BUT, SERIOUSLY. DON'TSWEAT IT.

I KNOW WHAT

YOU ARE

SAYING…

OH GOD.

ANYTHING

BUT FINANCE.

6.

BUT, SERIOUSLY. DON'TSWEAT IT.

I KNOW WHAT

YOU ARE

SAYING…

OH GOD.

ANYTHING

BUT FINANCE.

FINANCE IS ACTUALLY QUITE SIMPLE

7.

BUT, SERIOUSLY. DON'TSWEAT IT.

I KNOW WHAT

YOU ARE

SAYING…

OH GOD.

ANYTHING

BUT FINANCE.

FINANCE IS ACTUALLY QUITE SIMPLE

WHEN YOU FOCUS ON WHAT MATTERS.

SO LET'S TALKABOUT VALUATION

SINCEYOUCAN’T

AVOIDIT

SINCE IT'S NOT ACTUALLY

THAT HARD

15.

SO LET'S TALKABOUT VALUATION

SINCE IT'S NOT ACTUALLY

THAT HARD

AND SINCE IT IS ONE OF

THOSE TOPICS THAT

ABSATIVELY CANNOT BE

DELEGATED TO FINANCE

SINCEYOUCAN’T

AVOIDIT

DEFINITION VALUATION IS

THEPROCESS OF

DEFINING WHAT

YOUR START-UP

IS WORTH!

YOU DO THAT IN 3 SIMPLE WAYS

YOU'RE WORTH WHAT YOU

OWN

19.

DEFINITION VALUATION IS

THEPROCESS OF

DEFINING WHAT

YOUR START-UP

IS WORTH!

YOU DO THAT IN 3 SIMPLE WAYS

YOU'RE WORTH WHAT YOU

OWN

YOU'RE WORTH WHAT YOU

CAN EARN IN THE FUTURE

20.

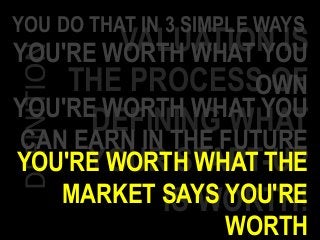

DEFINITION VALUATION IS

THEPROCESS OF

DEFINING WHAT

YOUR START-UP

IS WORTH!

YOU DO THAT IN 3 SIMPLE WAYS

YOU'RE WORTH WHAT YOU

OWN

YOU'RE WORTH WHAT YOU

CAN EARN IN THE FUTURE

YOU'RE WORTH WHAT THE

MARKET SAYS YOU'RE

WORTH

VALUATION BASED ONACTUAL

ASSETS IS PROBABLY THE SIMPLEST

AND MOST INTUITIVE

24.

YOU ARE WORTHEXACTLY HOW MUCH

YOU HAVE IN YOUR POCKET!

* (ADVANCED READER: WHAT IS IN YOUR BALANCE SHEET TODAY?)

25.

ACTUALLY, WHAT YOU’REWORTH

RIGHT NOW CAN BE DIVIDED INTO 2

MAJOR CATEGORIES OF VALUE

26.

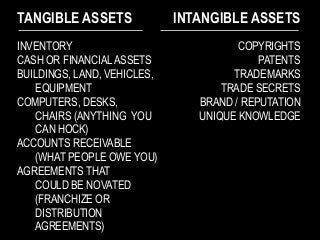

TANGIBLE ASSETS INTANGIBLEASSETS

INVENTORY

CASH OR FINANCIALASSETS

BUILDINGS, LAND, VEHICLES,

EQUIPMENT

COMPUTERS, DESKS,

CHAIRS (ANYTHING YOU

CAN HOCK)

ACCOUNTS RECEIVABLE

(WHAT PEOPLE OWE YOU)

AGREEMENTS THAT

COULD BE NOVATED

(FRANCHIZE OR

DISTRIBUTION

AGREEMENTS)

COPYRIGHTS

PATENTS

TRADEMARKS

TRADE SECRETS

BRAND / REPUTATION

UNIQUE KNOWLEDGE

27.

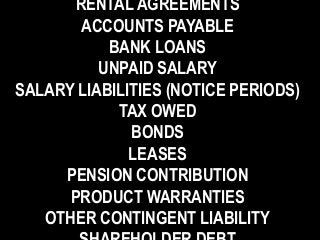

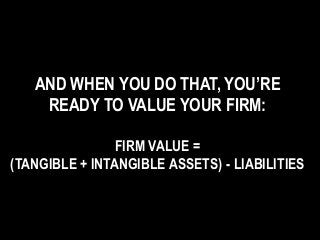

SO THE FIRSTTHING YOU NEED TO DO

IS FIGURE OUT HOW MUCH YOU CAN

SELL ALL THE TANGIBLE & INTANGIBLE

ASSETS FOR

FORTUNATELY, AN ARMYOF

MATHEMATICIANS WORKED THEIR

MAGIC AND CAME UP WITH A COUPLE

OF NIFTY FORMULAS

66.

