Masdar, Inpex to explore e-methane production in UAE

•

0 likes•4 views

The Tata Group will build a major electric vehicle battery gigafactory in the UK, investing over £4 billion. The factory will be one of Europe's largest, with production starting in 2026 and initially supplying 40GWh of batteries annually, nearly half of the UK's estimated 2030 needs. This represents a significant boost to the UK's plans to develop domestic EV battery supply. US natural gas inventories exceed the five-year average as production outpaces demand, keeping prices low. Rising gasoline inventories in the US have been driven by increased imports to the East Coast where prices are relatively high and refinery outages have reduced production.

Recommended

Recommended

More Related Content

Similar to Masdar, Inpex to explore e-methane production in UAE

Similar to Masdar, Inpex to explore e-methane production in UAE (20)

More from Khaled Al Awadi

More from Khaled Al Awadi (20)

Recently uploaded

Recently uploaded (20)

Masdar, Inpex to explore e-methane production in UAE

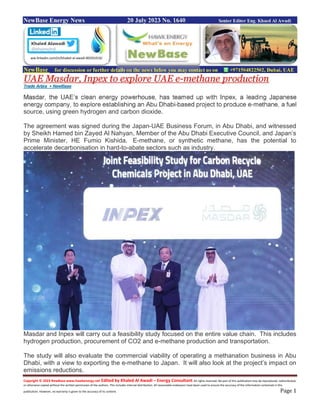

- 1. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 1 NewBase Energy News 20 July 2023 No. 1640 Senior Editor Eng. Khaed Al Awadi NewBase for discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE UAE Masdar, Inpex to explore UAE e-methane production Trade Arbia + NewBase Masdar, the UAE’s clean energy powerhouse, has teamed up with Inpex, a leading Japanese energy company, to explore establishing an Abu Dhabi-based project to produce e-methane, a fuel source, using green hydrogen and carbon dioxide. The agreement was signed during the Japan-UAE Business Forum, in Abu Dhabi, and witnessed by Sheikh Hamed bin Zayed Al Nahyan, Member of the Abu Dhabi Executive Council, and Japan’s Prime Minister, HE Fumio Kishida. E-methane, or synthetic methane, has the potential to accelerate decarbonisation in hard-to-abate sectors such as industry. Masdar and Inpex will carry out a feasibility study focused on the entire value chain. This includes hydrogen production, procurement of CO2 and e-methane production and transportation. The study will also evaluate the commercial viability of operating a methanation business in Abu Dhabi, with a view to exporting the e-methane to Japan. It will also look at the project’s impact on emissions reductions. ww.linkedin.com/in/khaled-al-awadi-80201019/

- 2. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 2 Masdar’s CEO, Mohamed Jameel Al Ramahi, said, “We are proud to be working with our Japanese partners to advance clean energy solutions. Today’s development opens an exciting new chapter for Masdar as we explore how to unlock the full potential of green hydrogen to produce fuel for homes and businesses. Ahead of the UAE hosting COP28, Masdar will continue to build upon strong alliances with our Japanese partners as we advance the global energy transition.” Inpex President & CEO Takayuki Ueda, said, “We position carbon recycling and methanation as one of our five net zero businesses, and this joint initiative with Masdar to explore the production of clean e-methane is fully aligned with our decarbonization efforts as well as our long-term commitment to Abu Dhabi, which is one of our core business areas. We hope to leverage this opportunity to provide added value for our stakeholders in Japan and the UAE, while helping realise a net-zero society by 2050.” E-methane does not impose special fuel conversion requirements upon consumers and can be accessed widely via countries’ existing gas infrastructure. This means it has the potential to accelerate decarbonisation without significantly increasing costs.

