1. Oz Metals

16th

Edition – 1st

Feb 2015

DISCLAIMER

This report is provided in good faith from sources believed to be accurate and reliable. Terra Studio Pty Ltd directors and employees do not accept liability

for the results of any action taken on the basis of the information provided or for any errors or omissions contained therein. Readers should seek investment

advice from their professional advisors before acting upon information contained herein.

Page 1 / 4

TerraStudio

ANOTHER YEAR, ANOTHER COPPER SURPLUS

EXPECTED… REALLY?

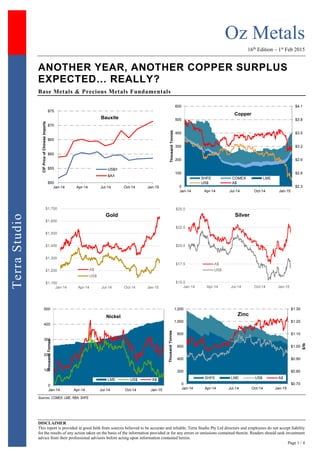

Base Metals & Precious Metals Fundamentals

Sources: COMEX, LME, RBA, SHFE

$50

$55

$60

$65

$70

$75

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15

CIFPriceofChineseImports

Bauxite

US$/t

$A/t

$2.3

$2.6

$2.9

$3.2

$3.5

$3.8

$4.1

0

100

200

300

400

500

600

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15

ThousandTonnes

Copper

SHFE COMEX LME

US$ A$

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15

Gold

A$

US$

$15.0

$17.5

$20.0

$22.5

$25.0

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15

Silver

A$

US$

$6

$9

0

100

200

300

400

500

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15

$/lb

ThousandTonnes

Nickel

LME US$ A$

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

$1.30

0

200

400

600

800

1,000

1,200

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15

$/lb

ThousandTonnes

Zinc

SHFE LME US$ A$

2. Oz Metals

16th

Edition – 1st

Feb 2015

DISCLAIMER

This report is provided in good faith from sources believed to be accurate and reliable. Terra Studio Pty Ltd directors and employees do not accept liability

for the results of any action taken on the basis of the information provided or for any errors or omissions contained therein. Readers should seek investment

advice from their professional advisors before acting upon information contained herein.

Page 2 / 4

TerraStudio

Markets & Majors

Thomson Reuters - The global copper market oversupply is

expected to shrink this year and next, helping cushion prices

of an industrial metal that has suffered due to slowing growth

in top consumer China, a Reuters poll showed. In a prediction

that could signal a reversal of chronic oversupply, the poll

also showed the aluminium market could post its first deficit

in nine years. Supplies are projected to remain scarce overall

within the base metals complex, with all the metals -- except

copper -- expected to register a deficit over the next two years.

Analysts began the year on a bearish footing, with forecasts

for all six base metals slashed from estimates in October.

Some 34 market participants surveyed over the last three

weeks expect cash copper prices to average $6,371.70 a

tonne this year, down 5% from 2015 forecasts in a previous

poll. In 2016, prices are seen rising to $6,813. The poll

showed analysts expect the copper market to have a surplus

of 221,000 tonnes this year, compared with a surplus of

350,000 tonnes forecast previously in October. In 2016, the

surplus is seen narrowing to 200,000 tonnes.

Thomson Reuters - London-based broker Traderight Ltd has

downgraded its membership of the LME, the latest to scale

back in the base metals business as slowing growth and

higher costs of regulation eat into profits. The LME, the oldest

and biggest market for base metals such as copper and

aluminium, said that Traderight has moved to category 4

membership. Traderight was previously a category 2, or

associate broker member, which allows membership to the

LME's new clearing house. Category 4 members do not have

the ability to clear trades. Traderight is backed by some of the

biggest hitters in the metals industry, including China's largest

metals trading house Maike and London-based hedge fund

RK Capital.

Reuters - Newly elected President Edgar Lungu said

Zambia's new mineral royalty tax, which hiked royalty rates

on open-pit mining operations and underground mines in the

country to 20% and 8%, respectively, from 6%, will stay.