INTERNAL RATE OFRETURN (IRR)

AND

NET PRESENT VALUE (NPV)

(ACTUALLY, IT’S REALLY THE SAME FORMULA, JUST SOLVED FORWARDS AND

BACKWARDS)

67.

THESE FORMULAS LOOKAT YOUR

FUTURE PROMISED CASH FLOWS, AND

DISCOUNT THEM FOR TODAY

(SOMETIMES WE CALL THIS DISCOUNTED CASH FLOW)

68.

IT IS NOTACTUALLY HARD MATH, BUT IT

ISN’T EASY MATH EITHER

(UNLESS YOU ARE FROM ANYWHERE OUTSIDE OF THE US, IN WHICH CASE, IT IS

EASY)

69.

FORTUNATELY, BILL’S BOYSIN THE MS

EXCEL TEAM HAVE TAKEN THAT MATH

AND TRANSFORMED IT INTO A VERY

SIMPLE FORMULA IN EXCEL WHICH 7 OF

9 CHIMPANZEES CAN USE

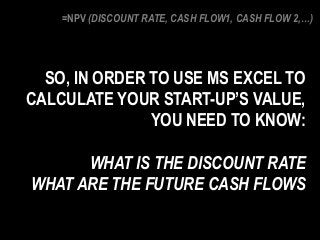

=NPV (DISCOUNT RATE,CASH FLOW1, CASH FLOW 2,…)

SO, IN ORDER TO USE MS EXCEL TO

CALCULATE YOUR START-UP’S VALUE,

YOU NEED TO KNOW:

WHAT IS THE DISCOUNT RATE

WHAT ARE THE FUTURE CASH FLOWS

YOU JUST GRABTHE PROFIT (NOT

REVENUE) LINE FOR YOUR NEXT 5

YEARS

(YOU GET THAT IN YOUR PRO-FORMA

P&L)

(NOTE FOR ADVANCED USERS: I AM NOT A FAN OF TERMINAL VALUE FOR START-

UPS, SO I WON’T COVER IT HERE. I’M ALSO NOT CONSIDERING DEBT SINCE IT IS A

START-UP. CORPORATE TREASURERS NEED TO READ SOMETHING MORE

ADVANCED THAN THIS DECK, AS I’M SURE YOU REALIZED ALREADY)

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

74.

CHOOSING THE DISCOUNTRATE

HOWEVER, IS SLIGHTLY HARDER

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

(SOMETIMES PEOPLE REFER TO DISCOUNT RATE AS WEIGHTED AVERAGE COST OF CAPITAL

OR WACC)

75.

THE DISCOUNT RATEIS A NUMBER

FROM 0 TO 1.

THE CLOSER TO 1 YOU GET, THE MORE

YOU DISCOUNT

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

76.

SO A DISCOUNTRATE OF .2 (20%) IS

NOT VERY RISKY AT ALL, AND A

DISCOUNT RATE OF .8 (80%) IS SUPER

RISKY.

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

77.

THE DISCOUNT RATEIS ACTUALLY

CALCULATED BASED ON MANY

CRITERIA

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

RISK

HOW CONFIDENT ISTHE INVESTOR

ABOUT THE LIKELIHOOD THE PROFIT

YOU FORECASTED WILL ACTUALLY

MATERIALIZE (REVENUE AND COST

ASSUMPTIONS ACCURATE?)

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

80.

OPPORTUNITY COSTS

HOW MUCHMONEY WOULD THE

INVESTOR MAKE IF SHE INVESTED THE

MONEY ELSEWHERE – ESPECIALLY IN

RISK-FREE THINGS LIKE T-BILLS…AND

WHAT ABOUT INFLATION…

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

81.

MARKET NORMS

THE DISCOUNTRATE WILL ALSO VARY

FROM MARKET TO MARKET WHERE THE

WISDOM OF CROWDS HAS GENERATED

RULES OF THUMB OVER THE YEARS

(IE: PHARMA RATES ARE DIFFERENT FROM E-COMMERCE

PORTAL RATES)

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

82.

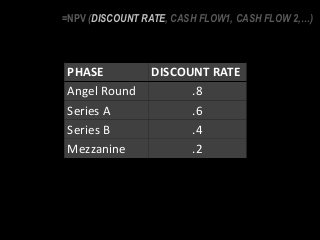

HOWEVER, HERE ISMY PERSONAL

INVESTING RULE OF THUMB,

GENERICALLY

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

83.

PHASE DISCOUNT RATE

AngelRound .8

Series A .6

Series B .4

Mezzanine .2

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

84.

