#1 Basic Cost Terms and Concepts Basic Cost Terms and Concepts.pptx

1.

Week 1

Basic CostTerms and Concepts

Cost and Investment Management

1

Laboratorium PSMI 2025

Departemen Teknik Sistem dan Industri

Institut Teknologi Sepuluh Nopember (ITS)

2.

Learning Objectives

1. Explainwhat is meant by the word cost.

2. Distinguish among product costs, period

costs, and expenses.

6

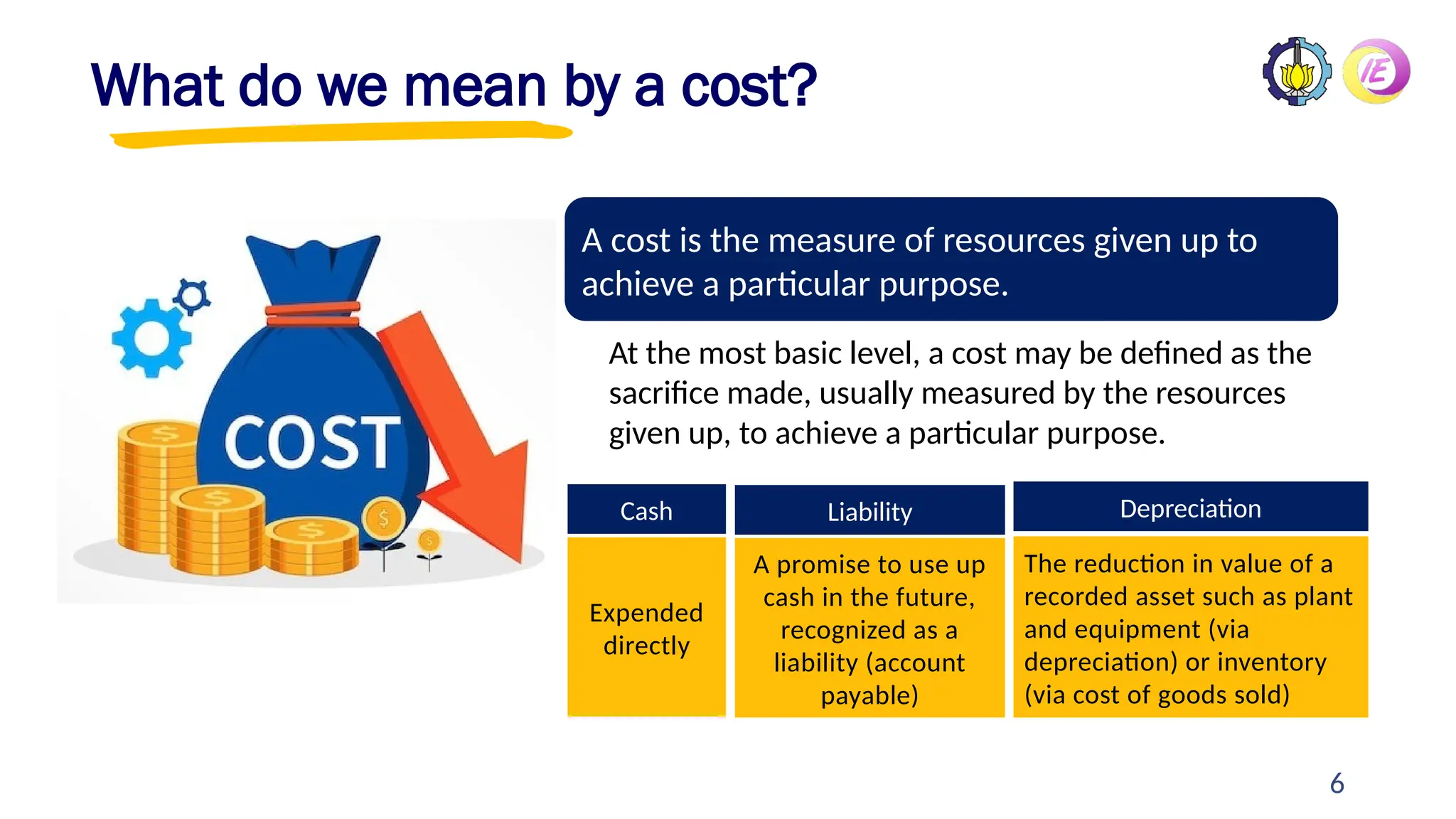

What do wemean by a cost?

At the most basic level, a cost may be defined as the

sacrifice made, usually measured by the resources

given up, to achieve a particular purpose.

A cost is the measure of resources given up to

achieve a particular purpose.

Expended

directly

The reduction in value of a

recorded asset such as plant

and equipment (via

depreciation) or inventory

(via cost of goods sold)

Cash Depreciation

A promise to use up

cash in the future,

recognized as a

liability (account

payable)

Liability

7.

9

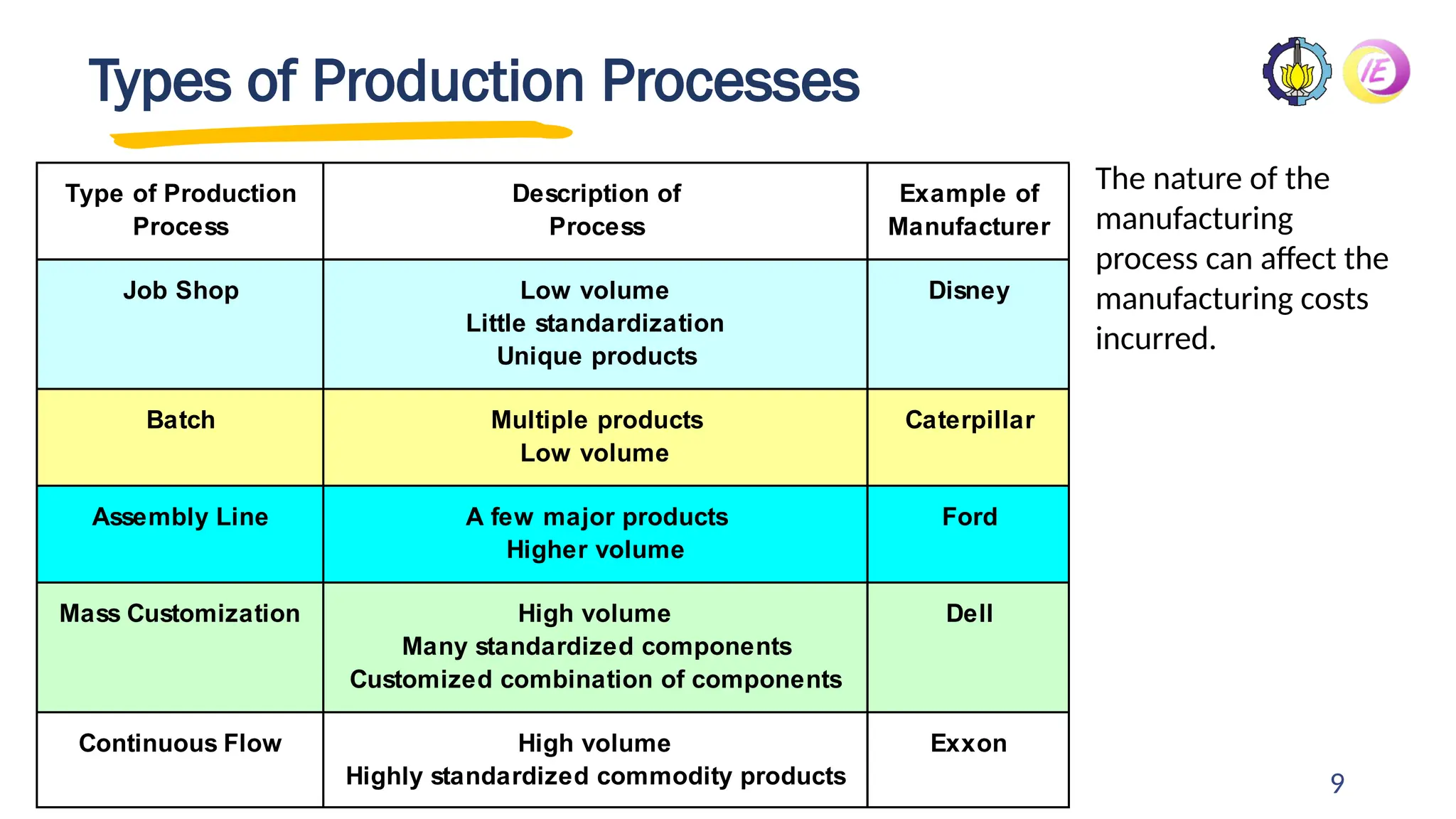

Types of ProductionProcesses

Type of Production Description of Example of

Process Process Manufacturer

Job Shop Low volume Disney

Little standardization

Unique products

Batch Multiple products Caterpillar

Low volume

Assembly Line A few major products Ford

Higher volume

Mass Customization High volume Dell

Many standardized components

Customized combination of components

Continuous Flow High volume Exxon

Highly standardized commodity products

The nature of the

manufacturing

process can affect the

manufacturing costs

incurred.

