Navneet Education Financials and Valuation Analysis

•

3 likes•2,294 views

- Navneet Education Ltd is an Indian publishing and stationery company that saw sales grow from Rs. 82207 lacs in FY13 to an estimated Rs. 110463 lacs in FY16, with net profit estimated to grow from Rs. 10860 lacs to Rs. 13350 lacs over the same period. - The paper and publishing industries in India are expected to see continued growth, supported by a growing economy and population as well as low per capita paper consumption relative to other countries. - Navneet has leading market positions in its key business segments and is pursuing growth through expanding its product catalog and exploring new markets.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Navneet Education Financials and Valuation Analysis

Similar to Navneet Education Financials and Valuation Analysis (20)

More from Peeyush Sahu CAPM®

More from Peeyush Sahu CAPM® (13)

Recently uploaded

Recently uploaded (20)

Navneet Education Financials and Valuation Analysis

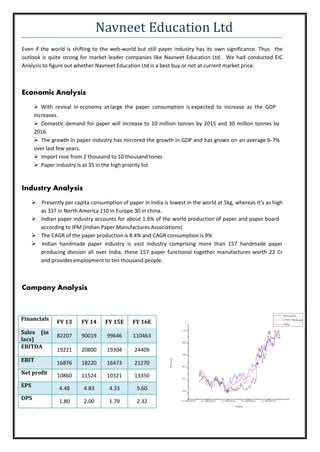

- 1. Financials FY 13 FY 14 FY 15E FY 16E Sales (in lacs) 82207 90019 99646 110463 EBITDA 19221 20800 19304 24409 EBIT 16876 18220 16473 21270 Net profit 10860 11524 10321 13350 EPS 4.48 4.83 4.33 5.60 DPS 1.80 2.00 1.79 2.32 Prices Navneet Education Ltd Even if the world is shifting to the web-world but still paper industry has its own significance. Thus the outlook is quite strong for market leader companies like Navneet Education Ltd. We had conducted EIC Analysis to figure out whether Navneet Education Ltd is a best buy or not at current market price. Economic Analysis With revival in economy at large the paper consumption is expected to increase as the GDP Increases. Domestic demand for paper will increase to 10 million tonnes by 2015 and 30 million tonnes by 2016. The growth in paper industry has mirrored the growth in GDP and has grown on an average 6-7% over last few years. Import rose from 2 thousand to 10 thousand tones Paper industry is at 35 in the high priority list Industry Analysis Presently per capita consumption of paper in India is lowest in the world at 5kg, whereas it’s as high as 337 in North America 110 in Europe 30 in china. Indian paper industry accounts for about 1.6% of the world production of paper and paper board according to IPM (Indian Paper Manufactures Associations) The CAGR of the paper production is 8.4% and CAGR consumption is 9% Indian handmade paper industry is vast industry comprising more than 157 handmade paper producing division all over India, these 157 paper functional together manufactures worth 22 Cr and provides employment to ten thousand people. Company Analysis Navneet CNX Midcap Nifty 1.0 0.8 0.6 0.4 0.2 0.0 11-09-2012 11-03-2013 11-09-2013 11-03-2014 11-09-2014 Date

- 2. Key Data CMP 113 Target price 125 (19% upside) 52 week high/low 120/24.10 Market cap 229997 EV (in crore) 299042 Recommendation BUY The share prices of Navneet mirrors the benchmark CNX Nifty and CNX midcap. With the present conducive changes in government policies, the economy is poised to move northwards, so is Navneet. During FY10-14, the revenues have grown at a CAGR of 13.50% to 882.1crore The publication segment has grown on the back of syllabus changes while the stationery segment continues to grow on the back of healthy exports The company is also exploring other avenues for growth. It has completed developing content for Standards 1-7 for the CBSE Board and has also started marketing the same in its key states – Maharashtra and Gujarat. Thereby, expect revenues to grow at a CAGR of 15.28% to touch 1,08,220 crore by FY16E. The publication segment has grown at a CAGR of 19.33% during FY10-14. A series of syllabus changes has aided this growth (Considering that there is visibility for syllabus changes in both Maharashtra and Gujarat over the next two academic years and that the common curriculum would aid in boosting revenues, ) Company is expecting the publication segment to grow at a CAGR of 19.33% to 48704 Cr by FY16E The stationery segment has recorded revenue growth of 19.5%, albeit on a small base, during FY10- 14. The company supplies its stationery products to global retail giants like Walmart, Target, Tesco, etc. We expect stationery segment revenues to grow at 8.6% (FY14-16E) to 494.7 Cr. Valuation In the publication and e-learning business, content is king. Navneet has over five decades of experience in developing content. It has an asset base of over 185 authors that create content and update the same timely. Even as an established player in this business it takes almost two years for Navneet to enter newer markets and even longer for it to set up, create content and build distribution channels. Navneet has a long standing relationship with state boards and also schools. This is very important in this business as the state boards recommend which workbooks, guides, etc. should be used. Navneet also has a strong distribution channel, which enables easy distribution and supply of its products. We continue to believe in the company and like its strong fundamentals. The company’s efforts to boost sales are bearing fruit and they shall also aid growth, going forward. However, the growth potential of the company has been discounted in the price. We, therefore maintain our target price of ₹ 125. We maintain a BUY rating on the stock. VALUATION Summary FY 13 FY 14 FY 15E FY 16E P/E 13.65 19.97 22.28 17.23 EV/Share 67.8 106.0 104.3 107.6 EV to EBITDA 8.41 12.14 12.87 10.50 Price to book 3.47 4.81 4.27 3.72 ROCE 27.3% 25.7% 20.3% 23.1%

- 3. Peers comparison 5 yr EV/sales EV/EBITDA PE Equity Enterprise EPS Company value value CAGR 2015 2016 2015 2016 2015 2016 PEG 2015 Navneet 377 405 13.6% 2.6 x 2.4 x 13.3x 10.5x 23.1 x 17.8 x 1.7 x MPS 195 191 Sandesh 58 36 DIC_India 53 52 57.1% 5.1 x 4.2 x 16.6x 13.5x 8.7% 0.7 x 0.6 x 1.0 x 0.9 x (13.4) 0.5 x 0.5 x 9.1 x 7.9 x 26.2 x 25.1 x 7.0 x 6.4 x 24.1 x 19.0 x 0.5 x 0.8 x N/A SWOT Analysis: Strengths: • Publishing Segment enjoys over 60% Market share in Western India. • Strong Brand name & strong network. • Strong Entry Barriers in Publication segment. • Enjoys Pricing Power • Unique & scalable business model of eSense. Weaknesses: • Publication business is seasonal in nature with 55% to 60% sales occuring in first quarter. • Publication growth is driven by changes in syllabus. Opportunities: • E-Learning Market at nascent stage - 90% market still untapped. • Organized Stationery players gaining market share at 12% annually. • Expansion of K-12 and Pre-school provides humungous opportunities. • Huge untapped potential in Education Sector. Threats: • Competition from Second Hand Book market for guides. • Stationery segment faces tough competition from cheap Chinese products. • Fluctuations in Paper Prices which is the major Raw Material. Conclusion: Among peers, Navneet is the most mature company with $405 m as Enterprise value & with equity of $377 m. Barring MPS, Navneet has shown the best EPS growth rate at 13.6% compounded annually. The high EV/sales & EV/EBITDA shows the positive market perception of Navneet as a growth stock. The estimated PE ratio also confirms our hypothesis. The combined effect of lower PEG ratio & high EPS predicts that the company will give better results than its peers in near term horizon.