IN OTHER WORDS,IF YOU ARE USING

A DISCOUNT RATE OF 50% AT THE

IDEA STAGE, I’M JUST NOT GOING TO

BITE

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

85.

BECAUSE THERE ISJUST SO MUCH

DAMN RISK THAT YOUR FORECASTS

WILL BE WRONG, OR YOU’LL DIE IN

EXECUTION

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

86.

AS I NEGOTIATEYOUR DISCOUNT

RATE WITH YOU, I’D ALSO BE

CONSIDERING A MOTLEY OF

FACTORS…

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

87.

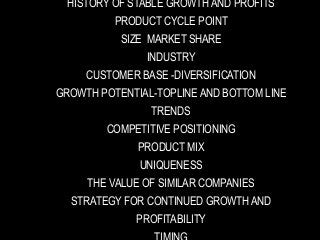

HISTORY OF STABLEGROWTH AND PROFITS

PRODUCT CYCLE POINT

SIZE MARKET SHARE

INDUSTRY

CUSTOMER BASE -DIVERSIFICATION

GROWTH POTENTIAL-TOPLINE AND BOTTOM LINE

TRENDS

COMPETITIVE POSITIONING

PRODUCT MIX

UNIQUENESS

THE VALUE OF SIMILAR COMPANIES

STRATEGY FOR CONTINUED GROWTH AND

PROFITABILITY

88.

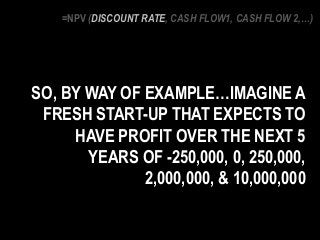

SO, BY WAYOF EXAMPLE…IMAGINE A

FRESH START-UP THAT EXPECTS TO

HAVE PROFIT OVER THE NEXT 5

YEARS OF -250,000, 0, 250,000,

2,000,000, & 10,000,000

=NPV (DISCOUNT RATE, CASH FLOW1, CASH FLOW 2,…)

89.

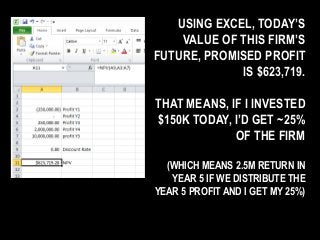

USING EXCEL, TODAY’S

VALUEOF THIS FIRM’S

FUTURE, PROMISED PROFIT

IS $623,719.

THAT MEANS, IF I INVESTED

$150K TODAY, I’D GET ~25%

OF THE FIRM

(WHICH MEANS 2.5M RETURN IN

YEAR 5 IF WE DISTRIBUTE THE

YEAR 5 PROFIT AND I GET MY 25%)

90.

OK, THAT'S NPV

LETME QUICKLY MENTION IRR AS

WELL SINCE IRR IS QUITE POPULAR

THESE DAYS

91.

AS WE MENTIONEDBEFORE,

INTERNAL RATE OF RETURN (IRR) IS

LIKE STANDING THE NPV FORMULA

ON IT'S HEAD AND SHAKING IT UP AND

DOWN

92.

THE IRR ISTHE DISCOUNT RATE THAT

WOULD MAKE THE NPV ZERO

OR, IN OTHER WORDS, THE IRR IS THE

RATE OF EXPECTED GROWTH

THE HIGHER THE IRR, THE BETTER

THE INVESTMENT

93.

AGAIN, BILL'S BOYSCAME TO THE

RESCUE

=IRR (INVESTMENT, CASH FLOW 1, CASH FLOW 2…)

94.

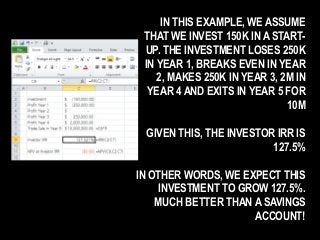

IN THIS EXAMPLE,WE ASSUME

THAT WE INVEST 150K IN A START-

UP. THE INVESTMENT LOSES 250K

IN YEAR 1, BREAKS EVEN IN YEAR

2, MAKES 250K IN YEAR 3, 2M IN

YEAR 4 AND EXITS IN YEAR 5 FOR

10M

GIVEN THIS, THE INVESTOR IRR IS

127.5%

IN OTHER WORDS, WE EXPECT THIS

INVESTMENT TO GROW 127.5%.

MUCH BETTER THAN A SAVINGS

ACCOUNT!

THAT SAID, WHILEIRR IS GREAT FOR

GIANT MULTI-NATIONAL FIRMS, I

PERSONALLY DON'T LIKE IT FOR

START-UPS

98.

TO ME, IRRWORKS BEST WHEN

COMPARING PROJECTS OF EQUAL

RISK OR EQUAL COST & INCOME

REALIZATION

99.