11

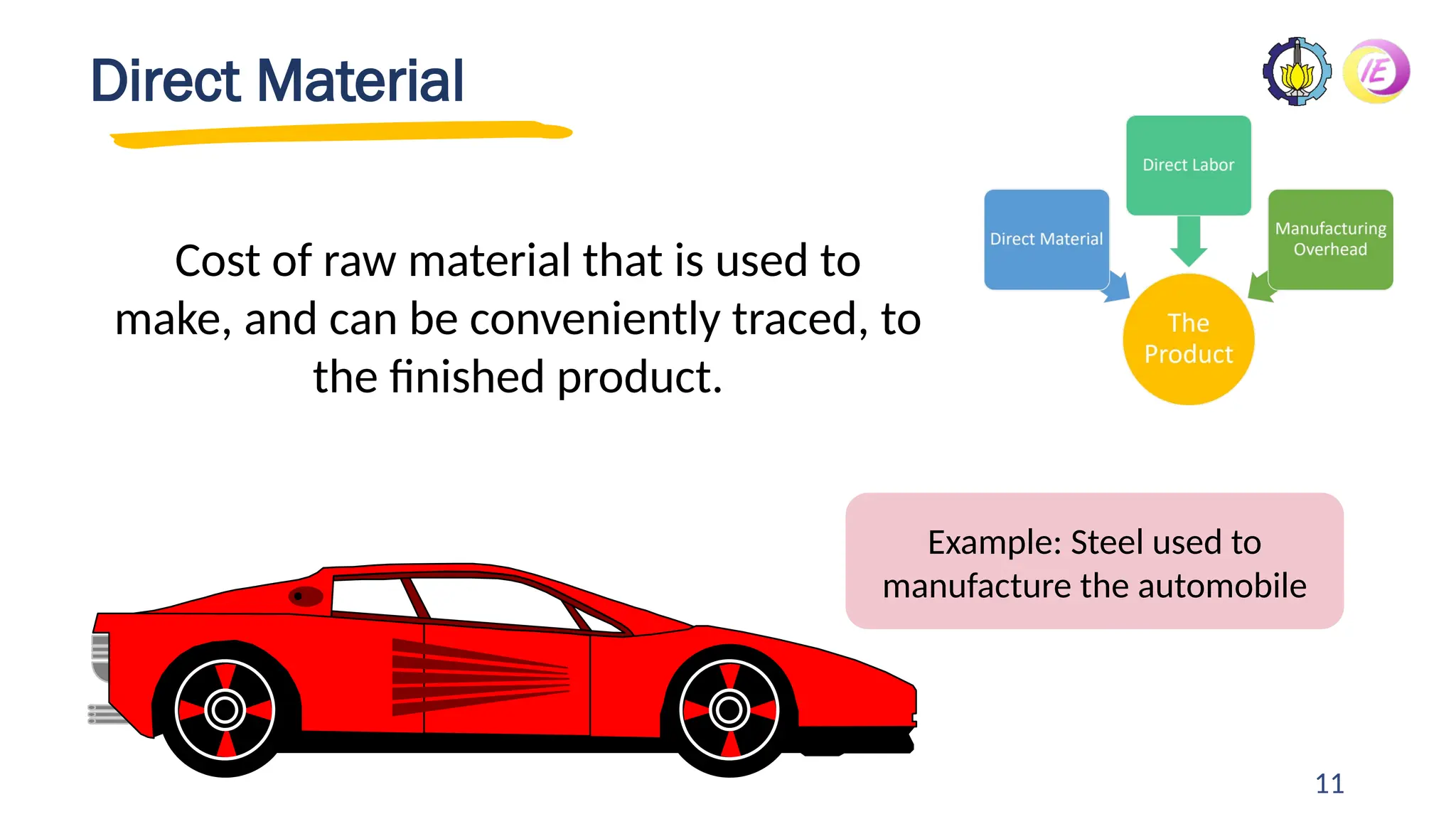

Direct Material

Cost ofraw material that is used to

make, and can be conveniently traced, to

the finished product.

Example: Steel used to

manufacture the automobile

10.

12

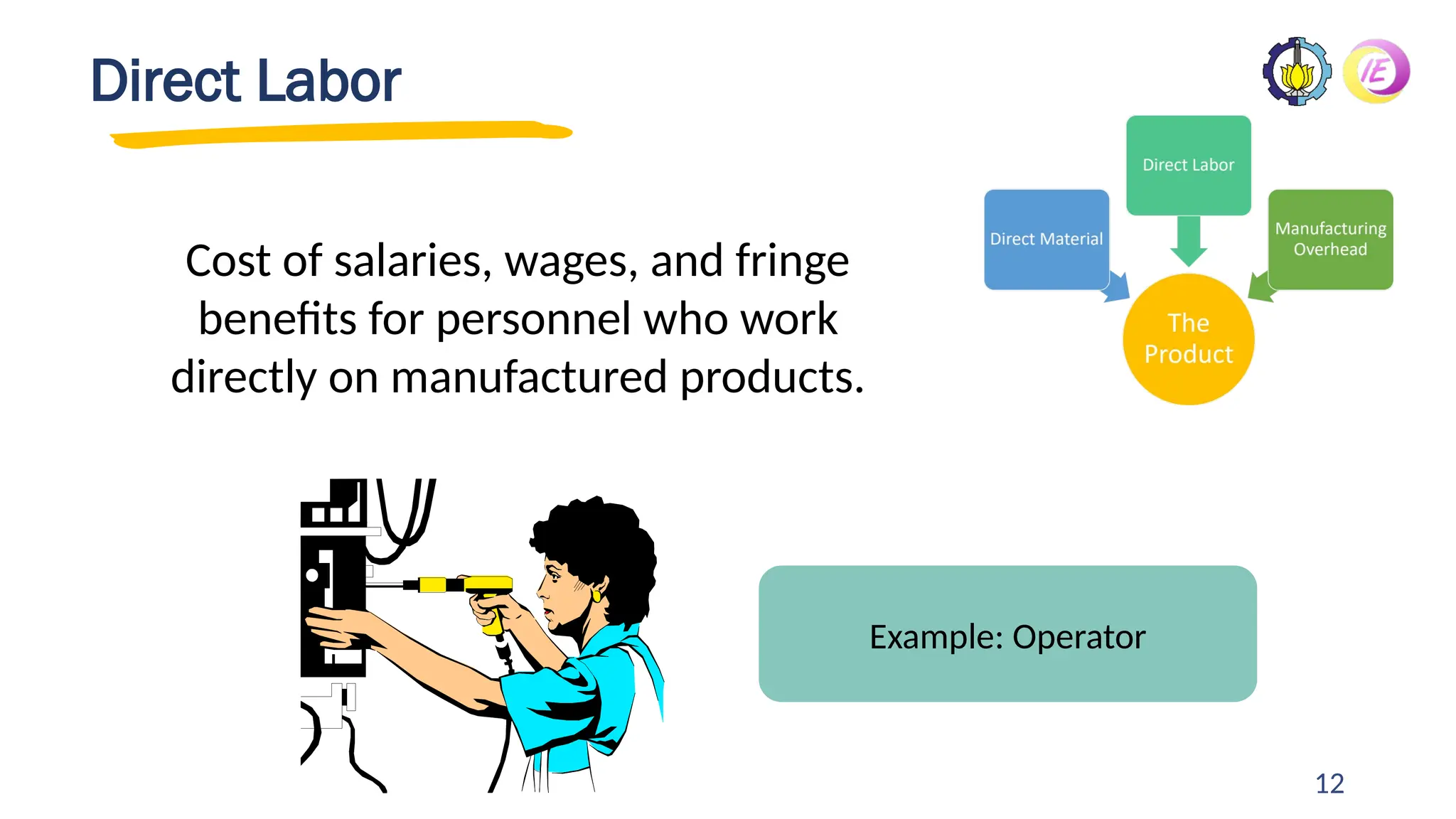

Direct Labor

Cost ofsalaries, wages, and fringe

benefits for personnel who work

directly on manufactured products.