Business News Americas - Chilean President Michelle

Bachelet said that the Latin American country will

contemplate establishment of public-private partnerships in a

bid to develop future lithium initiatives.

Mining.com - In New York trade on Friday copper futures

advanced nearly 2% on the back of a huge rally in oil and a

comeback in the gold price, but at US$2.50/lb remains near

mid-2009 lows. Copper has likely been ‘over-sold’, given the

fifth-highest imports into China on record in December, new

fiscal stimulus by Beijing to spur the economy (speeding up

spending on 300 infrastructure projects) and a planned 24%

increase in capital spending by the State Electricity Grid

(likely geared towards copper cable). Mining companies have

recently cut projected output for 2015 by 300,000 tonnes (Rio

Tinto at Kennecott, BHP Billiton at Escondida and Glencore

at Alumbrera), helping to trim an expected surplus this year

to a modest 250,000 tonnes.

The Australian - Rio Tinto has offered to drop a US$1.6 billion

royalty the company would receive from its Oyu Tolgoi

copper-gold mine to break the deadlock with the Mongolian

government over a stalled US$5 billion expansion of the

project.

The Monitor - BHP Billiton could be forced to lay off more

workers at its Olympic Dam copper mine in South Australia

as the mining giant looks to further cut costs. "With this fall in

price, we have no choice but to further accelerate our cash

reduction efforts," the report quoted BHP Olympic Dam Asset

President Darryl Cuzzubbo as saying.

Thomson Reuters - Freeport-McMoRan is expected to export

500,000 tonnes of copper concentrate from its Indonesian

operations over the next six months, down 100,000 tonnes

from the previous six months, a company official said. The

official from Freeport's Indonesian unit, who made the

comment late on Sunday and declined to be named, did not

give a reason for the expected fall in exports. The Indonesian

government extended Freeport's permit to continue shipping

copper concentrate for another six months after the miner

announced a site for a new copper smelter.

First Quantum Minerals said it will shortly reopen its

Ravensthorpe nickel mine in Western Australia at a limited

capacity, The West Australian reported. Operations at the

mine were suspended in December 2014 after a leach tank

burst and spilled slurry, damaging a power substation. The

company expects to produce 24,000 tonnes to 30,000 tonnes

of nickel from the mine in 2015.

Metal Bulletin - China's refined zinc imports dropped for the

sixth consecutive month in December 2014 to 17,469 tonnes

— down 71% from a year earlier — though exports remained

high as tightening credit availability from banks dampened

demand and forced sellers to search for alternative outlets.

Australian Companies

Newcrest Mining reported total gold production of 577,110

ounces for the quarter ended Dec. 31, 2014, up slightly from

the 561,731 ounces produced in the previous quarter. The

company upped its gold and copper production guidance for

fiscal 2015, now expecting to produce between 2.3 million

ounces and 2.5 million ounces of gold, and between 90,000

tonnes and 100,000 tonnes of copper.

Northern Star Resources said total gold sold by the company

in the quarter ended Dec. 31, 2014, was in line with guidance

at 142,556oz, as were all-in sustaining costs of A$1,073/oz.

3. Oz Metals

16th

Edition – 1st

Feb 2015

DISCLAIMER

This report is provided in good faith from sources believed to be accurate and reliable. Terra Studio Pty Ltd directors and employees do not accept liability

for the results of any action taken on the basis of the information provided or for any errors or omissions contained therein. Readers should seek investment

advice from their professional advisors before acting upon information contained herein.

Page 3 / 4

TerraStudio

PanAust said the group's consolidated output in 2014

exceeded guidance, with copper in concentrate production

rising 10% year over year to 71,155 tonnes. Meanwhile,

production of gold in concentrate and doré totaled 168,755

ounces, surpassing the guidance of between 160,000 oz and

165,000 oz. In 2015, PanAust expects to produce between

73,000 tonnes and 76,000 tonnes of copper in concentrate,

and between 175,000 ounces and 183,000 ounces of gold in

concentrate and doré.