IT IS GREATFOR A BIG FIRM TRYING

TO COMPARE WHETHER TO BUILD A

NEW DATA CENTER OF EXTEND THE

EXISTING ONE

100.

BUT IMHO, ITIS NOT SO USEFUL AT

COMPARING WHETHER TO INVEST IN A

BIO-INFORMATICS START-UP OR A B2B

E-COMMERCE PORTAL, 2 PROJECTS

WITH SIGNIFICANTLY DIFFERENT RISK

& SPEND PROFILES

IN AN ACQUISITIONSITUATION,

RATHER THAN AN INVESTOR

SITUATION, HOPEFULLY THERE IS

SYNERGY VALUE BETWEEN BUYER

AND SELLER

103.

WHICH MEANS THATPART OF THE

VALUE OF THE DEAL IS NOT JUST

YOUR FUTURE REVENUE, BUT ALSO

THE POSITIVE IMPACT ON THE

BUYER’S REVENUE AS A RESULT OF

THE DEAL

104.

WHETHER THIS CANBE ADDED TO

THE BASE VALUATION IS UP TO YOUR

NEGOTIATION SKILLS, BUT IMHO, IT

SHOULD BE FACTORED IN TO BE FAIR

THE MOST COMMONWAY TO

GUESTIMATE MARKET VALUE IS TO

LOOK AT COMPARABLES (SIMILAR-ISH

COMPANIES TO YOURS)

110.

AND SINCE NOCOMPANY IS JUST LIKE

YOURS, YOU NEED TO TAKE A BUNCH

OF DATA POINTS TO TRIANGULATE

111.

THIS IS USUALLYDONE WITH P/E

RATIO

ACTUALLY, YOU CAN SOMETIMES ALSO CONSIDER: PRICE TO BOOK RATIO, EQUITY / SALES,

EQUITY / CASH FLOW, EQUITY / PAT, EQUITY / BOOK VALUE OF SHARE. BUT PE IS FAR

MORE COMMON FOR START-UPS

112.

P/E STANDS FOR

PRICE/ EARNINGS

(THINK OF PRICE AS SYNONYMOUS WITH VALUATION

FOR THE MOMENT)

113.

SO IF AFIRM’S VALUE IS 8 MILLION

AND THEIR EARNINGS WERE 2

MILLION, THE P/E RATIO WOULD BE 4

SINCE

8 / 2 = 4

TO GET AVALUE FOR YOU, WE NEED

TO USE THE AVERAGE MULTIPLE

ACROSS ALL THE COMPARABLE

FIRMS WHO HAVE BEEN VALUED.

LET’S ASSUME FOR NOW, THAT THE

AVERAGE MULTIPLE TURNED OUT TO

BE 4

116.

WITH THE MULTIPLEAND YOUR

PROFIT THIS YEAR, WE CAN REVERSE

CALCULATE YOUR PRICE (VALUATION)

117.

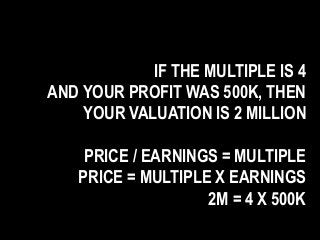

IF THE MULTIPLEIS 4

AND YOUR PROFIT WAS 500K, THEN

YOUR VALUATION IS 2 MILLION

PRICE / EARNINGS = MULTIPLE

PRICE = MULTIPLE X EARNINGS

2M = 4 X 500K

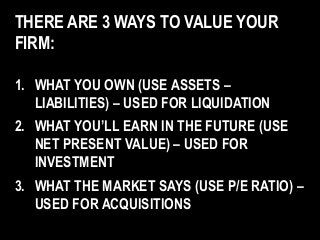

THERE ARE 3WAYS TO VALUE YOUR

FIRM:

1. WHAT YOU OWN (USE ASSETS –

LIABILITIES) – USED FOR LIQUIDATION

2. WHAT YOU’LL EARN IN THE FUTURE (USE

NET PRESENT VALUE) – USED FOR

INVESTMENT

3. WHAT THE MARKET SAYS (USE P/E RATIO) –

USED FOR ACQUISITIONS

129.

SHARE THIS DECK

&FOLLOW ME(please-oh-please-oh-please-oh-please)

stay up to date with my future

slideshare posts

http://www.slideshare.net/selenasol/presentations

https://twitter.com/eric_tachibana

http://www.linkedin.com/pub/eric-tachibana/0/33/b53

CREATIVE COMMONS ATTRIBUTIONS

Dr.Evil: http://www.flickr.com/photos/bpage/

Attribution Slide: http://www.flickr.com/photos/21572939@N03/

Please note that all content & opinions

expressed in this deck are my own and don’t

necessarily represent the position of my

current, or any previous, employers