Example: Operator

11.

13

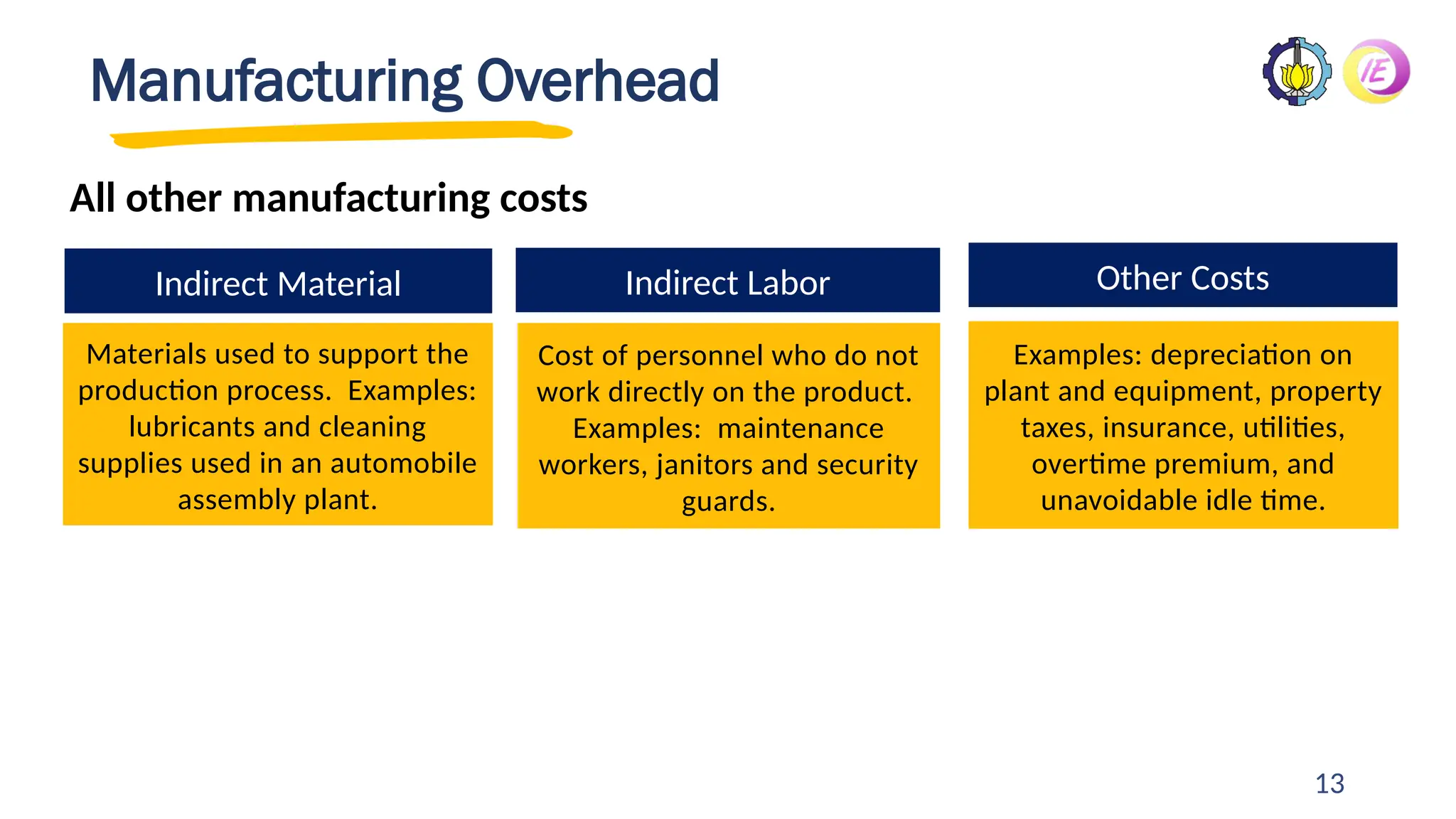

Manufacturing Overhead

All othermanufacturing costs

Materials used to support the

production process. Examples:

lubricants and cleaning

supplies used in an automobile

assembly plant.

Examples: depreciation on

plant and equipment, property

taxes, insurance, utilities,

overtime premium, and

unavoidable idle time.

Indirect Material Other Costs

Cost of personnel who do not

work directly on the product.

Examples: maintenance

workers, janitors and security

guards.

Indirect Labor

12.

14

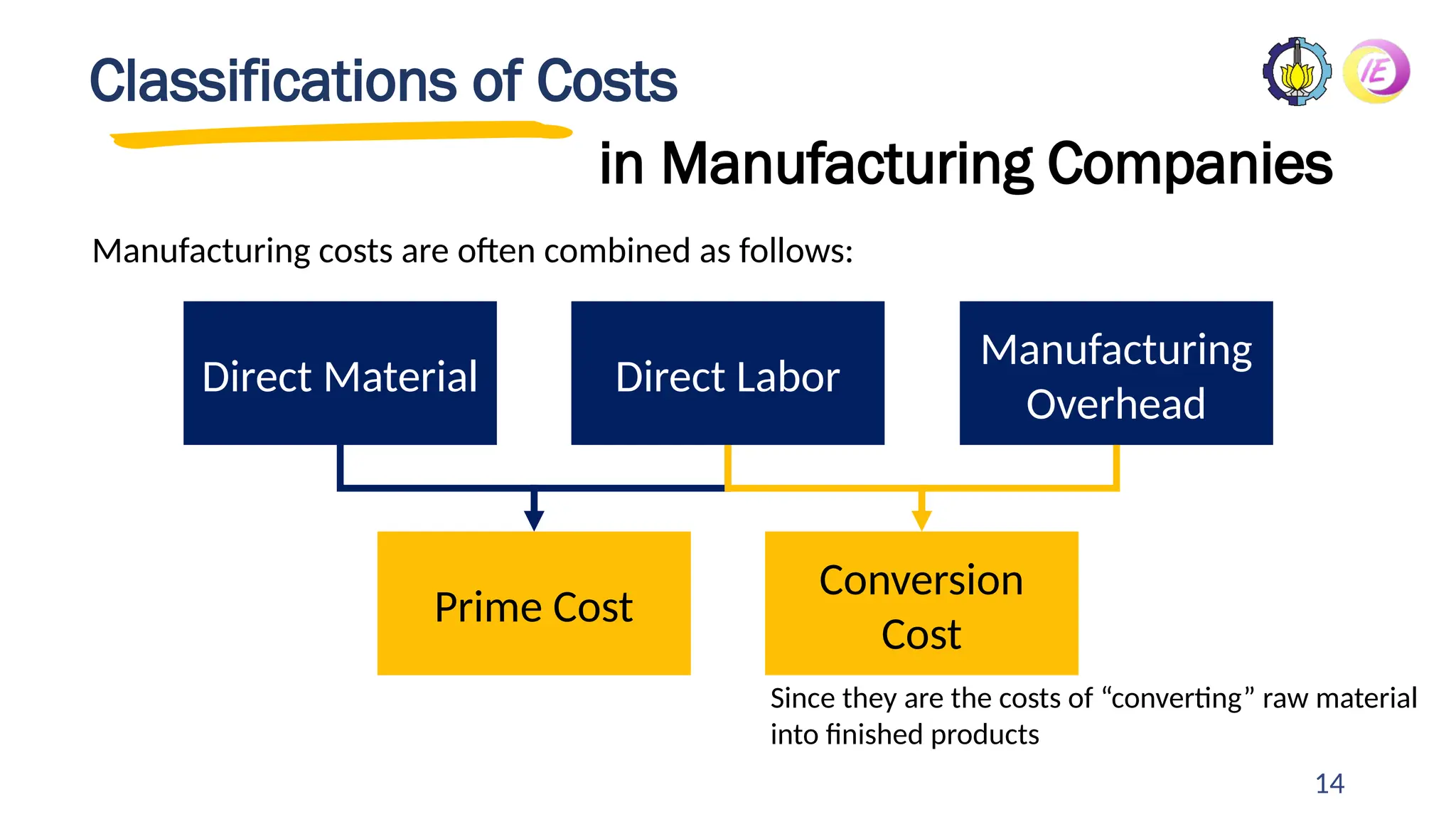

Classifications of Costs

inManufacturing Companies

Manufacturing costs are often combined as follows:

Direct Material Direct Labor

Manufacturing

Overhead

Prime Cost

Conversion

Cost

Since they are the costs of “converting” raw material

into finished products

13.

