Downloaded 97 times

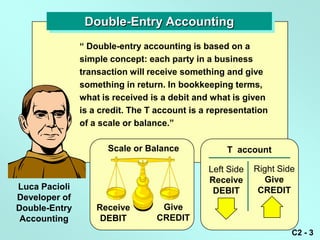

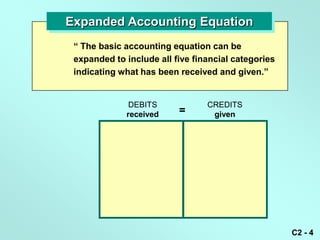

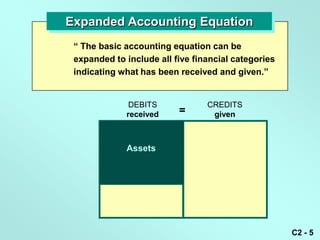

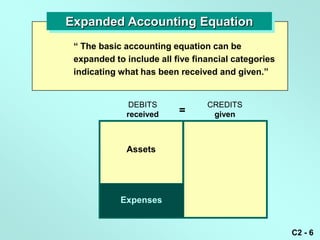

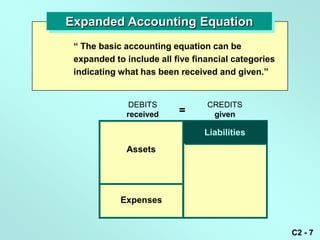

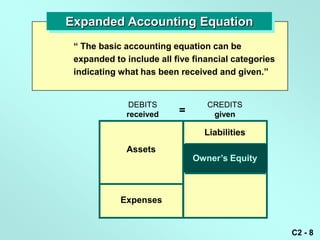

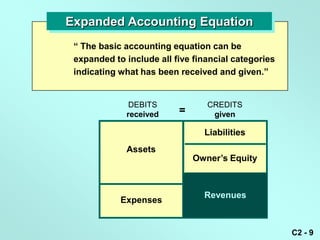

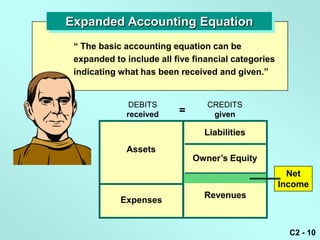

The document provides an overview of analyzing transactions in accounting. It discusses key concepts like the double-entry accounting system where every transaction has a debit and credit recorded, and how this is represented with T-accounts. It also shows how the basic accounting equation can be expanded to include the five main financial categories of assets, liabilities, equity, revenues and expenses. An example is then provided of recording business transactions for a sole proprietorship using double-entry accounting.