Sandfire Resources further extended the mine life of its 1.5

million tonnes per annum DeGrussa copper-gold mine to mid-

2021. The company incorporated the high-grade

underground mineral resource of 9.5 million tonnes grading

5.7% copper and 2 g/t of gold for 546,000 tonnes contained

copper and 616,000 ounces contained gold to the mine plan,

and added a maiden ore reserve for the C4 deposit of 2

million tonnes grading 4.5% copper and 1.5 g/t of gold for

88,000 tonnes contained copper and 94,000 ounces

contained gold.

Mungana Goldmines reported an updated JORC-compliant

resource estimate for its King Vol zinc deposit in Queensland,

which will form the basis of development studies on the

property. The deposit hosts indicated resources containing

154,000 tonnes of zinc, 9,000 tonnes of copper, 7,000 tonnes

of lead and 1.23 million ounces of silver within 1.05 million

tonnes grading 14.7% zinc, 0.9% copper, 0.7% lead and 36.5

g/t of silver.

Transactions, Mergers & Acquisitions

Mining.com - The number of mergers and acquisitions in the

mining and metals industry declined to the lowest in a decade

last year as much anticipated private equity interest in the

sector evaporated. The report by E&Y shows 2014 was the

fourth consecutive year of declining M&A activity, with deal

volumes down 23% year-on-year to 544 in 2014, the lowest

volume of deals since 2003. Overall deal values have also

been spiraling downwards, tanking 49% from 2013 to

US$44.6 billion in 2014, the lowest since 2004. E&Y says the

larger number of sub-$10m deals which makes up nearly two-

thirds of all deals "indicates distress among juniors and

opportunistic buyers entering the market". Opportunistic

buyers buying distressed assets (aka vulture funds picking at

carcasses) aside, what's happened to the billions readied for

the sector we've been told for the past two years are imminent?

Bloomberg estimated funds raised for investments in mining

and metals last year topped $1 billion, compared to about

$8.8 billion in 2013. Others put the figure as high as $15

billion.

AFR - Panoramic Resources Managing Director Peter Harold

believes that the nickel sector is likely to see a rise in mergers

among cash-positive companies.

Alloy Resources secured an option over the Martin's Well

gold-silver-copper project, which contains walk up drill targets

on 2km of outcropping quartz-veined gossans. The project is

located in South Australia, where the company secured an

848km2

exploration license through application.

Bauxite Sector

Source: Bloomberg, SNL

Lithium-Tantalum Sector

Source: SNL

Tin Sector

Source: SNL

Nickel Sector

Source: SNL

Copper Producers

Source: SNL

Code Company Name

Close

Price

Week

r

YTD r

52 Week

Range

Market Cap

(A$m)

Cash

(A$m)

TEV

(A$m)

ABX Australian Bauxite 0.300 ▲ 11% (2%) 38 5 33

BAU Bauxite Resources 0.097 ▼ (8%) (1%) 22 25 (2)

MLM Metallica Minerals 0.057 ▼ (5%) 4% 10 1 9

MMI Metro Mining 0.038 ▼ (5%) 41% 11 8 3

Code Company Name

Close

Price

Week r YTD r

52 Week

Range

Market Cap

(A$m)

Cash

(A$m)

TEV

(A$m)

AJM Altura Mining 0.050 ▲ 6% (23%) 23 3 39

GXY Galaxy Resources 0.025 ▼ (7%) 0% 27 3 93

ORE Orocobre 2.93 ▲ 3% 5% 387 26 362

PLS Pilbara Minerals Ltd. 0.037 ▼ (8%) (12%) 23 2 21

RDR Reed Resources 0.039 ▲ 18% 3% 19 7 NA

Code Company Name

Close

Price

Week r YTD r

52 Week

Range

Market Cap

(A$m)

Cash

(A$m)

TEV

(A$m)