15

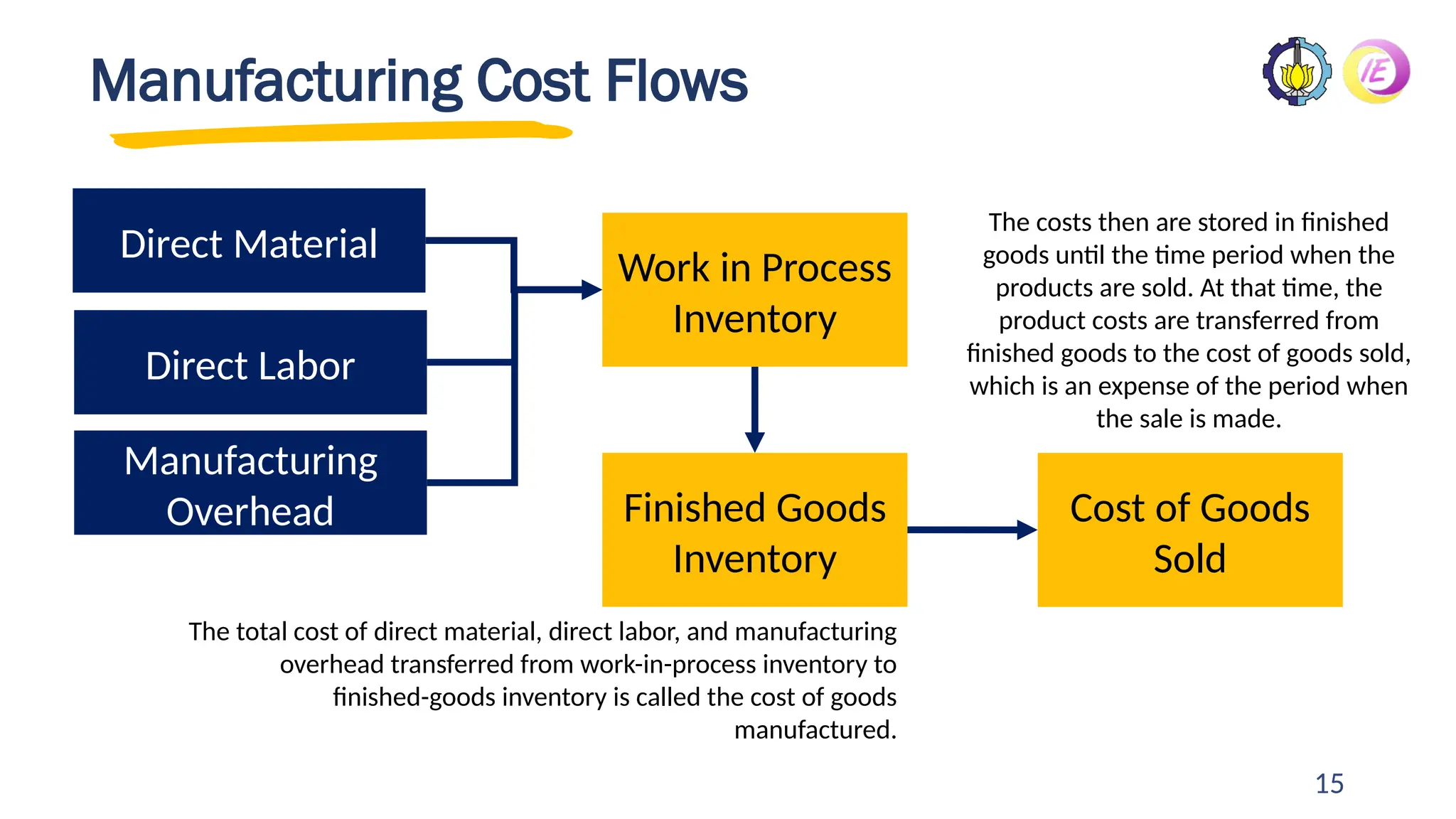

Manufacturing Cost Flows

Workin Process

Inventory

Direct Material

Direct Labor

Manufacturing

Overhead Finished Goods

Inventory

Cost of Goods

Sold

The total cost of direct material, direct labor, and manufacturing

overhead transferred from work-in-process inventory to

finished-goods inventory is called the cost of goods

manufactured.

The costs then are stored in finished

goods until the time period when the

products are sold. At that time, the

product costs are transferred from

finished goods to the cost of goods sold,

which is an expense of the period when

the sale is made.

14.

