Download as PDF, PPTX

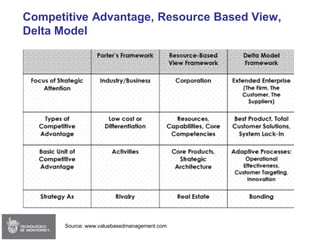

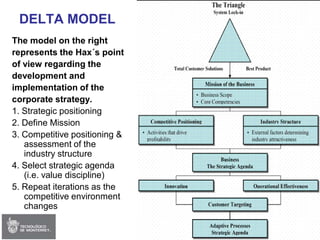

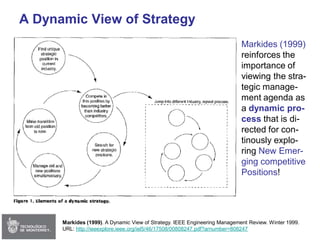

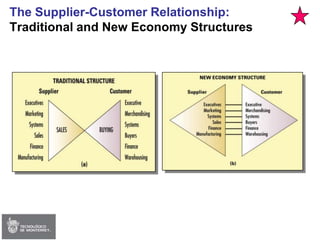

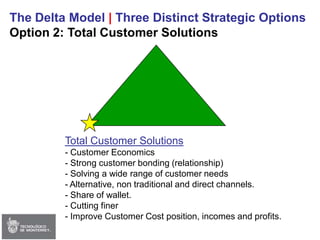

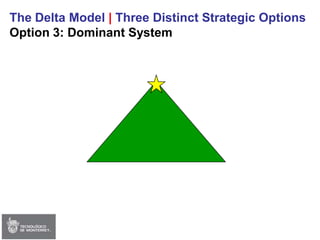

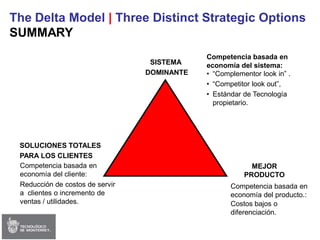

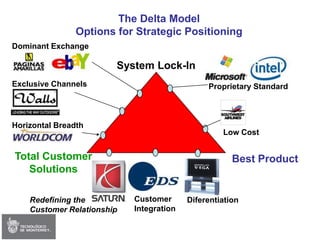

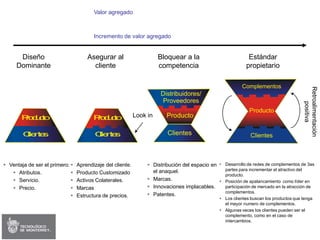

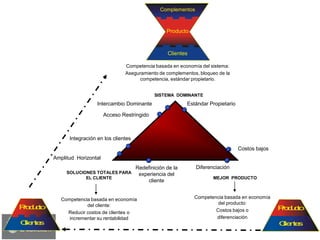

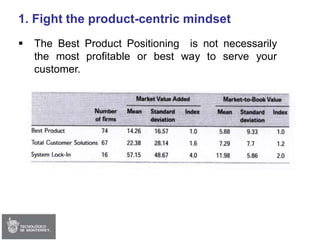

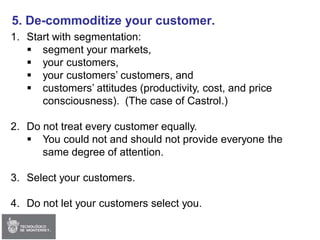

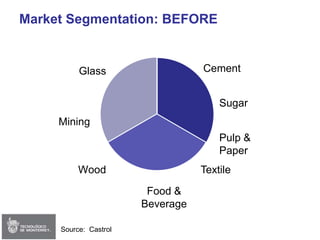

The document discusses strategic options for achieving competitive advantage using the Delta Model. It describes three strategic options: Best Product, focusing on product economics and differentiation; Total Customer Solutions, focusing on customer economics and bonding; and Dominant System, focusing on the economics of the entire system and complementors. Each option provides a distinct basis for competition. The document also discusses challenges of transforming organizations from product-centric to customer-centric strategies and the importance of viewing strategy as dynamic rather than static.

![제 15회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [Find Your Style 팀] : 사용자 이미지 라벨링을 통한 의류 추천 시스템](https://cdn.slidesharecdn.com/ss_thumbnails/04findyourstyle-220124104046-thumbnail.jpg?width=640&height=640&fit=bounds)

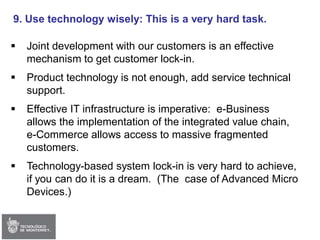

![Strategic analysis case-framework.ppt[1]](https://cdn.slidesharecdn.com/ss_thumbnails/strategicanalysis-case-framework-ppt1-120426102932-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)