Download to read offline

![Copyright © 2013 by ScottMadden. All rights reserved.

Training and Audit

Understand requirements for language translation, and

translate both system and collateral communication and

training materials where required

There are both regulatory and cultural reasons for

translating a system into the local language

— In countries like France and Germany, local

language translation may be required by the

Workers’ Councils. In places like Japan, it may

not be common for employees to read and write

in English; therefore, Japanese translation is

required

— Ask for advice on translation from international

HR representatives and legal counsel

Some applications, like Concur, offer in-system language

translation that can be easily applied to an existing

configuration. Custom fields can be translated with

assistance from representatives in country to ensure

fluency and accuracy

Centralize your T&E audit function for efficiency in audit

and consistency in policy interpretation

Once T&E policies are harmonized, efficiencies and cost

savings can be gained by centralizing T&E audit in one

location

— Using one group to administer T&E policy

ensures consistency across the organization.

Reporting centrally will provide consistency in

audit, allowances, and exceptions that can be

difficult to achieve in a decentralized model

— Cycle times for review and approval of T&E do

not require 24-hour employee support and can be

managed with e-communication, documented

approval and processing schedules, and a clear

escalation procedure

— A global company might leverage additional

locations or processors to optimize parts of the

financial process

Hire T&E auditors with foreign language proficiency to

ensure accuracy and provide support in reviewing expense

reports from international locations

— Many U.S. cities offer a diverse workforce with

many language capabilities

— Vendors exist who can offer support for foreign

languages that are not frequently used in the

organization

6

Category

Category

[Japanese] Expense Type

Exp Type

[Japanese]

02 - Meals and Entertainment 食事・ 接待交際費 Per Diem 国内出張: 食事日当

ガ ソ リ ン 代03 - Transportation 交通費 Gas / Petrol

空港使用料

03 - Transportation 交通費 Car Rental レ ン タ カ ー

03 - Transportation 交通費 Airport Tax

航空運賃

02 - Meals and Entertainment 食事・ 接待交際費 Special Events 全社イ ベン ト

03 - Transportation 交通費 Airfare](https://image.slidesharecdn.com/scottmaddeninternationalteimplementation-140410151734-phpapp01/85/International-Travel-and-Expense-Implementation-7-320.jpg?cb=1397143191)

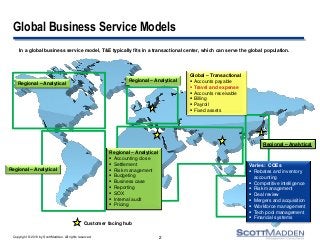

In a global business service model, travel and expense services typically fit in a transactional center, which can serve the global population. Many challenges exist with international travel and expense due to the complexities that come with a global process including policy standardization, regulatory and data protection compliance, system choices, and design options, among others. ScottMadden provides best practices for planning and preparation, requirements and design, and training and audit when implementing a global travel and expense program. This report discusses ScottMadden's best practices for implementing international travel and expense administration.