CSD Consolidated Tin Mines 0.052 ▼ (13%) 27% 15 0 15

ELT Elementos 0.006 ▼ (14%) (25%) 5 1 4

KAS Kasbah Resources Limited 0.053 ▼ (12%) (2%) 24 4 18

MLX Metals X Limited 1.10 ▲ 6% 40% 458 57 401

MOO Monto Minerals 0.002 — 0% 0% 3 1 2

SRZ Stellar Resources Limited 0.028 ▲ 8% (3%) 8 4 NA

VMS Venture Minerals Limited 0.037 ▼ (5%) 19% 11 7 4

Code Company Name

Close

Price

Week r YTD r

52 Week

Range

Market Cap

(A$m)

Cash

(A$m)

TEV

(A$m)

TEV/

EBITDA

IGO Independence Group 4.95 ▲ 5% 12% 1,160 57 1,131 8.1x

MBN Mirabella Nickel 0.029 — 0% 0% 27 31 66 NA

MCR Mincor Resources 0.72 ▲ 7% 23% 136 26 114 3.6x

PAN Panoramic Resources 0.46 ▼ (4%) 8% 146 64 90 1.9x

WSA Western Areas 4.02 ▼ (1%) 7% 935 231 922 6.4x

AVQ Axiom Mining 0.013 ▼ (7%) (13%) 44 2 41 NM

CZI Cassini Resources 0.10 ▼ (17%) (21%) 11 8 3 NM

DKM Duketon Mining 0.17 ▼ (13%) (37%) 13 7 6 NA

LEG Legend Mining 0.008 ▼ (11%) 14% 16 7 9 NA

MAT Matsa Resources 0.155 ▼ (3%) (9%) 22 3 20 NM

MLM Metallica Minerals 0.057 ▼ (5%) 4% 10 1 9 NA

PIO Pioneer Resources 0.018 ▲ 6% 38% 11 1 10 NM

POS Poseidon Nickel 0.11 — 0% (8%) 75 4 106 NM

SEG Segue Resources 0.006 ▼ (25%) 20% 12 1 11 NM

SGQ St George Mining 0.059 ▼ (12%) (6%) 7 1 5 NA

SIR Sirius Resources 2.51 ▼ (10%) (2%) 857 59 798 NM

TLM Talisman Mining 0.15 ▲ 11% (3%) 20 16 4 NM

WIN Winward Resources 0.13 ▲ 19% (22%) 11 6 5 NM

Code Company Name

Close

Price

Week

r

YTD r

52 Week

Range

Market Cap

(A$m)

Cash

(A$m)

TEV

(A$m)

TEV/

EBITDA

ABY Aditya Birla Minerals 0.20 ▲ 3% 3% 63 137 (42) NA

AOH Altona Mining 0.23 ▲ 2% (4%) 123 129 (6) 3.0x

HGO Hillgrove Resources 0.38 ▲ 1% (16%) 56 16 70 1.7x

KBL KBL Mining 0.018 ▼ (40%) (40%) 7 7 22 1.4x

MWE Mawson West 0.035 ▲ 75% (30%) 7 48 36 NM

OZL OZ Minerals 3.87 ▲ 12% 11% 1,174 364 1,020 5.6x

PNA PanAust 1.21 ▼ (9%) (14%) 771 130 1,016 NA

SFR Sandfire Resources 4.27 ▲ 1% (6%) 666 58 769 3.5x

SRQ Straits Resources 0.003 ▼ (25%) (40%) 4 13 127 17.2x

TGS Tiger Resources 0.05 ▼ (55%) (62%) 56 80 202 NA

985 CST Mining 0.044 — 0% 0% 1,192 136 99 0.2x

1208 MMG 2.22 ▼ (4%) (8%) 11,743 137 24,668 4.0x

3993 China Molybdenum 4.90 ▼ (2%) 9% 57,955 1,883 62,003 NA

4. Oz Metals

16th

Edition – 1st

Feb 2015

DISCLAIMER

This report is provided in good faith from sources believed to be accurate and reliable. Terra Studio Pty Ltd directors and employees do not accept liability

for the results of any action taken on the basis of the information provided or for any errors or omissions contained therein. Readers should seek investment

advice from their professional advisors before acting upon information contained herein.

