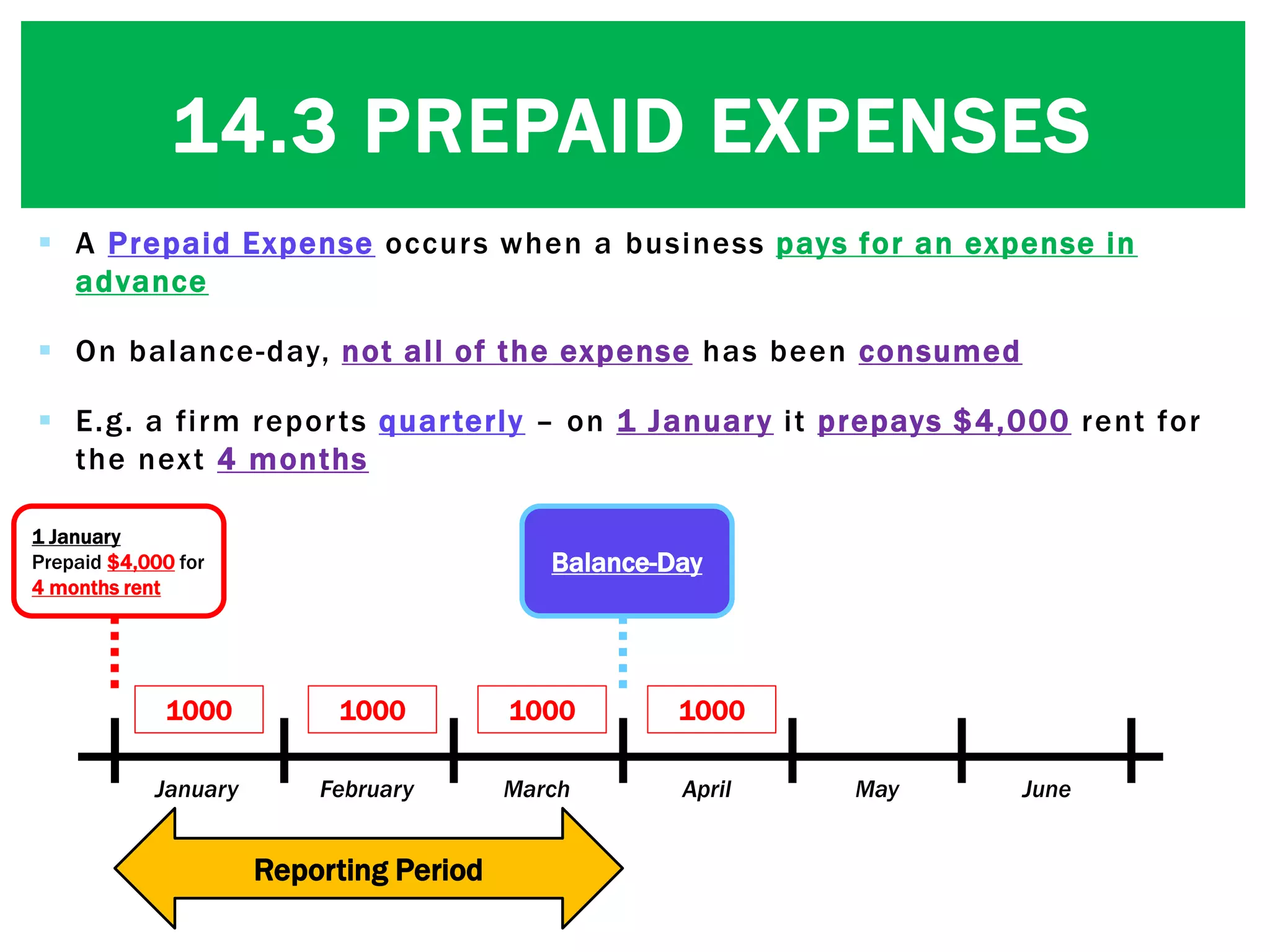

This document discusses prepaid expenses. It explains that a prepaid expense occurs when a business pays for an expense in advance, such as paying $4,000 rent for the next 4 months on January 1st. On the balance date, the prepaid amount is split between an expense and an asset. The expense is the amount that has been used, while the asset is the unused amount that will be applied to future periods. For example, on March 31st the business would report $3,000 as a rent expense and $1,000 as a prepaid rent asset on the balance sheet.