16

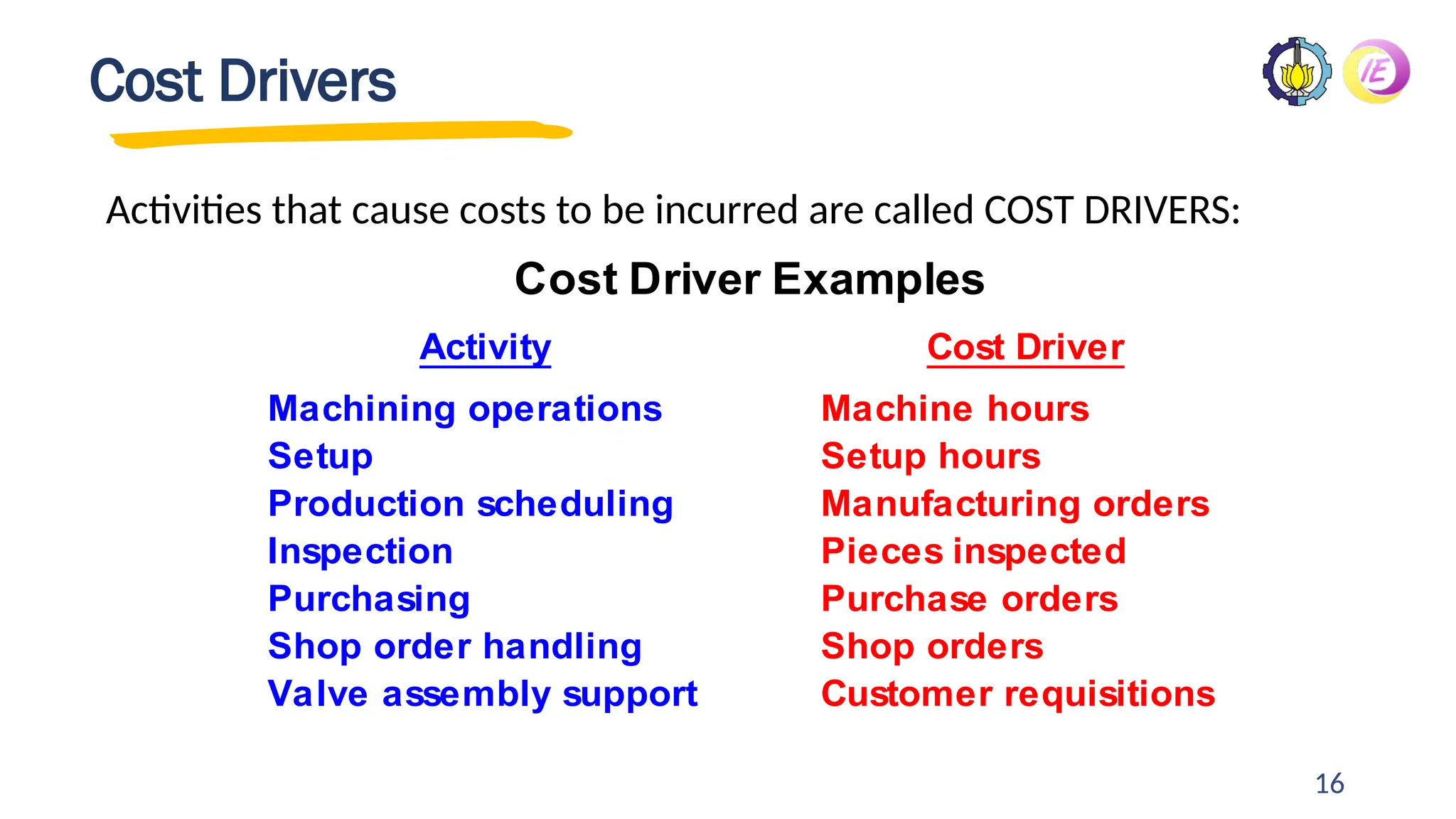

Cost Drivers

Activities thatcause costs to be incurred are called COST DRIVERS:

Cost Driver Examples

Activity Cost Driver

Machining operations Machine hours

Setup Setup hours

Production scheduling Manufacturing orders

Inspection Pieces inspected

Purchasing Purchase orders

Shop order handling Shop orders

Valve assembly support Customer requisitions

15.

17

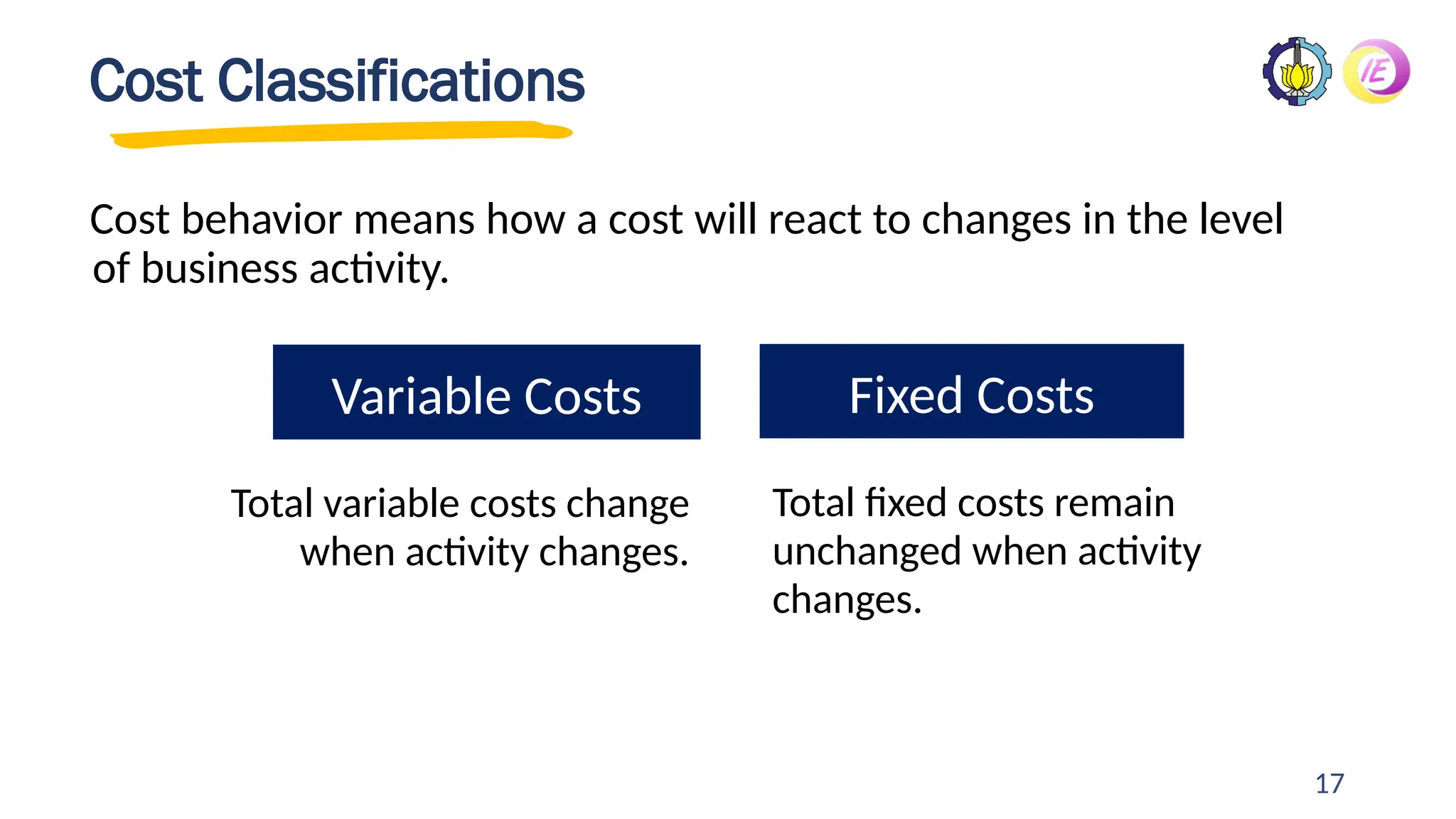

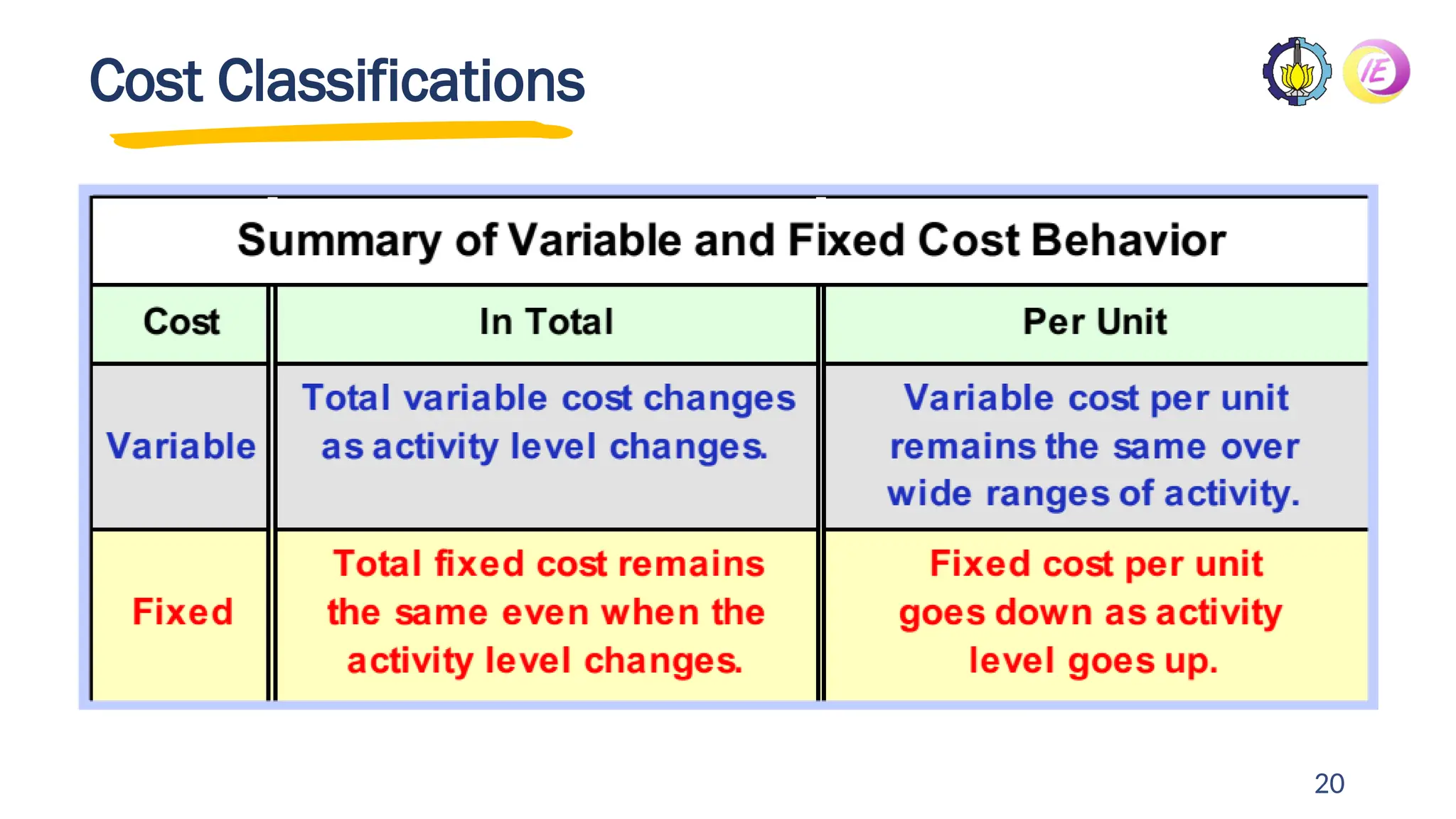

Cost Classifications

Cost behaviormeans how a cost will react to changes in the level

of business activity.

