1. Q4 2012 | RETAIL MARKET

RESEARCH & FORECAST REPORT

Houston’s Retail Market Absorption Boosted by

Year-End Push

Houston’s retail market posted 1.1M square feet of positive net absorption in Q4,

bringing the year-end 2012 total to 1.2M SF. The opening of Phase 1 of the Tanger

Outlet Center in Texas City, as well as the opening of the new HEB in Cypress,

contributed over 534,000 SF to the fourth quarter’s positive net absorption. Other

MARKET INDICATORS

tenants that moved during the fourth quarter include American Girl, Wellborne

YE 2011 YE 2012 Cinema, Bone Daddy’s and Serious Cigars.

CITYWIDE NET

ABSORPTION (SF) 1.8M 1.2M

Houston’s retail vacancy rate decreased from 7.2% to 7.0% between quarters as

CITYWIDE AVERAGE

well as over-the-year. Due to the large amount of new inventory deliveries,

VACANCY 7.2% 7.0% Houston’s retail vacancy only decreased 2% between quarters, despite the

significant positive absorption.

CITYWIDE AVERAGE

RENTAL RATE $15.13 $14.34 The citywide average quoted rental rate for all property types is $14.34 per square

foot; however, rental rates vary widely from $10.00 to $70.00 per square foot

DELIVERIES (SF) 625K 1.1M

depending on location and property type and class.

UNDER CONSTRUCTION

(SF) 617K 451K The Houston metropolitan area added 85,000 jobs between November 2011 and

November 2012, an annual increase of 3.1% over the years prior job growth.

Further, Houston’s unemployment rate fell to 5.8% from 7.3% one year ago which

has bolstered annual home sales in the Houston area. With continued expansion in

the energy industry and a strong housing market, Houston’s economy is expected

to remain healthy for both the near and long-term.

JOB GROWTH & UNEMPLOYMENT

(Not Seasonally Adjusted)

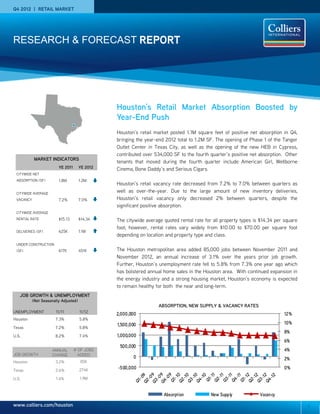

ABSORPTION, NEW SUPPLY & VACANCY RATES

UNEMPLOYMENT 11/11 11/12

2,000,000 12%

Houston 7.3% 5.8%

1,500,000 10%

Texas 7.2% 5.8%

8%

U.S. 8.2% 7.4% 1,000,000

6%

500,000

ANNUAL # OF JOBS 4%

JOB GROWTH CHANGE ADDED

0 2%

Houston 3.2% 85K

Texas 2.6% 274K -500,000 0%

U.S. 1.4% 1.9M

Absorption New Supp ly Vacancy

www.colliers.com/houston 1

2. RESEARCH & FORECAST REPORT | Q4 2012 | HOUSTON RETAIL MARKET

Rental Rates Houston’s retail construction pipeline Q4 2012 ABSORPTION

contains 451,000 SF, of which

The citywide average quoted rental rate approximately 31% is pre-leased. SF

increased from $14.30 to $14.34 per Tenant

Fourth quarter deliveries totaled Occupied

SF NNN between quarters and 756,000 SF.

decreased from $15.13 over the year. Tanger Outlet Center – Ph1 350,000

Absorption & Demand

Class A in-line retail rental rates vary

Houston’s retail market posted 1.1M SF HEB 184,083

widely due to location and center type.

of positive net absorption in the fourth

Recent quoted rates for unanchored

quarter bringing the year-end total to Academy Sports 72,979

strip centers range from $20.00 -

1.2M SF. The opening of Phase 1 of the

$35.00 per SF (Class B and below can Kroger 48,501

Tanger Outlet Center in Texas City as

rent for $12.00 to $20.00 per SF)

well as the opening of the new HEB in

while power centers with three or LA Fitness 45,000

Cypress contributed over 534,000 SF

more strong anchors range from

to the fourth quarters positive net

$10.00 - $35.00 per SF. Lifestyle Thrift Outlet 26,402

absorption.

centers and newly constructed strip

centers in Class A locations such as Other notable tenants that moved into 99¢ Store 18,119

High Street, Uptown Park and The their space during the fourth quarter

Vintage range from $40.00 - $70.00 include: Academy Sports, Kroger, LA

American Girl 17,685

per SF. Fitness, and Thrift Outlet as seen in the

table to the right.

Vacancy & Availability Wellborne Cinema 15,180

Houston’s retail vacancy decreased Ogle School 11,468

from 7.2% to 7.0% in the fourth

quarter. By product type on a quarterly JB’s Multi Events 10,300

basis, outlet centers posted the largest

vacancy rate decrease from 10.1% to Velvet Restaurant 8,878

7.8%, 230 basis points. Strip centers,

neighborhood centers and theme/ Bone Daddy’s 7,000

entertainment vacancy rates remained

unchanged between quarters. Serious Cigars 7,000

HOUSTON RETAIL MARKET STATISTICAL SUMMARY

Direct Sublet Total 2012 YTD

Rentable Direct Sublet Total Vacant Q4 2012 Net Class A Rental

Vacancy Vacancy Vacancy Net

Area Vacant SF Vacant SF SF Absorption Rates (in-line)*

Rate Rate Rate Absorption

Strip Centers (unanchored) 31,381,269 3,247,523 10.3% 22,951 0.1% 3,270,474 10.4% 35,161 (89,158) $20.00-$35.00