- 3. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 3 UAE: Adnoc Is Said to Boost Covestro Takeover Bid to €11 Billion Bloomberg + Newbase Abu Dhabi National Oil Co. has increased its takeover offer for Covestro AG to about €11 billion ($12.4 billion) as it seeks to convince the German chemical producer to enter talks, people familiar with the matter said. Adnoc’s latest proposal values Covestro at about €57 per share, up from its first informal bid of around €55, the people said, asking not to be identified because the information is private. The state-backed firm voiced confidence in Covestro’s strategy and management, according to the people. Shares of Covestro jumped 5.6% in late Frankfurt trading to close at €50.30, the highest level since February 2022. Last month, Leverkusen-based Covestro rejected Adnoc’s earlier proposal as too low, people familiar with the matter said at the time. Covestro also raised questions around Adnoc’s plans for its specialties operations. Adnoc has tried to address Covestro’s concerns about its offer, including over how it would help the German company’s management develop the specialty chemical operations, according the people. If negotiations are entered, there could be scope for further increases in Adnoc’s bid. Deliberations are ongoing, and it’s unclear how Covestro will respond to the latest proposal. Representatives for Adnoc and Covestro declined to comment. Adnoc, which produces almost all the oil in the United Arab Emirates, plans to invest $150 billion to expand production capacity for crude, natural gas and chemicals. It’s also in separate talks with Austria’s OMV AG about a potential merger of two petrochemical firms they back, Borouge Plc and Borealis AG

- 4. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 4 UAE: Adnoc Gas announces $7bn LNG deal with Indian Oil TradeArabia News Service Adnoc Gas, a world-class integrated gas processing company, has announced a 14-year supply agreement with Indian Oil Corporation Limited (IOCL) for the export of up to 1.2 million metric tonnes per annum (mmtpa) of liquefied natural gas (LNG) to India’s largest integrated and diversified energy company. The agreement, valued in the range of $7 billion to $9 billion over its 14-year term, signifies a major step forward in the partnership between the two industry leaders. The landmark deal marks another significant milestone for Adnoc Gas as it expands its global reach, reinforcing its position as a global LNG export partner of choice, and reaffirming IOCL as its key strategic partner in the LNG market. Commenting on the deal, CEO Ahmed Alebri said: "We are pleased to announce this long-term LNG sale, further strengthening the long-standing partnership with IOCL." "We look forward to expanding our collaboration and take pride in the knowledge that Adnoc Gas’ LNG exports will further support the development of IOCL and contribute to India’s growth story," he stated. Under the terms of the agreement, Adnoc Gas sai d it will deliver up-to 1.2 mmtpa of LNG to IOCL in India. The deal serves as a testament to its ability to meet the growing global demand for LNG, a critical fuel in the energy transition, it added.

- 5. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 5 India’s Tata Group to build $5 billion gigafactory in the UK CNBC - Anmar Frangoul The Tata Group will develop a major facility for the production of electric car batteries in the U.K., with the Indian conglomerate set to invest more than £4 billion (around $5.17 billion) in the project. The news represents a significant boost for the U.K.’s plans to secure its own supply of EV batteries as it looks to move away from vehicles that use gasoline and diesel. In a statement Wednesday, the U.K. government said the site would create as many as 4,000 direct jobs and provide Jaguar Land Rover — a subsidiary of Tata Motors — with batteries. Other customers in the U.K. and Europe are also being eyed. The government said the factory would generate thousands of extra jobs further down the supply chain, in sectors connected to critical raw minerals and battery materials. “This investment will be crucial to boosting the UK’s battery manufacturing capacity needed to support the electric vehicle industry in the long term,” the government said. “With an initial output of 40GWh it will also provide almost half of the battery production that the Faraday Institution estimates the UK will need by 2030,” it added. The gigafactory will be one of Europe’s largest. The aim is for production to start in 2026. So-called gigafactories are facilities that produce batteries for electric vehicles on a large scale. Tesla CEO Elon Musk has been widely credited as coining the term. It’s been widely reported that the U.K. will provide Tata with significant subsidies for the project. The government said details of its support to Tata Sons would be “published in due course as part of our regular transparency data.” The gigafactory will be one of Europe’s largest, according to the U.K. government. The aim is for production to start in 2026, with the Tata Group planning to invest over £4 billion in the project. The news represents a significant boost for the U.K.’s plans to secure its own supply of EV batteries.