Variable Costs Fixed Costs

Total variable costs change

when activity changes.

Total fixed costs remain

unchanged when activity

changes.

16.

18

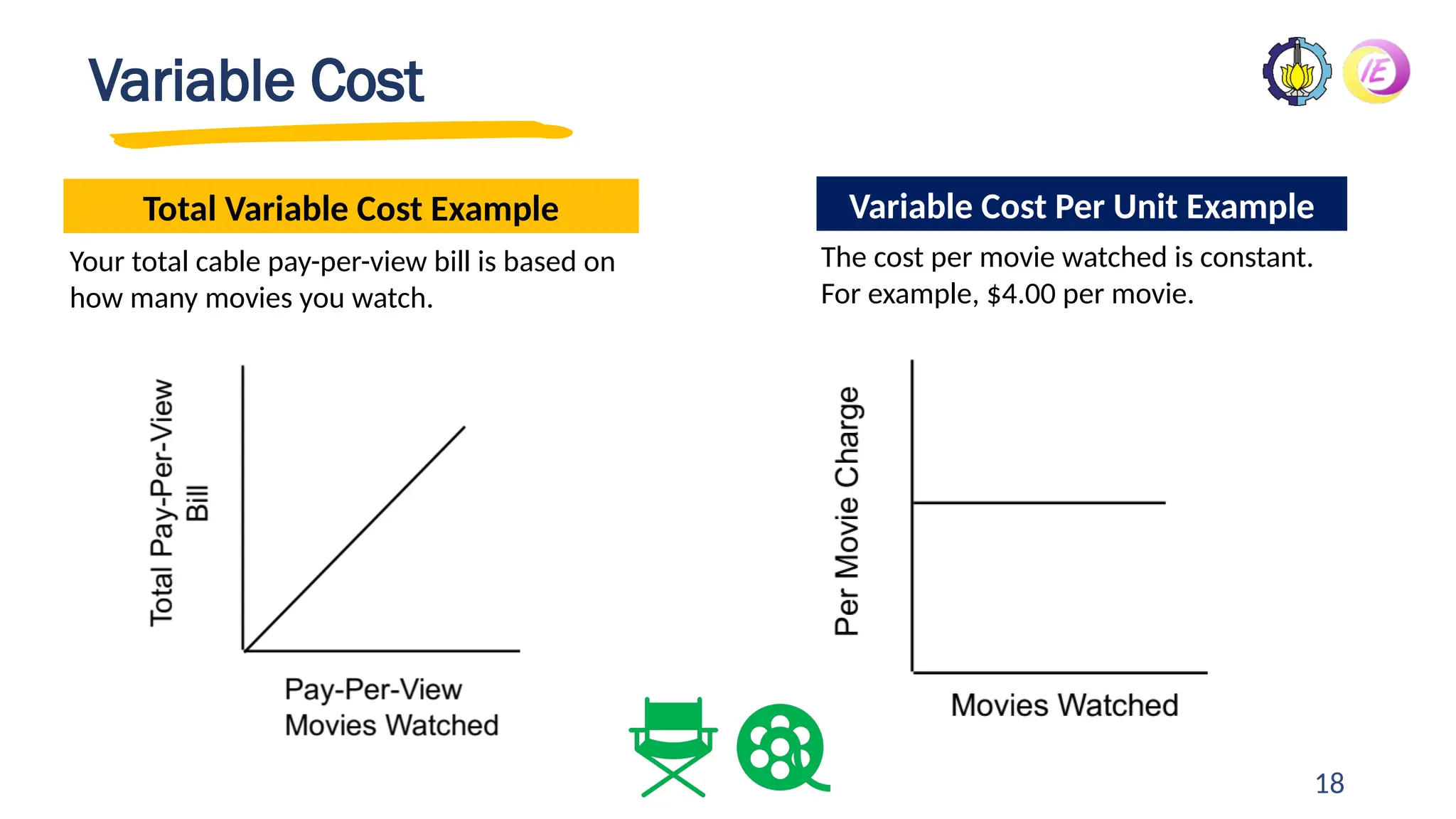

Variable Cost

Your totalcable pay-per-view bill is based on

how many movies you watch.

The cost per movie watched is constant.

For example, $4.00 per movie.

Total Variable Cost Example Variable Cost Per Unit Example

17.

