QSBS for startups, Investors and founders

•Download as PPTX, PDF•

0 likes•28 views

QSBS Qualified Small Business Stock

Recommended

Recommended

More Related Content

Similar to QSBS for startups, Investors and founders

Similar to QSBS for startups, Investors and founders (20)

More from Roger Royse

More from Roger Royse (20)

Recently uploaded

Recently uploaded (20)

QSBS for startups, Investors and founders

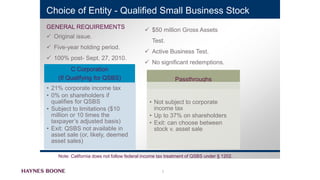

- 1. C Corporation (If Qualifying for QSBS) • 21% corporate income tax • 0% on shareholders if qualifies for QSBS • Subject to limitations ($10 million or 10 times the taxpayer’s adjusted basis) • Exit: QSBS not available in asset sale (or, likely, deemed asset sales) Passthroughs • Not subject to corporate income tax • Up to 37% on shareholders • Exit: can choose between stock v. asset sale Choice of Entity - Qualified Small Business Stock GENERAL REQUIREMENTS Original issue. Five-year holding period. 100% post- Sept. 27, 2010. $50 million Gross Assets Test. Active Business Test. No significant redemptions. Note: California does not follow federal income tax treatment of QSBS under § 1202. 1

- 2. Shareholder Requirements Original issuance In exchange for money, property or services, NOT stock Options can become QSBS on exercise What about SAFEs? QSBS contributed to an LLC or partnership 2

- 3. Company Requirements $50 million is based on cash and tax basis (not FMV) Measured before close of financing Qualified trade or business - 80% of company assets must be used in a qualified trade or business Working capital safe harbor - No more than half of the value of the company can be working capital Real estate, stock or securities - No more than 10% of the value of the company can be held in real estate, stock or securities 3

- 4. Redemptions Shares issued within 2 years before or 2 years after a redemption from a taxpayer or related party may not be QSBS Shares issued one year before or after a 5% redemption may not be QSBS De minimus ($10,000 or 2%) and exceptions for employment termination, death, divorce etc. Secondary sales 4

- 5. Planning S corporations LLCs taxed as partnerships Stacking through gifting Married filing jointly exemption amount Rollovers 351 Transactions 5