- 6. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 6 Speaking to the BBC on Wednesday morning, Grant Shapps, the secretary of state for energy security and net zero, said the news represented “certainly the biggest U.K. car investment for 40 years” and “a big vote of confidence in the British economy.” Pushed on the value of the incentive given to Tata, Shapps acknowledged it was “large and … I make no bones about that,” but would not give an exact figure. The numbers, he added, “will come out in the usual way, because of the commercial sensitivity.” The U.K. wants to stop the sale of new diesel and gasoline cars and vans by 2030 and will require, from 2035, all new cars and vans to have zero-tailpipe emissions. News about the gigafactory plans was welcomed by those within the industry. “This is a shot in the arm for the UK automotive industry, our economy and British manufacturing jobs, demonstrating the country is open for business and electric vehicle production,” Mike Hawes, chief executive of the Society of Motor Manufacturers and Traders, said. “It comes at a critical moment, with the global industry transitioning at pace to electrification,” he added. Production of batteries within the U.K. was, Hawes said, “essential if we are to anchor wider vehicle production here for the long term.”

- 7. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 7 U.S Natural gas storage injections exceed five-year average U.S. Energy Information Administration, Weekly Natural Gas Storage Report Working natural gas inventories totaled 2,930 billion cubic feet (Bcf) in the Lower 48 states as of July 7, according to our Weekly Natural Gas Storage Report. U.S. natural gas production has outpaced demand, resulting in more natural gas injected into storage midway through the 2023 refill season (April 1–October 31). Since April 1, net injections into natural gas storage have exceeded the five-year (2018–22) average by 6% (66 Bcf), and working natural gas inventories have reached 69% of working gas capacity so far this refill season. The increased surplus of working natural gas inventory has reduced natural gas prices during the first half of this year. Last summer, large deficits to the five-year average contributed to high natural gas prices, and the daily near-month futures price rose above $9.00 per million British thermal units (MMBtu) on several occasions.

- 8. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 8 When the deficit to the five-year average eased late last summer, prices began to fall. Working natural gas stocks have been at a surplus to the five-year average since January 2023. This surplus reached a high in March and has remained above average since the start of refill season in April. Prices began to decline in January from an average of $5.53/MMBtu in December 2022 and have averaged below $2.50/MMBtu since February. Data source: U.S. Energy Information Administration, Weekly Natural Gas Storage Report and Short-Term Energy Outlook (STEO) In our June Short-Term Energy Outlook, we forecast that storage injections will slow because of relatively flat natural gas production and increased natural gas use in the electric power sector to meet cooling demand for the remainder of the summer. Nevertheless, we expect working natural gas inventories to remain above the five-year average for the rest of the year.

- 9. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 9 U.S. gasoline inventories are rising, driven by East Coast market dynamics source: U.S. Energy Information Administration, Weekly Petroleum Status Report U.S. gasoline inventories have been rising following a low this year of 216 million barrels (8% below the previous five-year average) on May 26. East Coast (PADD 1) gasoline inventories account for most of the national inventory growth despite refinery unit outages that are limiting regional gasoline production. Relatively high gasoline prices on the East Coast and falling freight rates are driving U.S. imports from Europe, which is increasing regional inventories. On the East Coast, where gasoline consumption is typically greater than in other regions of the country, gasoline inventories had been trending near or below the previous five-year range until the past few weeks, when inventories began building. On May 26, gasoline inventories in this region totaled 53.2 million barrels, or 15% less than the previous five-year average. After May 26, however, both U.S. and East Coast inventories increased. U.S. gasoline inventories increased by 3%, or 5.9 million barrels, reaching 222.0 million barrels on June 23, about the same as last year at the same time. East Coast gasoline inventories increased by 2.4 million barrels (5%) over the same period, reaching 55.7 million barrels, which is 2.3 million barrels (4%) more than at the same time last year. Both U.S. and East Coast inventories have fallen since June 23 but remain above their respective May 26 levels.