19

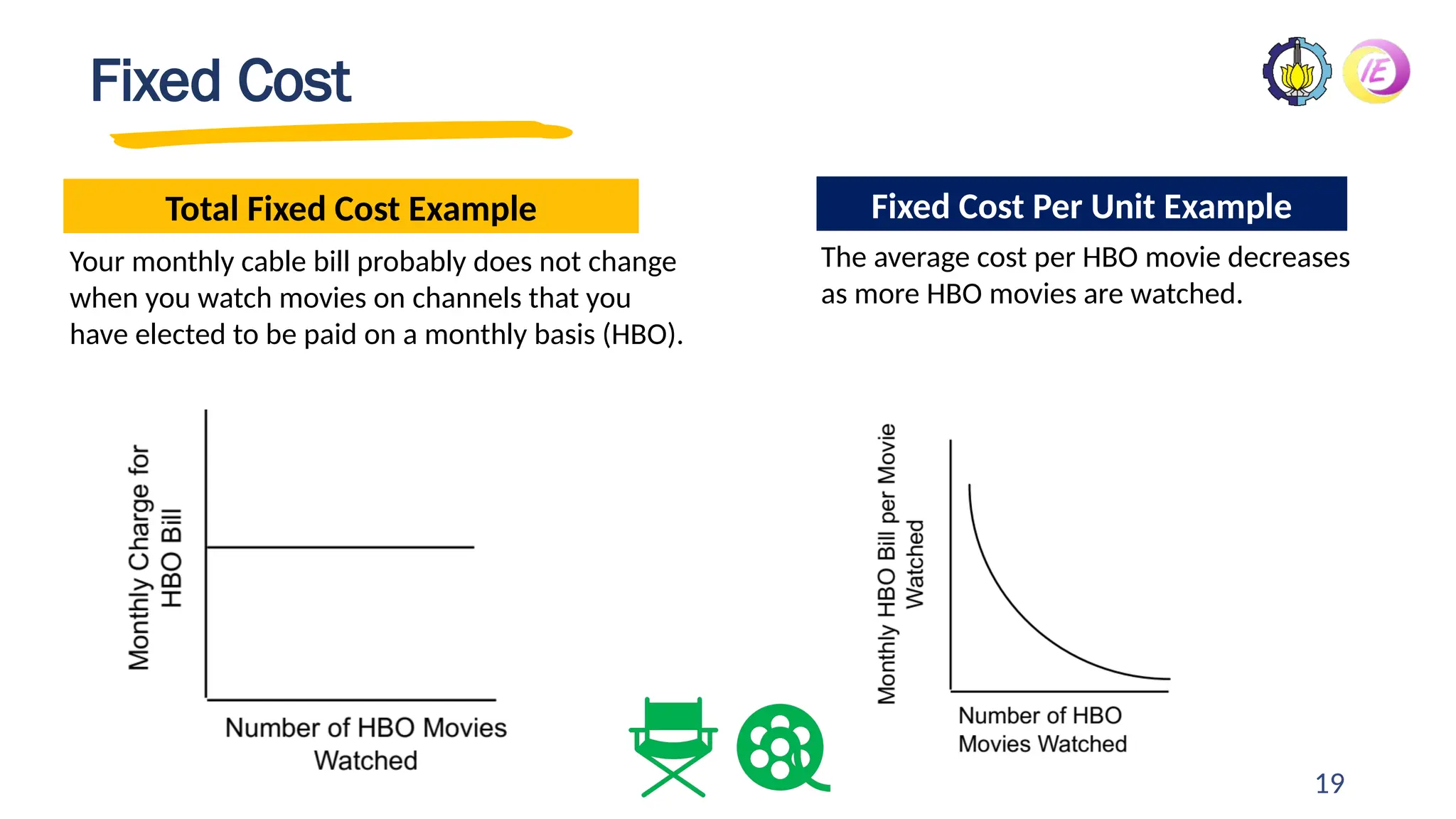

Fixed Cost

Your monthlycable bill probably does not change

when you watch movies on channels that you

have elected to be paid on a monthly basis (HBO).

The average cost per HBO movie decreases

as more HBO movies are watched.

Total Fixed Cost Example Fixed Cost Per Unit Example

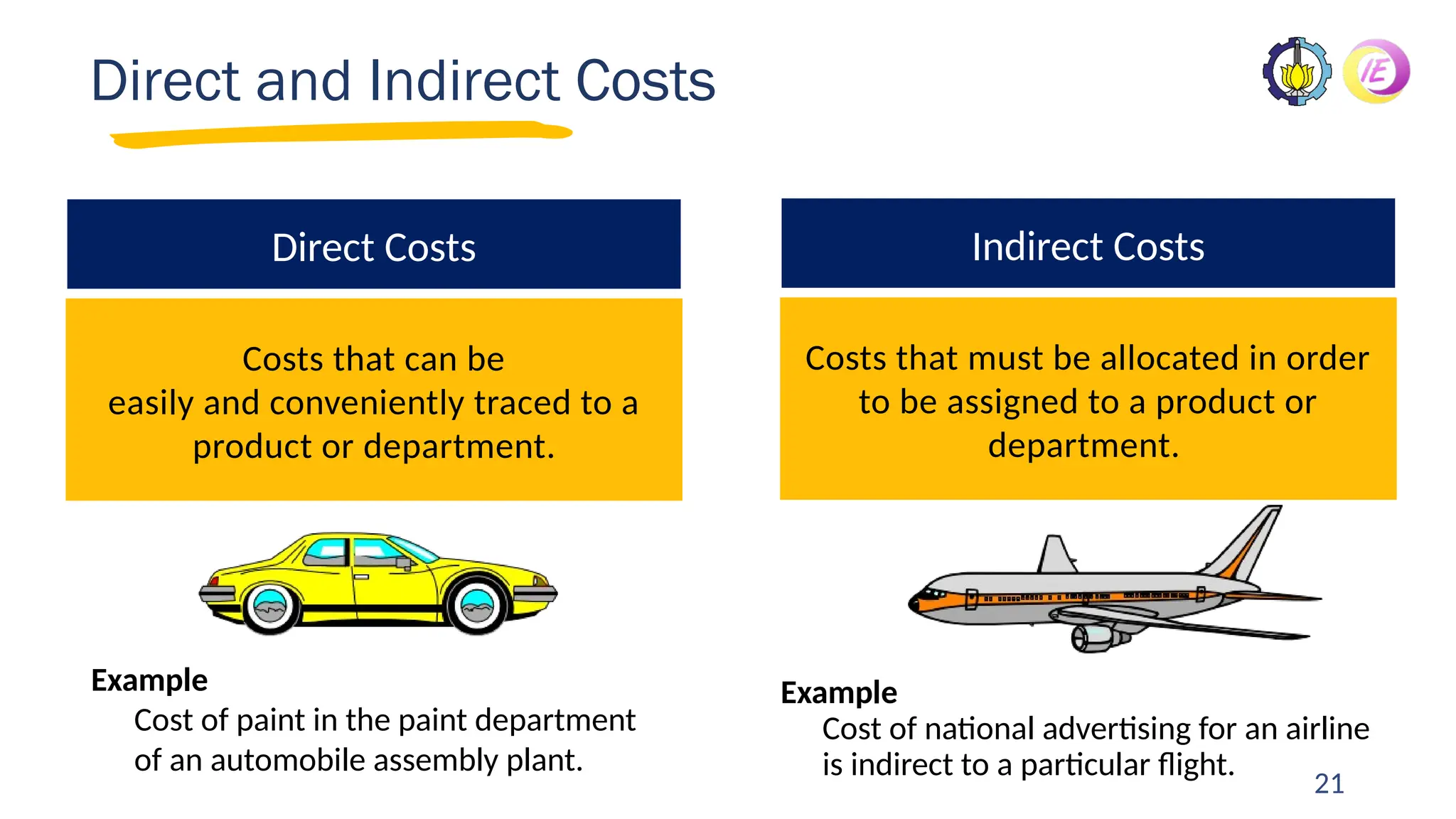

21

Example

Cost of nationaladvertising for an airline

is indirect to a particular flight.

Direct and Indirect Costs

Costs that can be

easily and conveniently traced to a

product or department.

Direct Costs

Costs that must be allocated in order

to be assigned to a product or

department.

Indirect Costs

Example

Cost of paint in the paint department

of an automobile assembly plant.

