More Related Content

Similar to Daily livestock report jan 17 2013

Similar to Daily livestock report jan 17 2013 (20)

More from joseleorcasita (20)

Daily livestock report jan 17 2013

- 1. Sponsored by

Vol. 11, No. 12 / January 17, 2013

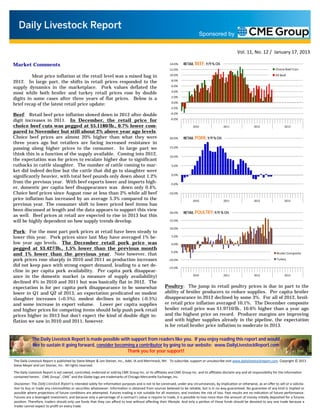

Market Comments 14.0% RETAIL BEEF: Y/Y % CH.

12.0% Choice Beef Cuts

Meat price inflation at the retail level was a mixed bag in 10.0% All Beef

2012. In large part, the shifts in retail prices responded to the 8.0%

supply dynamics in the marketplace. Pork values deflated the 6.0%

most while both broiler and turkey retail prices rose by double 4.0%

digits in some cases after three years of flat prices. Below is a 2.0%

brief recap of the latest retail price update: 0.0%

-2.0%

Beef: Retail beef price inflation slowed down in 2012 after double -4.0%

digit increases in 2011. In December, the retail price for -6.0%

choice beef cuts was pegged at $5.1180/lb., 0.7% lower com- 2010 2011 2012 2013

pared to November but still about 2% above year ago levels.

Choice beef prices are almost 20% higher than what they were 20.0% RETAIL PORK: Y/Y % CH.

three years ago but retailers are facing increased resistance in

passing along higher prices to the consumer. In large part we 15.0%

think this is a function of the supply available. Coming into 2012, 10.0%

the expectation was for prices to escalate higher due to significant

cutbacks in cattle slaughter. The number of cattle coming to mar- 5.0%

ket did indeed decline but the cattle that did go to slaughter were

significantly heavier, with total beef pounds only down about 1.2% 0.0%

from the previous year. With beef exports lower and imports high- -5.0%

er, domestic per capita beef disappearance was down only 0.4%.

Choice beef prices since August rose at less than 2% while all beef -10.0%

price inflation has increased by an average 5.3% compared to the 2010 2011 2012 2013

previous year. The consumer shift to lower priced beef items has

been discussed at length and the data appears to support this view

20.0% RETAIL POULTRY: Y/Y % CH.

as well. Beef prices at retail are expected to rise in 2013 but this

will be highly dependent on how supply trends develop. 15.0%

10.0%

Pork: For the most part pork prices at retail have been steady to

lower this year. Pork prices since last May have averaged 1% be- 5.0%

low year ago levels. The December retail pork price was 0.0%

pegged at $3.427/lb., 1.5% lower than the previous month

-5.0%

and 1% lower than the previous year. Note however, that Broiler Composite

pork prices rose sharply in 2010 and 2011 as production increases -10.0% Turkey

did not keep pace with strong export demand, leading to a net de- -15.0%

cline in per capita pork availability. Per capita pork disappear-

ance in the domestic market (a measure of supply availability) 2010 2011 2012 2013

declined 4% in 2010 and 2011 but was basically flat in 2012. The

expectation is for per capita pork disappearance to be somewhat Poultry: The jump in retail poultry prices is due in part to the

lower in Q1 and Q2 of 2013, an expectation predicated on modest ability of broiler producers to reduce supplies. Per capita broiler

slaughter increases (+0.5%), modest declines in weights (-0.5%) disappearance in 2012 declined by some 3%. For all of 2012, broil-

and some increase in export volume. Lower per capita supplies er retail price inflation averaged 10.1%. The December composite

and higher prices for competing items should help push pork retail broiler retail price was $1.9710/lb., 10.6% higher than a year ago

prices higher in 2013 but don't expect the kind of double digit in- and the highest price on record. Producer margins are improving

flation we saw in 2010 and 2011, however. and with higher supplies already in the pipeline, the expectation

is for retail broiler price inflation to moderate in 2013.

The Daily Livestock Report is made possible with support from readers like you. If you enjoy reading this report and would

like to sustain it going forward, consider becoming a contributor by going to our website: www.DailyLivestockReport.com

Thank you for your support!

The Daily Livestock Report is published by Steve Meyer & Len Steiner, Inc., Adel, IA and Merrimack, NH. To subscribe, support or unsubscribe visit www.dailylivestockreport.com. Copyright © 2013

Steve Meyer and Len Steiner, Inc. All rights reserved.

The Daily Livestock Report is not owned, controlled, endorsed or sold by CME Group Inc. or its affiliates and CME Group Inc. and its affiliates disclaim any and all responsibility for the informa on

contained herein. CME Group®, CME® and the Globe logo are trademarks of Chicago Mercan le Exchange, Inc.

Disclaimer: The Daily Livestock Report is intended solely for informa on purposes and is not to be construed, under any circumstances, by implica on or otherwise, as an offer to sell or a solicita-

on to buy or trade any commodi es or securi es whatsoever. Informa on is obtained from sources believed to be reliable, but is in no way guaranteed. No guarantee of any kind is implied or

possible where projec ons of future condi ons are a empted. Futures trading is not suitable for all investors, and involves the risk of loss. Past results are no indica on of future performance.

Futures are a leveraged investment, and because only a percentage of a contract’s value is require to trade, it is possible to lose more than the amount of money ini ally deposited for a futures

posi on. Therefore, traders should only use funds that they can afford to lose without affec ng their lifestyle. And only a por on of those funds should be devoted to any one trade because a

trader cannot expect to profit on every trade.