- 10. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 10 Gasoline inventories on the East Coast have increased despite refinery issues affecting gasoline production. At the Phillips 66 refinery in Bayway, New Jersey, the fluid catalytic cracker (FCC), primarily used for producing additional gasoline in refining, came offline, and the outage will reduce gasoline production by 100,000 barrels per day (b/d), according to trade press reports. Reports indicate that repairs to the FCC will be made over the next few weeks, and gasoline production should increase once the unit is back online. Our data indicate that gasoline imports into the U.S. East Coast have increased since March, which follows seasonal trends, and reached 823,000 b/d in June, the highest monthly average (based on the four-week moving average) since July 2019. The East Coast primarily receives its gasoline imports from Europe, which increased by 173,000 b/d between March and June, according to data from Vortexa Analytics. In addition to the relatively high gasoline prices on the East Coast, lower shipping rates are also supporting gasoline imports.

- 11. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 11 NewBase July 20 -2023 Khaled Al Awadi NewBase for discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE Oil steady on lower U.S. crude stocks, cautious demand outlook Reuters + NewBase Oil prices were little changed on Thursday as a lower-than-expected drop in U.S. crude inventories and a potentially weaker demand outlook kept investors cautious. September Brent futures climbed 34 cents, or 0.431%, at $79.80 a barrel by 10.00 GMT, while August U.S. West Texas Intermediate (WTI) crude gained 5 cents, or 0.1%, to $75.40 a barrel. The August WTI contract expires on Thursday. September WTI crude was higher by 6 cents, or 0.1%, to $75.35. "Following some heavy selling pressure overnight, there is an attempt for oil prices to stabilise this morning," said Yeap Jun Rong, market strategist at IG. Oil price special coverage

- 12. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 12 Prices fell in the previous session as investors took profits after data showed U.S. inventories fell less than analysts expected. Meanwhile, the U.S. dollar (.DXY) was largely unchanged at 0645 GMT, edging down 0.1%. The outlook for demand in China, the world's biggest crude buyer, was also unclear amid its slowing economy. Crude prices may struggle to find a clear direction amid a mixed global demand outlook in the next few weeks, Citi analysts said in a note. Demand is "a mixed picture with stronger gasoline and jet fuel demand, but weaker petchems and diesel," the analysts said. Brent crude prices have broken to a higher range through July, after getting stuck at $72-$78 through May and June, the Citi analysts added, with support from Saudi output cuts and geopolitical risks. Reporting by Jeslyn Lerh in Singapore; Additional reporting by Laura Sanicola in Washington; Editing by Sonali Paul, Miral Fahmy and Kim Coghill