23

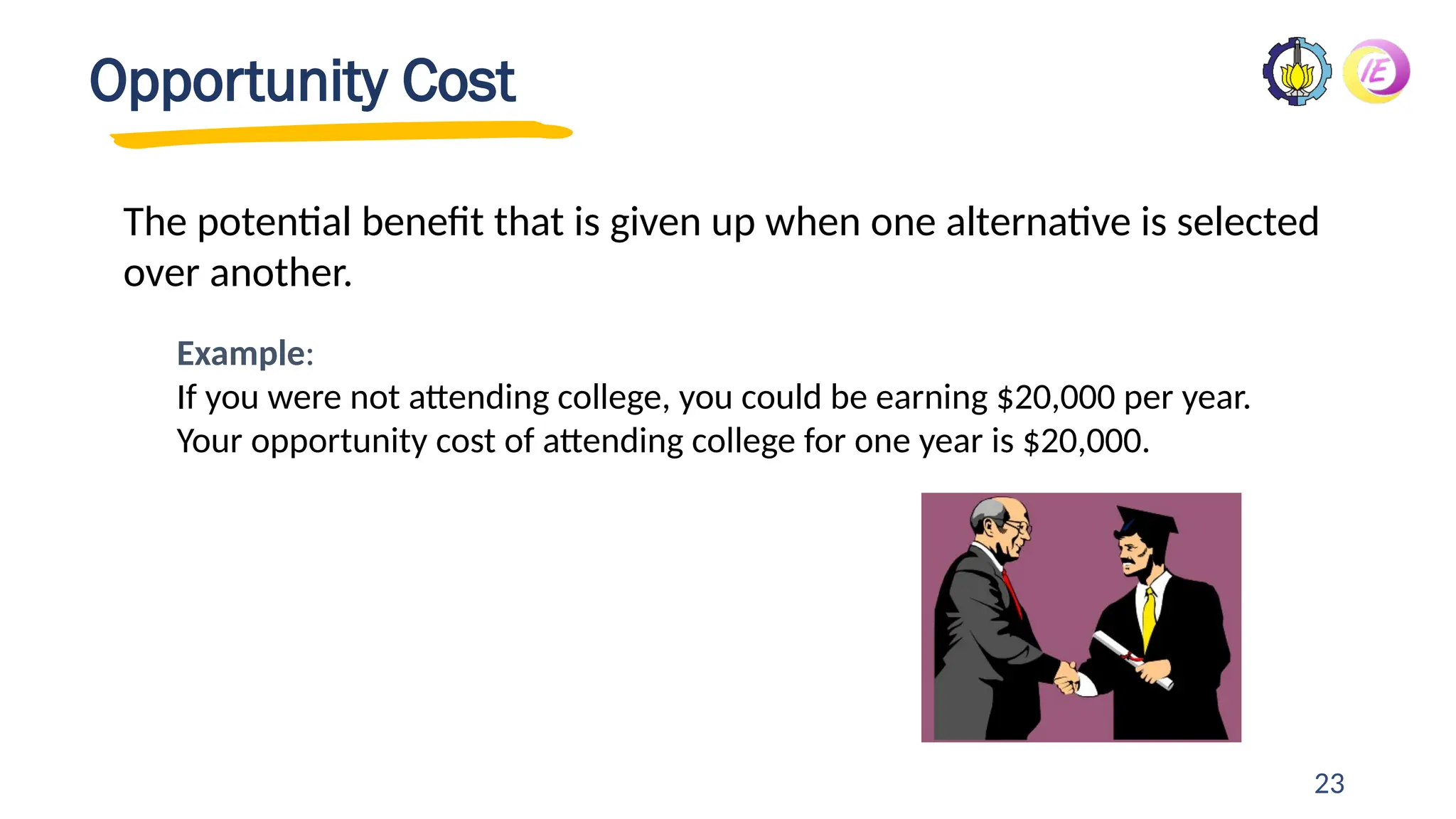

Opportunity Cost

The potentialbenefit that is given up when one alternative is selected

over another.

Example:

If you were not attending college, you could be earning $20,000 per year.

Your opportunity cost of attending college for one year is $20,000.

22.

Sunk Costs

All costsincurred in the past that cannot be changed by

any decision made now or in the future are sunk costs.

Sunk costs should not be considered in decisions.

• Example: You bought an automobile that cost $12,000 two years

ago. The $12,000 cost is sunk because whether you drive it, park it,

trade it, or sell it, you cannot change the $12,000 cost.

2-24

23.

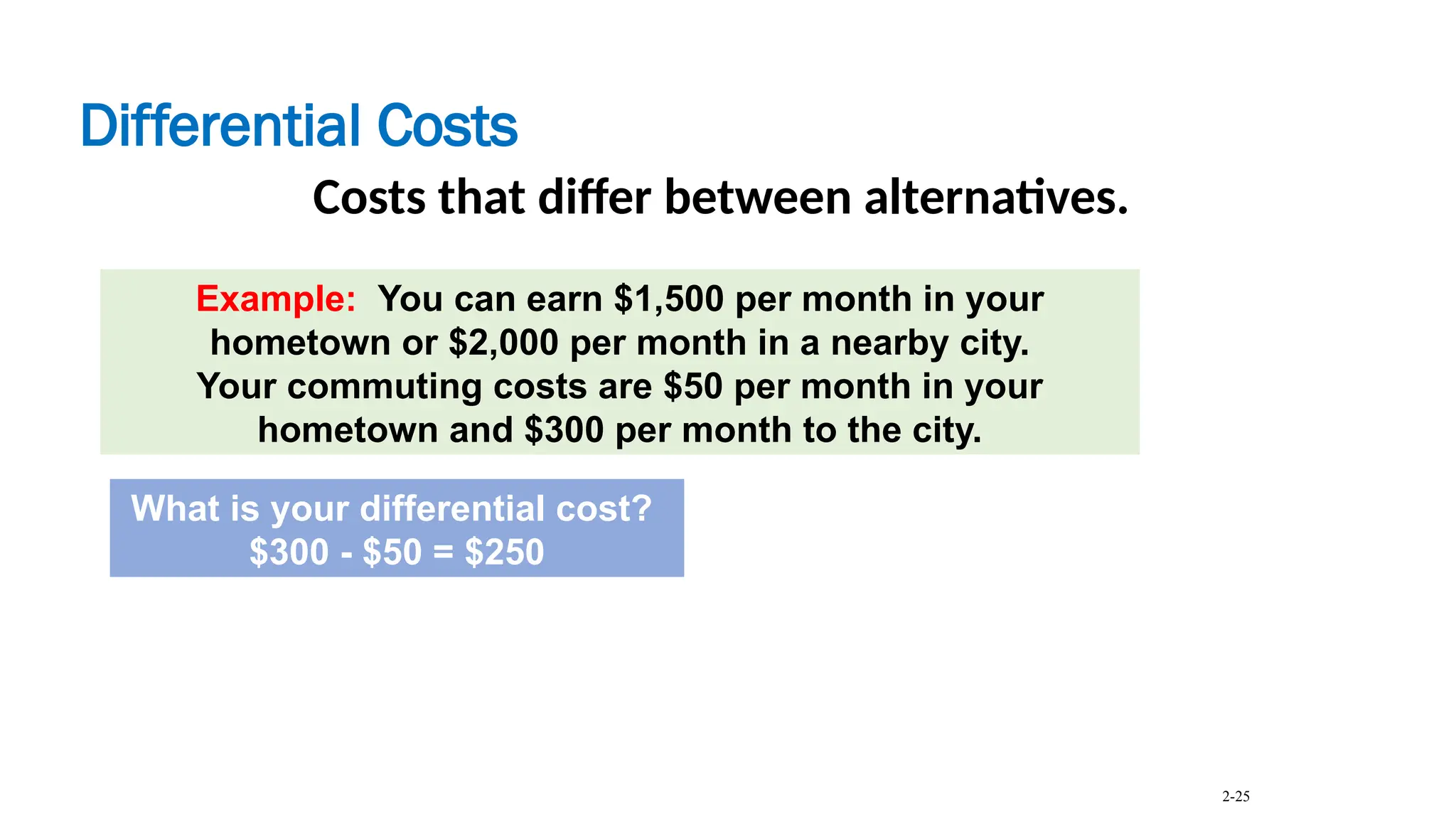

Differential Costs

Costs thatdiffer between alternatives.

Example: You can earn $1,500 per month in your

hometown or $2,000 per month in a nearby city.

Your commuting costs are $50 per month in your

hometown and $300 per month to the city.

What is your differential cost?

$300 - $50 = $250

2-25

24.

Marginal Costs andAverage Costs

The extra cost

incurred to produce

one additional unit.

The total cost to

produce a quantity

divided by the

quantity produced.

Marginal and average costs are

largely a function of cost behavior

-- variable and fixed costs.

2-26

25.

Costs and Benefitsof Information

Costs Benefits

More information does not mean more

benefits if information overload results.

2-27

• Another important task of the

managerial accountant is to weigh

the benefits of providing

information against the costs of

generating, communicating, and

using that information.

• When managers receive more data

than they can utilize effectively,

information overload occurs.

• In deciding how much and what

type of information to provide,

managerial accountants should

consider these human limitations.

Editor's Notes

#9 Production processes can be classified into five generic types. The nature of the manufacturing process can affect the manufacturing costs incurred. The management team is in a better position to control these costs if the relationship of the production process to the types of costs incurred is understood. (LO4)

#15 As direct material is consumed in production, its cost is added to work-in-process inventory. Similarly, the costs of direct labor and manufacturing overhead are accumulated in work in process. (LO5)

When products are finished, their costs are transferred from work-in-process inventory to finished-goods inventory. The total cost of direct material, direct labor, and manufacturing overhead transferred from work-in-process inventory to finished-goods inventory is called the cost of goods manufactured. (LO5)

The costs then are stored in finished goods until the time period when the products are sold. At that time, the product costs are transferred from finished goods to cost of goods sold, which is an expense of the period when the sale is made.

#24 Sunk costs are costs that have been incurred in the past. Consequently, they do not affect future costs and cannot be changed by any current or future action. (LO10)

#25 A differential cost is the amount by which the cost differs under two alternative actions. (LO10)

#26 A special case of the differential-cost concept is the marginal cost, which is the extra cost incurred when one additional unit is produced. Marginal costs typically differ across different ranges of production quantities because the efficiency of the production process changes. (LO10)

#27 Another important task of the managerial accountant is to weigh the benefits of providing information against the costs of generating, communicating, and using that information. When managers receive more data than they can utilize effectively, information overload occurs. In deciding how much and what type of information to provide, managerial accountants should consider these human limitations. (LO10)