Page 4 / 4

TerraStudio

Copper Developers & Explorers

Source: ASX, SNL

Nickel Sector

Source: SNL

Gold Producers

Source: SNL

Gold Developers & Explorers

Source: SNL

Zinc & Poly-metallic Sector

Source: SNL

For further information, please contact:

J-François Bertincourt

m +61 406 998 779

jf@terrastudio.biz

au.linkedin.com/in/jfbertincourt

Code Company Name

Close

Price

Week

r

YTD r

52 Week

Range

Market Cap

(A$m)

Cash

(A$m)

TEV

(A$m)

ARE Argonaut Resources 0.010 ▼ (17%) (38%) 4 1 3

AVB Avanco Resources 0.073 ▼ (5%) (4%) 121 20 101

AVI Avalon Minerals 0.025 ▲ 25% 25% 4 1 NA

AZS Azure Minerals 0.017 ▼ (6%) (29%) 14 1 13

CDU CuDeco 1.41 — 0% (28%) 343 9 333

CVV Caravel Minerals 0.011 ▼ (8%) 38% 8 1 NA

ENR Encounter Resources 0.13 ▼ (7%) (4%) 17 4 13

ERM Emmerson Resources 0.032 ▼ (6%) 3% 12 3 9

FND Finders Resources 0.14 — 0% (7%) 93 8 77

GCR Golden Cross Resources 0.078 — 0% 11% 7 2 5

GPR Geopacific Resources 0.050 ▲ 9% (4%) 17 3 16

HAV Havilah Resources 0.140 ▼ (3%) 0% 22 6 16

HCH Hot Chili 0.16 ▼ (3%) 0% 56 13 53

HMX Hammer Metals 0.080 ▼ (2%) (2%) 7 1 6

IAU Intrepid Mines 0.13 ▲ 4% (4%) 48 59 (11)

IRN Indophil Resources 0.30 — 0% 0% 355 215 146

KDR Kidman Resources 0.062 ▲ 24% (7%) 7 3 4

KGL KGL Resources 0.16 ▼ (14%) (29%) 22 10 13

MEP Minotaur Exploration 0.10 ▼ (20%) (31%) 18 7 11

MNC Metminco 0.007 — 0% (13%) 13 3 10

MTH Mithril Resources 0.006 — 0% (14%) 3 1 1

PEX Peel Mining 0.065 ▲ 8% (6%) 9 3 5

RDM Red Metal 0.06 ▼ (7%) (22%) 11 2 9

RER Regal Resources 0.041 ▼ (5%) (11%) 8 2 5

RTG RTG Mining 0.710 ▼ (10%) 22% 80 11 73

RXM Rex Minerals 0.11 — 0% 0% 24 3 NA

SMD Syndicated Metals 0.026 ▼ (4%) (19%) 7 2 5

SRI Sipa Resources 0.037 ▼ (8%) 0% 23 4 19

SUH Southern Hemisphere 0.040 — 0% (7%) 10 2 7

THX Thundelarra Resources 0.099 ▼ (6%) (10%) 32 7 24

XAM Xanadu Mines 0.090 ▼ (1%) (10%) 33 4 34

Code Company Name

Close

Price

Week r YTD r

52 Week

Range

Market Cap

(A$m)

Cash

(A$m)

TEV

(A$m)