- 13. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 13 NewBase Specual Coverage The Energy world –July-20 -2023 CLEAN ENERGY A new global gas market is taking shape in the aftermath of the 2022 supply shock *Global Gas Security Review 2023* IEA The global energy crisis triggered by Russia’s invasion of Ukraine transformed natural gas markets in a structural manner with profound implications both for policy makers and market players. LNG became a new baseload supply for Europe, while China’s balancing role in the global gas market is set to increase. In this context, the architecture of global gas supply security and the underlying flexibility mechanisms need to be reassessed through an ever-closer dialogue between responsible producers and consumers. Global gas supply security remains at the forefront of energy policymaking, with growing complexity both in the short- and long term. While market fundamentals have significantly eased since the start of 2023, and the European Union is well on track to fill up its storage sites to 95% of working capacity, full storage sites are no guarantee against winter volatility. Our simulations show that a cold winter, together with a full halt of Russian piped gas supplies to the European Union starting from 1 October 2023, could easily renew price volatility and market tensions. The growing flexibility and liquidity of the global LNG market was crucial in the response to the gas supply shock of 2022. The non-observance of Russian piped gas contracts increased the European Union’s reliance on spot procurements, which rose from just 20% of total gas supply in 2021 to over 50% in 2023. Through the medium term, a fine balance should be struck between long- term contracts from non- Russian suppliers and exposure to an increasingly liquid spot market. Our review of LNG contracting trends indicates that European buyers have increased their LNG contracting activity since Russia’s invasion of Ukraine, though they still account for just 20% of total LNG volumes contracted since the start of 2022 – while China’s share topped 25%. Considering that in an increasingly globalised gas market, storage regulations can have extra- regional implications, the International Energy Agency carried out a survey on natural gas storage and its evolving regulatory frameworks across the members of the International Energy Agency's Task Force on Gas and Clean Fuels Market Monitoring and Supply and Security. It showed that in the wake of the global gas crisis triggered by Russia, more stringent storage regulations have been adopted across key markets. The integration of low-emission gases into the gas and broader energy system will be crucial to decarbonise gas supply streams. This year’s Global Gas Security Review provides a special focus on the storage of low-emission gases and the future role of liquefied low-emission gases in the international maritime sector. Natural gas markets moved towards a gradual rebalancing in H1 2023 Russia’s steep cuts in gas deliveries to the Europe Union – a drop of almost 80 bcm, equating to 15% of global LNG trade – put unprecedented pressure on European and global gas markets in 2022. This gas supply shock caused by Russia led to a reconfiguration of global LNG flows, drove

- 14. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 14 natural gas prices to all- time highs, both in Asia and Europe, and necessitated a readjustment in gas demand. Natural gas consumption fell by an estimated 1.5% in 2022 – similar to the drop experienced in 2020 following the first wave of Covid-19 lockdowns. Since the start of 2023, natural gas markets moved towards a gradual rebalancing due to timely policy action, efficient market forces and favourable weather conditions over the 2022/23 heating season. Spot gas prices in Asia and Europe fell by over 50% year- on-year in H1 2023, albeit remaining 140% and 180% above their H1 average levels between 2016-20, respectively. In the United States, strong growth in domestic gas production, together with an unseasonably mild Q1 2023, put downward pressure on benchmark Henry Hub prices, which fell by 60% year-on-year in H1 2023. The steep decline in natural gas prices in Asia and Europe occurred despite a tight supply environment. Russia’s piped gas deliveries to the European Union fell by over 75% (or 36 bcm) in H1 2023, while global LNG supply rose by an estimated 3% (or 9 bcm ) – insufficient to offset the decline in Russian piped supplies. Several non-Russian pipeline suppliers faced heavy maintenance and unplanned outages, further tightening supply. In this context, natural gas demand reductions played a key role in the softening of market fundamentals. In OECD Europe, natural gas demand fell by an estimated 10%, or over 30 bcm. This was primarily driven by lower residential and commercial demand in Q1, a sharp drop in gas use in the power sector during Q2 and depressed gas consumption by industrial consumers. In key Asian markets, natural gas demand remained close to last year’s levels in the first five months of 2023. While China returned to growth, these gains were almost entirely offset by demand drops in Japan and Korea, reflecting a mild Q1 and improving nuclear availability. Relatively muted demand in Asia has been a key contributor to the loosening of market fundamentals since the start of 2023.

