Downloaded 44 times

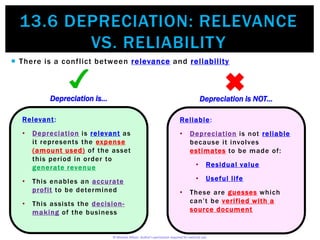

Depreciation is relevant because it represents the expense of using a fixed asset over a period to generate revenue, which allows an accurate profit to be determined and assists business decision making. However, depreciation is not fully reliable because it involves estimates of an asset's residual value and useful life that cannot be verified with documentation and are based on assumptions rather than facts. While depreciation provides useful information, its reliability is limited by the estimates and assumptions that go into calculating it.