TEV/

EBITDA

IGO Independence Group 4.95 ▲ 5% 12% 1,160 57 1,131 8.1x

MBN Mirabella Nickel 0.029 — 0% 0% 27 31 66 NA

MCR Mincor Resources 0.72 ▲ 7% 23% 136 26 114 3.6x

PAN Panoramic Resources 0.46 ▼ (4%) 8% 146 64 90 1.9x

WSA Western Areas 4.02 ▼ (1%) 7% 935 231 922 6.4x

AVQ Axiom Mining 0.013 ▼ (7%) (13%) 44 2 41 NM

CZI Cassini Resources 0.10 ▼ (17%) (21%) 11 8 3 NM

DKM Duketon Mining 0.17 ▼ (13%) (37%) 13 7 6 NA

LEG Legend Mining 0.008 ▼ (11%) 14% 16 7 9 NA

MAT Matsa Resources 0.155 ▼ (3%) (9%) 22 3 20 NM

MLM Metallica Minerals 0.057 ▼ (5%) 4% 10 1 9 NA

PIO Pioneer Resources 0.018 ▲ 6% 38% 11 1 10 NM

POS Poseidon Nickel 0.11 — 0% (8%) 75 4 106 NM

SEG Segue Resources 0.006 ▼ (25%) 20% 12 1 11 NM

SGQ St George Mining 0.059 ▼ (12%) (6%) 7 1 5 NA

SIR Sirius Resources 2.51 ▼ (10%) (2%) 857 59 798 NM

TLM Talisman Mining 0.15 ▲ 11% (3%) 20 16 4 NM

WIN Winward Resources 0.13 ▲ 19% (22%) 11 6 5 NM

Code Company Name

Close

Price

Week

r

YTD r

52 Week

Range

Market Cap

(A$m)

Cash

(A$m)

TEV

(A$m)

TEV/

EBITDA

AGD Austral Gold 0.10 — 0% (23%) 48 NA 116 8.6x

ALK Alkane Resources 0.26 ▲ 4% 18% 108 16 92 13.6x

AMI Aurelia Metals 0.24 ▼ (11%) 0% 87 22 172 NM

BDR Beadell Resources 0.29 ▼ (17%) 27% 228 10 290 NA

DRM Doray Minerals 0.47 ▼ (13%) (2%) 108 16 108 3.3x

EVN Evolution Mining 0.90 ▼ (10%) 40% 643 32 773 3.8x

IGO Independence Group 4.95 ▲ 5% 12% 1,160 57 1,131 8.1x

KCN Kingsgate Consolidated 0.79 — 0% 20% 177 54 277 NM

KRM Kingsrose Mining 0.25 ▼ (14%) (2%) 90 7 95 NM

LSA Lachlan Star 0.033 ▲ 38% 65% 5 2 24 NA

MIZ Minera Gold 0.003 — 0% 0% 8 0 13 NA

MLX Metals X 1.10 ▲ 6% 40% 458 57 401 5.7x

MML Medusa Mining 0.83 ▼ (3%) 27% 171 13 167 2.7x

MOY Millennium Minerals 0.036 ▼ (10%) (3%) 8 2 46 NA

NCM Newcrest Mining 13.56 ▼ (2%) 25% 10,394 141 14,455 NM

NGF Norton Gold Fields 0.19 — 0% 48% 172 38 273 NA

NST Northern Star Resources 1.80 ▼ (15%) 20% 1,063 82 987 11.8x

OGC OceanaGold Corp. 2.80 ▲ 6% 39% 843 NA 977 4.9x

PGI PanTerra Gold 0.017 ▲ 6% (6%) 14 5 89 NA

PRU Perseus Mining 0.35 ▼ (7%) 33% 182 37 146 6.2x

RMS Ramelius Resources 0.135 — 0% 165% 63 12 53 NM

RRL Regis Resources 1.90 ▼ (5%) (2%) 947 7 980 NM

RSG Resolute Mining 0.37 ▼ (13%) 40% 237 19 NA NA

SAR Saracen Mineral Holdings 0.36 ▼ (13%) 41% 285 36 264 6.3x

SBM St Barbara 0.21 ▲ 8% 100% 104 79 364 NM

SLR Silver Lake Resources 0.23 ▼ (25%) 15% 113 24 102 NM

TBR Tribune Resources 3.15 ▼ (2%) 19% 158 11 172 10.0x

TRY Troy Resources 0.56 ▼ (23%) 21% 108 43 105 NM

UML Unity Mining 0.010 ▼ (9%) 43% 11 7 NA NA

Code Company Name

Close

Price

Week

r

YTD r

52 Week

Range

Market Cap

(A$m)