- 15. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 15 Global gas demand is expected to remain broadly flat in 2023 and return to moderate growth of 2% in 2024, supported by the expansion of economic activity and assuming a return to average winter weather conditions in the Northern Hemisphere. The rapidly growing markets in the Asia Pacific region are expected to account for around 80% of incremental gas demand to the end of 2024. This short-term forecast is subject to an unusually wide range of uncertainties stemming from the broader geopolitical and macroeconomic environment. Softer market conditions in H1 2023 are no reason for complacency ahead of winter High natural gas inventory levels in key Asian and European markets provide cautious optimism ahead of the 2023/24 heating season in the Northern Hemisphere. However, full storage sites are no guarantee against winter volatility and the risk of renewed market tensions. The European Union inherited relatively high storage levels after the 2022/23 heating season, with inventories standing 60% above their five-year average. If injections continue at the average rate observed since mid-April, EU storage sites will reach 90% of their working capacity by early August and could be filled close to 100% by mid-September. If Russian piped gas supplies were to cease completely in summer 2023, the European Union would still be able to fill up storage sites to 90- 95% of working capacity on average by the start of the 2023/24 heating season. Nevertheless, key uncertainties remain ahead of Europe’s 2023/24 winter season. A cold winter could increase natural gas demand in the EU’s residential and commercial sectors by 30 bcm compared to the 2022/23 heating season. Given geopolitical uncertainties, a further decline in Russian piped gas deliveries to the European Union cannot be excluded. If Russian piped gas supplies were to fully stop from 1 October 2023, it would result in a total shortfall of 10 bcm.

- 16. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 16 Global LNG supply is expected to increase by around 15 bcm y-o-y, though project delays and/or unplanned outages could reduce incremental LNG supply. China’s LNG imports could fluctuate, with an uncertainty range of over 10 bcm through the 2023/24 winter. Considering these risk factors, gas storage trajectories could vary widely over the upcoming heating season. Our simulations show that a cold winter, together with a full stop of Russian piped gas supplies to the European Union starting from 1 October, could renew market tensions. If we assume a mild winter and LNG flows remaining close to last year’s levels, storage sites would end the heating season with inventory levels above 50% of capacity even without Russian piped gas. In contrast, a cold winter would put substantial pressure on the market. Higher LNG flows (a 15% y-o-y increase) would keep storage sites 34% full by the end of March. Yet if LNG flows remain at 2022/23 winter levels, storage sites would be just 25% full. Lower LNG availability (a 10% y-o-y decline) would further depress inventory levels to below 20% of capacity. Storage sites are typically less reactive when filled below 30% of their capacity, as withdrawal ability is reduced due to the drop in reservoir pressure. This could increase the risk of price volatility and supply disruptions in the case of a late cold spell coupled with low wind power output. Continued structural gas demand reductions – including via enhanced energy efficiency, the more rapid deployment of renewables and quicker installation of heat pumps – will be required to ensure a secure gas balance for the 2023/24 winter.

- 17. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 17 The 2022 gas supply shock transformed natural gas markets in a structural manner Russia's invasion of Ukraine profoundly transformed European and global gas markets. While the immediate effects of last year's supply shock have eased in recent months, the structural changes which emerged in 2022 will persist for years – and should be carefully assessed both by policy makers and market players. The steep decline in Russian piped gas deliveries to the European Union – a drop of close to 120 bcm through 2022-23 – reconfigured global LNG flows towards Europe. Consequently, the role of LNG in the European market drastically shifted. While in the past, LNG cargoes supplied the marginal molecule, LNG is now acting as baseload, in a similar fashion as Norwegian or North African piped gas. The share of LNG in the European Union’s gas demand rose from an average of 12% over the 2010s to close to 35% in 2022 – a share similar to Russia’s piped gas before the invasion of Ukraine. Europe has repositioned itself as the new premium LNG market. TTF was trading at USD 6/MBtu above Asian spot LNG prices in 2022. The price signal provided by TTF and other liquid European hubs was crucial to attract the necessary volumes of flexible LNG to Europe. Forward curves at the end of June 2023 suggest that the European premium is expected to stay in the coming years, with TTF’s premium over Asian spot LNG prices averaging USD 0.3/MBtu through 2023-25. The European Union’s exposure to the spot market is set to increase if no long-term contracts are signed Through the past two decades, long-term contracts, together with domestic production, met around 80-90% of EU gas demand on an annual basis. The non-observance of Russian piped gas contracts steeply increased the European Union’s reliance on spot procurements, rising from just 20% in 2021 to over 50% in 2023. The share of spot volumes is expected to increase to more than 70% by 2030 – if expiring contracts are not renewed and no new contracts are signed. This will naturally increase Europe's exposure to the greater volatility of spot markets over the medium term. Hence, a fine balance should be struck between non-Russian long-term contracts and procurements from an increasingly liquid spot market. A higher share of long-term contracts