Neighborhood Centers (one anchor) 68,820,507 7,301,626 10.6% 156,600 0.2% 7,458,226 10.8% 115,789 (335,197) $20.00-$32.00

Community Centers (two anchors) 40,772,147 2,548,743 6.3% 128,071 0.3% 2,676,814 6.6% 125,930 212,540 $15.00-$30.00

Power Centers (3 or more anchors) 20,297,712 874,797 4.3% 71,190 0.4% 945,987 4.7% 93,299 361,102 $10.00-$35.00

Lifestyle Centers 4,618,124 275,217 6.0% - 0.0% 275,217 6.0% 9,509 44,237 $40.00-$70.00

Outlet Centers 1,573,627 122,006 7.8% - 0.0% 122,006 7.8% 351,610 353,673 N/A

Theme/Entertainment 653,840 224,804 34.4% - 0.0% 224,804 34.4% - - $25.00-$35.00

Single-Tenant 63,079,142 1,491,177 2.4% 33,660 0.1% 1,524,837 2.4% 364,472 444,792 N/A

Malls 29,487,935 1,770,164 6.0% 58,539 0.2% 1,828,703 6.2% 31,304 164,400 N/A

Greater Houston 260,684,303 17,856,057 6.8% 471,011 0.2% 18,327,068 7.0% 1,127,074 1,156,389

2

3. RESEARCH & FORECAST REPORT | Q4 2012 | HOUSTON RETAIL MARKET

RETAIL SALE TRANSACTIONS SALES ACTIVITY Woodlands and Montgomery County

submarket, was purchased as an

Houston retail investment sales activity investment. Some of the center’s

included 72 recorded transactions, with major tenants include Trader Joe’s, Ace

a total dollar volume of approximately Hardware, 24-Hour Fitness, and

$115.4M, averaging $116 per SF with PETCO.

an average capitalization rate of 8.7%.

West Loop Plaza1 West Houston Retail LLC purchased a

3005-3115 West Loop South, Houston, TX Some of the more significant four-property portfolio from Satya, Inc.

Inner Loop River Oaks Ret Submarket transactions that closed during the for approximately $15.8M in November.

fourth quarter include: The portfolio included four strip centers

RBA: 68,780 SF

Built: 2006 Becar Venture purchased the 68,780- totaling 71,374 SF and were located in

Buyer: Becar Venture

SF West Loop Plaza from Cathay Bank Richmond, Cypress and Houston, TX.

Seller: Cathay Bank The portfolio was purchased as an

Sale Date: December 5, 2012 in December for $9.9M. The

Sales Price: $9.9M neighborhood center, located in the investment. Some of the tenants in the

Sales Price PSF: $144 Inner Loop River Oaks submarket, was centers include Quick Weight Loss,

100% leased at the time of sale and Subway, New York Pizzeria, and State

was purchased as an investment. Farm.

Golfsmith and Mattress Giant are the LEASING ACTIVITY

center’s anchor tenants.

Houston retail leasing activity for fourth

RioCan REIT purchased the 180,000-SF

quarter 2012 totaled 841,061 SF in 323

Louetta Central Shopping Center,

transactions, compared to 346

Woodlands Crossing located in the North/Spring Creek

10864-10868 Kuykendahl Rd., The

transactions totaling 866,000 SF one

submarket, from URDANG & RCG

Woodlands, TX year ago. Overall, transactions under

Ventures in November for $26M. Major

Montgomery County Ret Submarket 10,000 SF comprised the largest group

tenants in the center include Michael’s,

of retail leases, with the market

RBA: 125,200 SF Famous Footwear, and Kohl’s.

recording only nine leases over 10,000

Built: 2012

Buyer: First Washington Realty First Washington Realty purchased the SF and two over 20,000 SF in the

Seller: Realm Realty 125,200-SF Woodlands Crossing fourth quarter.

Sale Date: December 19, 2012 Shopping Center from Realm Realty in

Sales Price: $43.2M December for $43.2M. The

Sales Price PSF: $345

neighborhood center, located in The

1Colliers International Transaction

Q4 2012 Top Retail Leases

Building name/address Submarket SF Tenant Lease date

Point Nasa Shopping Center NASA/Clear Lake 47,900 Conn's Oct-12

Cypress Landing Shopping Center NorthBelt/Greenspoint 28,193 Gold's Gym Dec-12

Pasadena Town Plaza Near Southeast 20,558 Goodwill Nov-12

Fondren Southwest Village Southwest 16,579 Palais Royal Oct-12

Westheimer Commons West/Far West 14,500 Shoe Carnival Oct-12

Meadow Park Shopping Center Southeast Outlier 14,000 Family Dollar Oct-12

Cypress Station Square Far North 13,400 Davita Dialysis Nov-12

Pasadena Town Plaza Near Southeast 8,702 Anna's Linens Nov-12

Cypress Station Shopping Center North FM 1960/I-45 7,344 The Pour House Oct-12

Village Green Shopping Center West/Far West 5,900 Snooker 147 Oct-12

908 Congress CBD 5,400 Batanga Restaurant Oct-12

West Loop Market Center Inner Loop/River Oaks 4,700 S Factor Oct-12

River Oaks Shopping Center Inner Loop/River Oaks 4,375 J. Jill Oct-12

3

4. RESEARCH & FORECAST REPORT | Q4 2012 | HOUSTON RETAIL MARKET

LISA R. BRIDGES COLLIERS INTERNATIONAL | HOUSTON

Director of Market Research Houston 1300 Post Oak Boulevard

Direct +1 713 830 2125 Suite 200

Fax +1 713 830 2118 Houston, Texas 77056

lisa.bridges@colliers.com Main +1 713 222 2111 Accelerating success.

COLLIERS INTERNATIONAL | P. 4