Cash

(A$m)

TEV

(A$m)

ABU ABM Resources 0.30 ▼ (12%) 3% 82 10 72

AWV Anova Metals 0.039 ▼ (3%) 44% 10 1 8

AZM Azumah Resources 0.029 ▼ (19%) 45% 11 4 9

BLK Blackham Resources 0.096 ▼ (2%) 88% 14 1 13

BOK Black Oak Minerals 0.39 ▲ 4% 44% 17 11 31

BSR Bassari Resources 0.013 ▼ (32%) 8% 15 - 15

CHN Chalice Gold Mines 0.13 ▼ (7%) 24% 37 44 (7)

CHZ Chesser Resources 0.03 — 0% (11%) 7 1 8

DCN Dacian Gold 0.37 ▼ (8%) 32% 36 11 25

EXC Exterra Resources 0.012 ▼ (8%) (8%) 2 1 2

EXG Excelsior Gold 0.079 ▼ (6%) 30% 37 2 36

FML Focus Minerals 0.010 ▲ 11% 43% 91 81 91

GCY Gascoyne Resources 0.10 ▼ (17%) 41% 17 1 16

GMR Golden Rim Resources 0.009 ▲ 13% 80% 12 1 13

GOR Gold Road Resources 0.37 ▼ (3%) 51% 220 10 210

GRY Gryphon Minerals 0.076 ▼ (10%) 19% 30 34 NA

IDC Indochine Mining 0.012 ▼ (4%) (4%) 15 0 16

KGD Kula Gold 0.055 — 0% 25% 14 3 14

MSR Manas Resources 0.018 ▼ (14%) 29% 8 6 6

MUX Mungana Goldmines 0.10 ▲ 3% (22%) 24 5 18

MYG Mutiny Gold 0.047 ▼ (19%) 7% 32 3 29

OBS Orbis Gold 0.60 ▼ (5%) 7% 150 5 145

OGX Orinoco Gold 0.072 ▲ 3% 22% 10 1 11

PNR Pacific Niugini 0.058 ▲ 2% 16% 18 3 16

PXG Phoenix Gold 0.120 ▼ (14%) 22% 44 9 35

RED Red 5 0.105 ▼ (5%) 14% 80 38 41

RNI Resource & Investment 0.074 ▼ (8%) (1%) 36 5 51

RNS Renaissance Minerals 0.063 ▼ (10%) (3%) 25 2 24

SIH Sihayo Gold 0.018 ▲ 80% 125% 20 0 17

TAM Tanami Gold 0.015 ▼ (17%) 7% 18 1 24

WAF West African Resources 0.100 ▼ (5%) 0% 27 3 26

WPG WPG Resources 0.044 ▲ 2% 16% 12 3 8

Code Company Name

Close

Price

Week r YTD r

52 Week

Range

Market Cap

(A$m)

Cash

(A$m)

TEV

(A$m)

AQR Aeon Metals 0.086 ▼ (14%) (14%) 26 5 33

DGR DGR Global 0.031 ▼ (9%) (3%) 13 0 14

HRR Heron Resources 0.12 ▼ (8%) (4%) 43 28 19

IBG Ironbark Zinc 0.105 ▲ 9% 31% 46 3 44

IPT Impact Minerals 0.020 ▼ (23%) (17%) 11 1 NA

IVR Investigator Resources 0.019 ▲ 6% 19% 9 3 6

MRP MacPhersons Resources 0.145 ▲ 4% 16% 46 7 39

PNX Phoenix Copper 0.024 ▼ (11%) (20%) 8 3 6

RDM Red Metal 0.063 ▼ (7%) (22%) 11 8 3

RVR Red River Resources 0.16 — 0% 45% 28 4 24

RXL Rox Resources 0.026 ▼ (7%) (7%) 22 3 NA

TZN Terramin Australia 0.140 — 0% 27% 197 1 196

VXR Venturex Resources 0.004 — 0% (20%) 6 1 5