- 18. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 18 could potentially provide greater price and supply stability. Natural gas producers and consumers should work closely together to reduce the emission intensity of gas and LNG supply, in order to hedge against tightening emission regulations Gas supply flexibility options need to be reassessed amid the phase-out of Russian piped gas imports into the European Union Russian piped gas contracts included significant intra-annual and inter-annual flexibility, with the nomination rights ultimately lying with the buyers. This flexibility – underpinned by the country’s huge swing fields – played a key role in meeting short-term demand variability and seasonal swings. This contributed to the balancing of European and global gas markets. Overall, the inter-annual flexibility provided by Russian piped gas averaged close to 10 bcm on an annual basis through the 2010s. Intra-annual swings averaged close to 200 mcm/d between 2016-21, amounting to over 10% of EU gas demand on a cold day. This structurally lower gas supply flexibility means that other flexibility options, such as storage and LNG peak-shaving and demand response, will have to play a greater role in coming years. Based on projects currently in development, global natural gas and LNG storage capacity in import markets is expected to expand by 10% (or 45 bcm) during 2023-28. In addition, a closer dialogue between producers and consumers should facilitate the development of innovative commercial offerings, new procurement mechanisms and co-operation frameworks favouring a more flexible supply of LNG. A prime example is the coordination mechanism agreed between Japan and Thailand, building on seasonal differences in natural gas demand in the two countries. China’s role as a balancing market is set to increase, with potential ripple effects for energy supply security and clean energy transitions Prior to the 2022 gas supply shock, Europe played a key role in balancing the global gas market. This role was underpinned by several unique features of the European market, including: 1) flexible piped gas supply from Russia; 2) coal-to-gas switching potential in the power sector; 3) spare LNG regasification capacity; 4) vast underground storage capacity; 5) open, non-discriminatory third- party access to natural gas infrastructure and 6) liquid, well- traded gas hubs. Russia’s steep gas supply cuts in 2022 largely eroded Europe’s role as a balancing market. The unprecedented 20% drop in China’s LNG imports – reflecting lower spot procurements and exercising destination flexibility rights in long-term LNG contracts – was a key factor in enabling higher LNG shipments to the European market. In contrast to Europe, China’s role as a balancing market is expected to increase over the medium term, especially when considering the country’s active role in securing LNG contracts. China alone accounted for 30% of all LNG sales and purchase agreements (SPAs) signed in the past five years. As a result, China’s share of active LNG contracts is expected to rise from 12% in 2021 to close to 25% by 2030. This is set to boost the role of Chinese companies in LNG trading and the optimisation of global LNG flows. Nevertheless, China’s potential role as a balancing market will have ripple effects, both in terms of energy supply security and energy transitions: China has limited underground storage capacity. At the end of 2022, China’s working gas storage capacity was estimated at 18 bcm, accounting for just 5% of the country’s annual consumption – well below the level in mature markets. This contrasts with the European Union’s 100 bcm of working storage capacity (accounting for over 25% of annual gas demand), although China relies to a larger extenton its domestic production and portfolio of LNG contracts.

