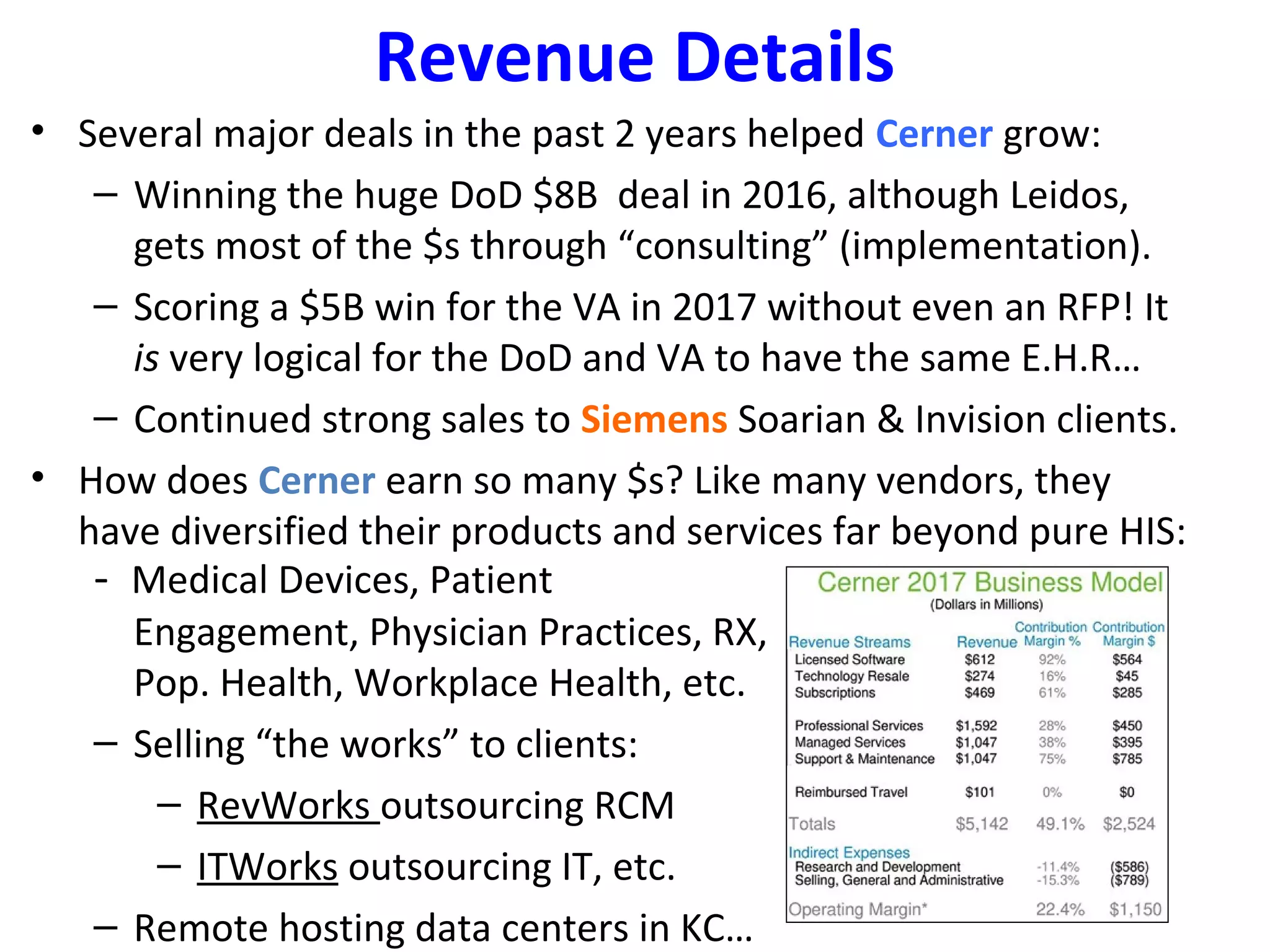

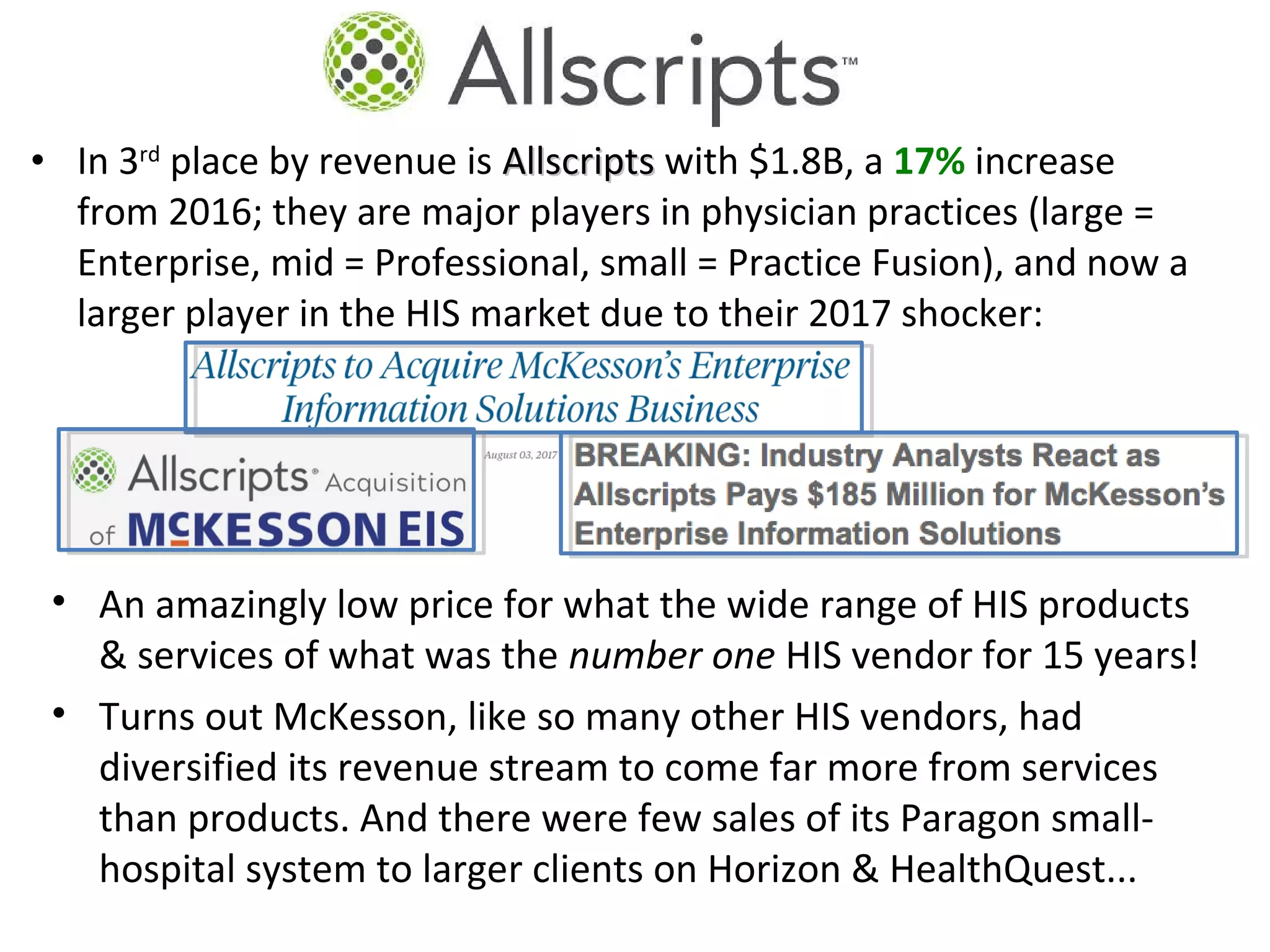

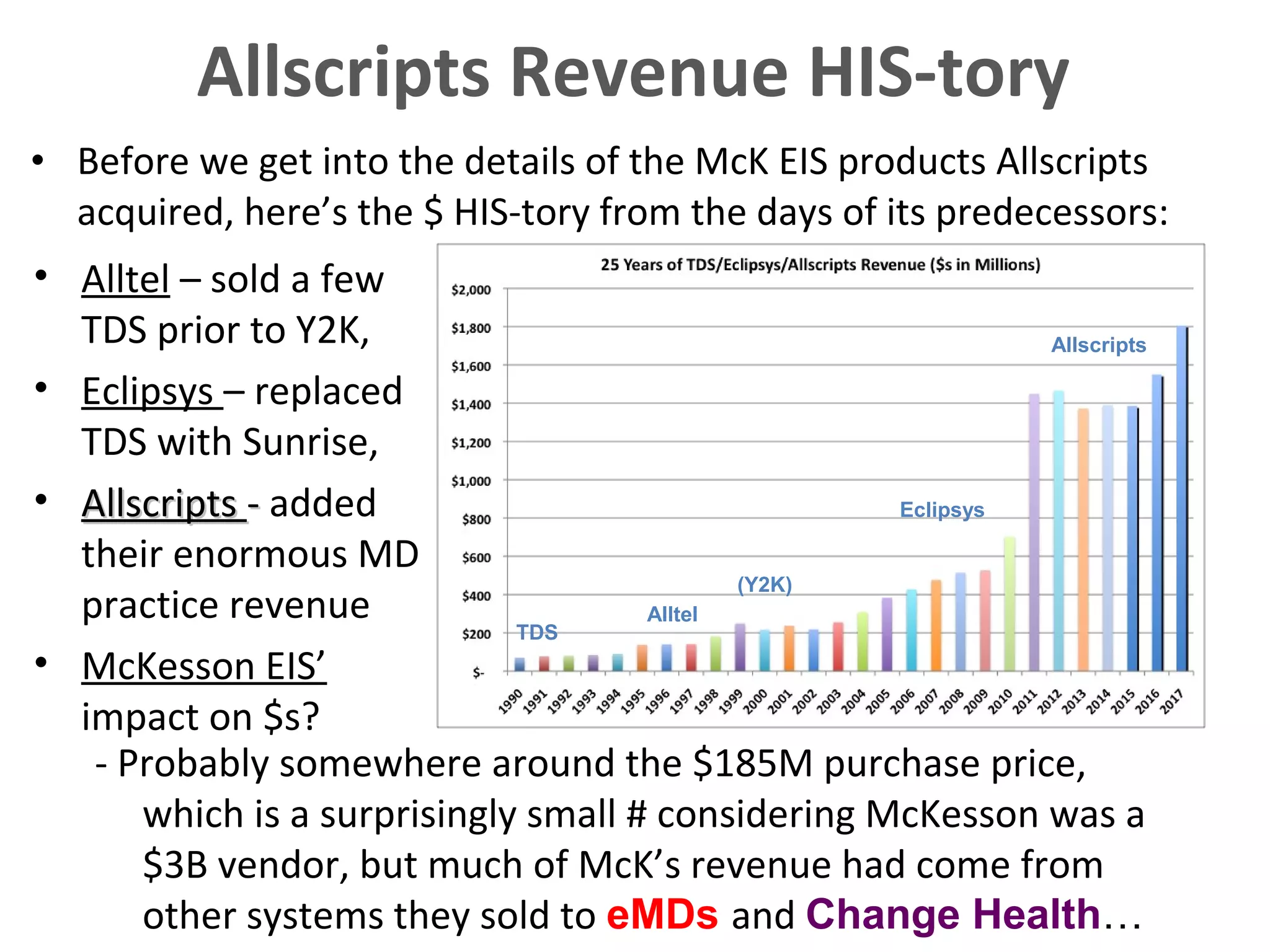

Cerner maintained the #1 spot for the fourth year in a row with over $5 billion in annual revenue. Their growth was driven by large government contracts like the $8 billion DoD deal and a $5 billion contract with the VA. Epic remained in second place with 9% revenue growth to $2.7 billion, and will likely gain clients switching from Siemens and Allscripts. Allscripts acquired McKesson's EIS business for $185 million, giving them new HIS products like Paragon to expand in the small hospital market as their physician practice business provides the majority of their $1.8 billion in revenue.