Download as PDF, PPTX

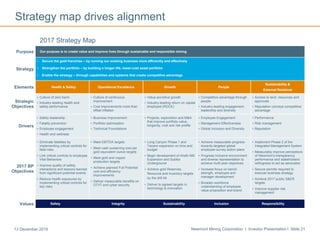

This document is an investor presentation from Newmont Mining Corporation dated December 13, 2016. It contains forward-looking statements regarding estimates and expectations of future production, costs, capital expenditures, profitability, and other metrics. It cautions that these statements are based on assumptions that may prove to be incorrect. The presentation provides an overview of Newmont's strategy to improve its underlying business, strengthen its portfolio, and create shareholder value. It summarizes recent performance results and updates to guidance. Newmont aims to maximize opportunities and manage risks across its global operations and projects.