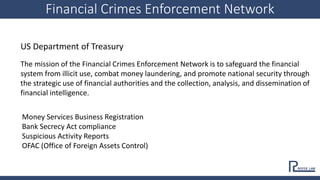

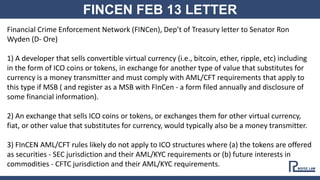

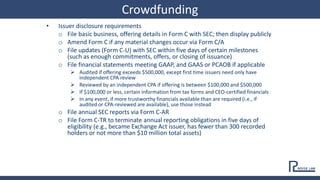

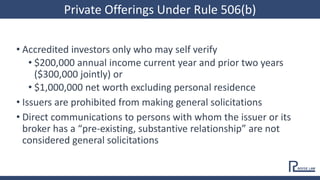

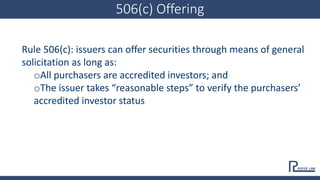

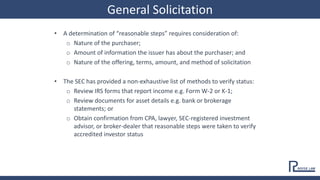

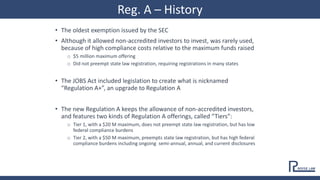

Downloaded 23 times

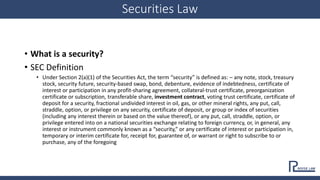

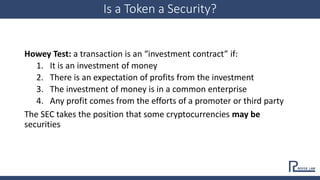

![Rule 10(b)-5 Private Right of Action

Section 10(b) of the Securities Exchange Act of 1934 gives shareholders a

private right of action to seek damages for securities fraud

Rule 10b-5 forbids “any person, directly or indirectly, . . . [t]o make any untrue

statement of a material fact” in connection with the purchase or sale of

securities

Ripple XRP Class Action Lawsuits are an example](https://image.slidesharecdn.com/ideatoipobc-181219193157/85/Idea-To-IPO-Blockchain-Slides-68-320.jpg)

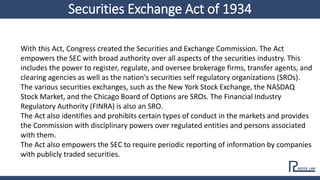

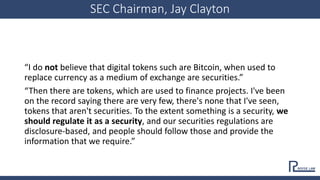

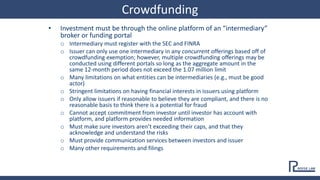

![Exemption from Registration

• The private company issuer (aggregated with predecessors and companies

under common control) may sell up to $1.07 million of securities in a 12-month

period [adjusted for inflation]

• Individual investments in all crowdfunding issuers in a 12-month period are

limited to:

o If either their annual income or net worth is less than $107,000, then the

greater of:

$2,200 or

5 percent of the lesser of their annual income or net worth

o If both their annual income and net worth are equal to or more than

$107,000, then

10 percent of the lesser of their annual income or net worth (up to a

maximum of $107,000)

o Issuer may rely on intermediary’s calculation of investor limits, unless issuer

knew it was or would be wrong

• Process is expensive and burdensome

Reg CF Crowdfunding](https://image.slidesharecdn.com/ideatoipobc-181219193157/85/Idea-To-IPO-Blockchain-Slides-75-320.jpg)

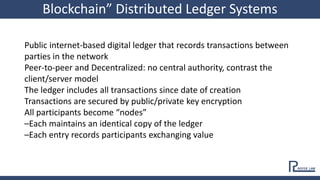

The document provides an overview of blockchain technology, including its features, mechanisms, and implications for business and finance. It discusses the evolution of trust protocols, consensus mechanisms like proof of work and proof of stake, and the role of blockchain in reducing costs and fostering innovation. Additionally, it addresses legal considerations regarding tokens and securities, highlighting the potential for blockchain to disrupt traditional industries and create new economic opportunities.