- 19. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 19 China does not have the same access to flexible piped gas supplies that Europe had in the past. Central Asian flows displayed often-negative seasonal swings due to cold spells during the winter seasons, while Russian deliveries viathe Power of Siberia pipeline system have limited flexibility inabsolute terms. A key contributor to China’s gas demand flexibility is the country’s significant gas-to-coal switching potential. In 2022, coal-fired generation rose by an estimated 1.9%, largely at the expense of gas-fired power plants, which reduced their output by close to 10% y- o-y. This translated into higher emissions (estimated at 15 Mt CO2-equivalent), further putting tensions on clean energy transitions. The majority of China's LNG importers are state-owned companies. Market-driven decision-making might be overwritten by supply security concerns or geopolitical considerations. The medium- to long-term outlook for natural gas demand is being revised downwards The global gas crisis triggered by Russia deeply damaged the medium- to long-term growth prospects for natural gas demand. The sharp increase in natural gas prices reduced its competitiveness vis-à-vis other sources of energy supply, while its image as a “reliable” fuel has been called into question by steep supply cuts of Russian piped gas. Global gas demand growth for the period between 2020 and 2024 was reduced by 40% compared to projections prior to Russia’s invasion of Ukraine. The IEA’s Gas 2021 report projected an increase of 350 bcm through 2020-24, which is revised down to 200 bcm in our latest forecast. Europe alone accounts for more than half of this downward revision. This reflects more stringent energy efficiency standards, the accelerated deployment of renewables and quicker electrification of heat, as well as a reduced role of natural gas in industry. The IEA’s World Energy Outlook 2023 edition and the Gas report Q4 2023 will provide an in-depth analysis of the medium- and long- term prospects of natural gas and gaseous fuels.

- 20. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 20 NewBase Energy News 20-July 2023 - Issue No. 1640 call on +971504822502, UAE The Editor:” Khaled Al Awadi” Your partner in Energy Services NewBase energy news is produced Twice a week and sponsored by Hawk Energy Service – Dubai, UAE. For additional free subscriptions, please email us. About: Khaled Malallah Al Awadi, Energy Consultant MS & BS Mechanical Engineering (HON), USA Emarat member since 1990 ASME member since 1995 Hawk Energy member 2010 www.linkedin.com/in/khaled-al-awadi-38b995b Mobile: +971504822502 khdmohd@hawkenergy.net or khdmohd@hotmail.com Khaled Al Awadi is a UAE National with over 30 years of experience in the Oil & Gas sector. Has Mechanical Engineering BSc. & MSc. Degrees from leading U.S. Universities. Currently working as self leading external Energy consultant for the GCC area via many leading Energy Services companies. Khaled is the Founder of the NewBase Energy news articles issues, Khaled is an international consultant, advisor, ecopreneur and journalist with expertise in Gas & Oil pipeline Networks, waste management, waste-to-energy, renewable energy, environment protection and sustainable development. His geographical areas of focus include Middle East, Africa and Asia. Khaled has successfully accomplished a wide range of projects in the areas of Gas & Oil with extensive works on Gas Pipeline Network Facilities & gas compressor stations. Executed projects in the designing & constructing of gas pipelines, gas metering & regulating stations and in the engineering of gas/oil supply routes. Has drafted & finalized many contracts/agreements in products sale, transportation, operation & maintenance agreements. Along with many MOUs & JVs for organizations & governments authorities. Currently dealing for biomass energy, biogas, waste-to-energy, recycling and waste management. He has participated in numerous conferences and workshops as chairman, session chair, keynote speaker and panelist. Khaled is the Editor-in-Chief of NewBase Energy News and is a professional environmental writer with over 1400 popular articles to his credit. He is proactively engaged in creating mass awareness on renewable energy, waste management, plant Automation IA and environmental sustainability in different parts of the world. Khaled has become a reference for many of the Oil & Gas Conferences and for many Energy program

- 21. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 21 broadcasted internationally, via GCC leading satellite Channels. Khaled can be reached at any time, see contact details above.

- 22. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 22

- 23. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 23

- 24. Copyright © 2023 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavors have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 24