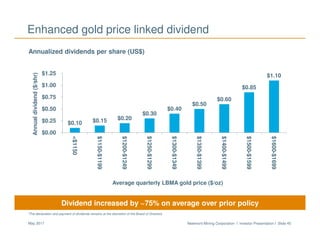

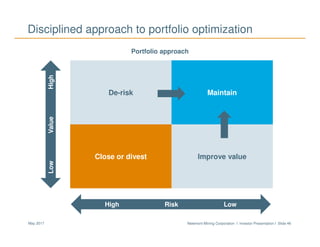

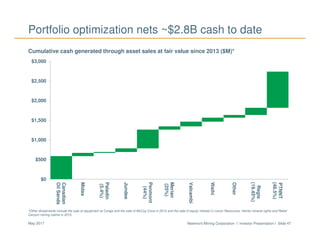

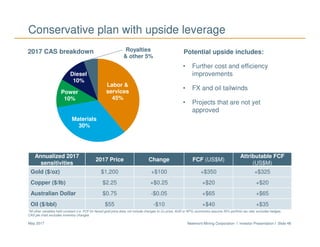

Download to read offline

This document provides a cautionary statement regarding forward-looking statements in Newmont Mining Corporation's investor presentation. It notes that estimates and expectations in the presentation are based on assumptions that may prove to be incorrect. It lists key assumptions including around geological, metallurgical and other conditions, permitting, development and expansion of operations, political stability, exchange rates, commodity prices, supply prices, mineral reserve and resource estimates, and other risks. The company does not undertake to publicly revise or update forward-looking statements except as required by law.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)